MACMILLAN AND CO., Limited

LONDON · BOMBAY · CALCUTTA · MADRAS

MELBOURNE

THE MACMILLAN COMPANY

NEW YORK · BOSTON · CHICAGO

DALLAS · SAN FRANCISCO

THE MACMILLAN CO. OF CANADA, Ltd.

TORONTO

Transcriber’s Note

Larger versions of most illustrations may be seen by right-clicking them and selecting an option to view them separately, or by double-tapping and/or stretching them.

Cover created by Transcriber from the original Title page and placed into the Public Domain.

BY THE SAME AUTHOR

INDIAN CURRENCY AND FINANCE.

Pp. viii + 263. 1913.

7s. 6d. net.

THE ECONOMIC CONSEQUENCES

OF THE PEACE.

Pp. vii + 279. 1919.

8s. 6d. net.

A TREATISE ON PROBABILITY.

Pp. xi + 466. 1921.

18s. net.

A REVISION OF THE TREATY.

Pp. viii + 223. 1922.

7s. 6d. net.

MACMILLAN AND CO., Limited

LONDON · BOMBAY · CALCUTTA · MADRAS

MELBOURNE

THE MACMILLAN COMPANY

NEW YORK · BOSTON · CHICAGO

DALLAS · SAN FRANCISCO

THE MACMILLAN CO. OF CANADA, Ltd.

TORONTO

A TRACT

ON

MONETARY REFORM

BY

JOHN MAYNARD KEYNES

FELLOW OF KING’S COLLEGE, CAMBRIDGE

MACMILLAN AND CO., LIMITED

ST. MARTIN’S STREET, LONDON

1923

COPYRIGHT

PRINTED IN GREAT BRITAIN

v

We leave Saving to the private investor, and we encourage him to place his savings mainly in titles to money. We leave the responsibility for setting Production in motion to the business man, who is mainly influenced by the profits which he expects to accrue to himself in terms of money. Those who are not in favour of drastic changes in the existing organisation of society believe that these arrangements, being in accord with human nature, have great advantages. But they cannot work properly if the money, which they assume as a stable measuring-rod, is undependable. Unemployment, the precarious life of the worker, the disappointment of expectation, the sudden loss of savings, the excessive windfalls to individuals, the speculator, the profiteer—all proceed, in large measure, from the instability of the standard of value.

It is often supposed that the costs of production are threefold, corresponding to the rewards of labour, enterprise, and accumulation. But there is a fourth cost, namely risk; and the reward of risk-bearing isvi one of the heaviest, and perhaps the most avoidable, burden on production. This element of risk is greatly aggravated by the instability of the standard of value. Currency Reforms, which led to the adoption by this country and the world at large of sound monetary principles, would diminish the wastes of Risk, which consume at present too much of our estate.

Nowhere do conservative notions consider themselves more in place than in currency; yet nowhere is the need of innovation more urgent. One is often warned that a scientific treatment of currency questions is impossible because the banking world is intellectually incapable of understanding its own problems. If this is true, the order of Society, which they stand for, will decay. But I do not believe it. What we have lacked is a clear analysis of the real facts, rather than ability to understand an analysis already given. If the new ideas, now developing in many quarters, are sound and right, I do not doubt that sooner or later they will prevail. I dedicate this book, humbly and without permission, to the Governors and Court of the Bank of England, who now and for the future have a much more difficult and anxious task entrusted to them than in former days.

J. M. KEYNES.

October 1923.

vii

| PAGE | |

| Preface | v |

| CHAPTER I | |

| The Consequences to Society of Changes in the Value of Money | 1 |

| I. As Affecting Distribution | 5 |

| 1. The Investor | 5 |

| 2. The Business Man | 18 |

| 3. The Earner | 27 |

| II. As Affecting Production | 32 |

| CHAPTER II | |

| Public Finance and Changes in the Value of Money | 41 |

| 1. Inflation as a Method of Taxation | 41 |

| 2. Currency Depreciation versus Capital Levy | 63 |

| CHAPTER III | |

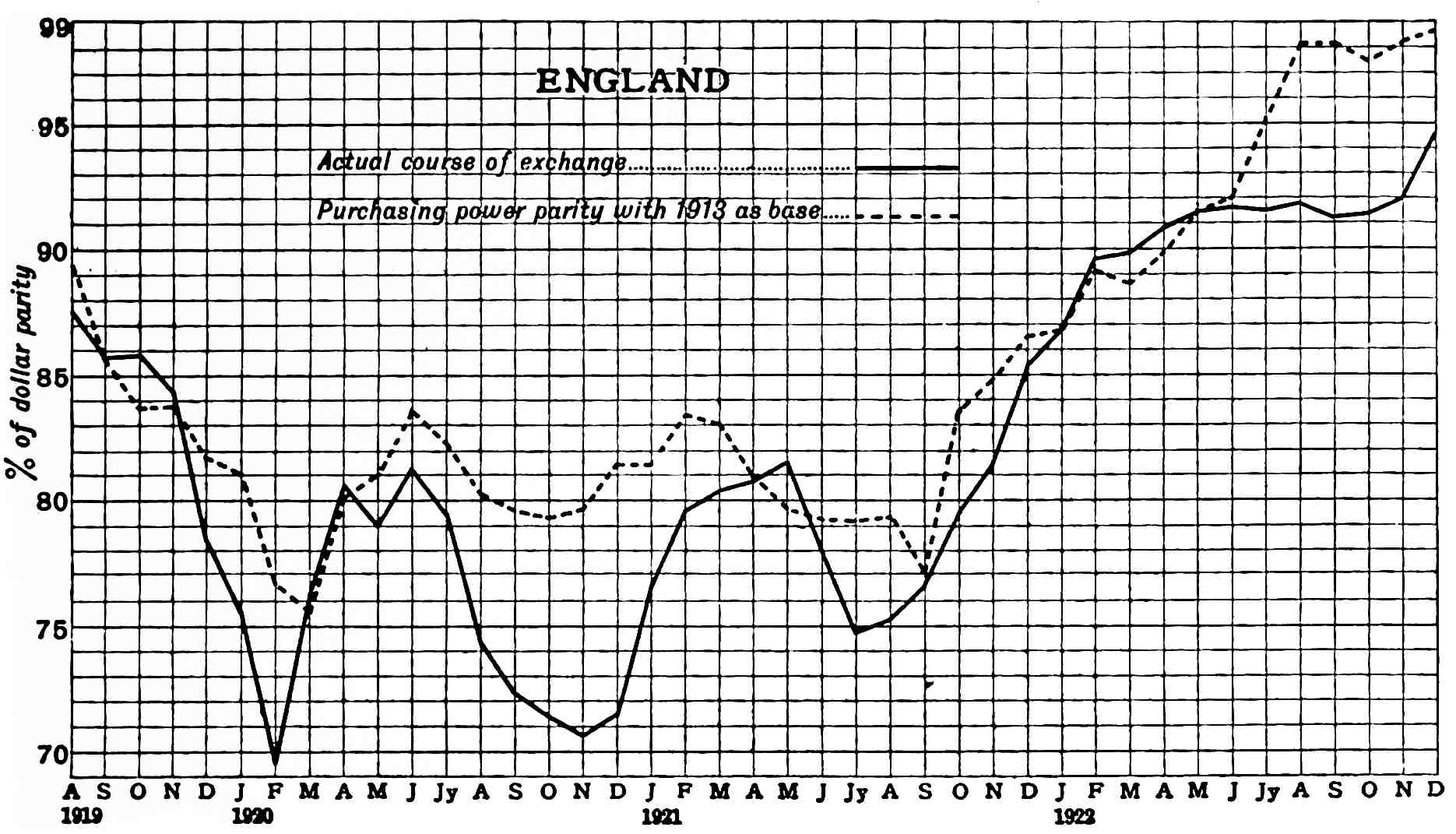

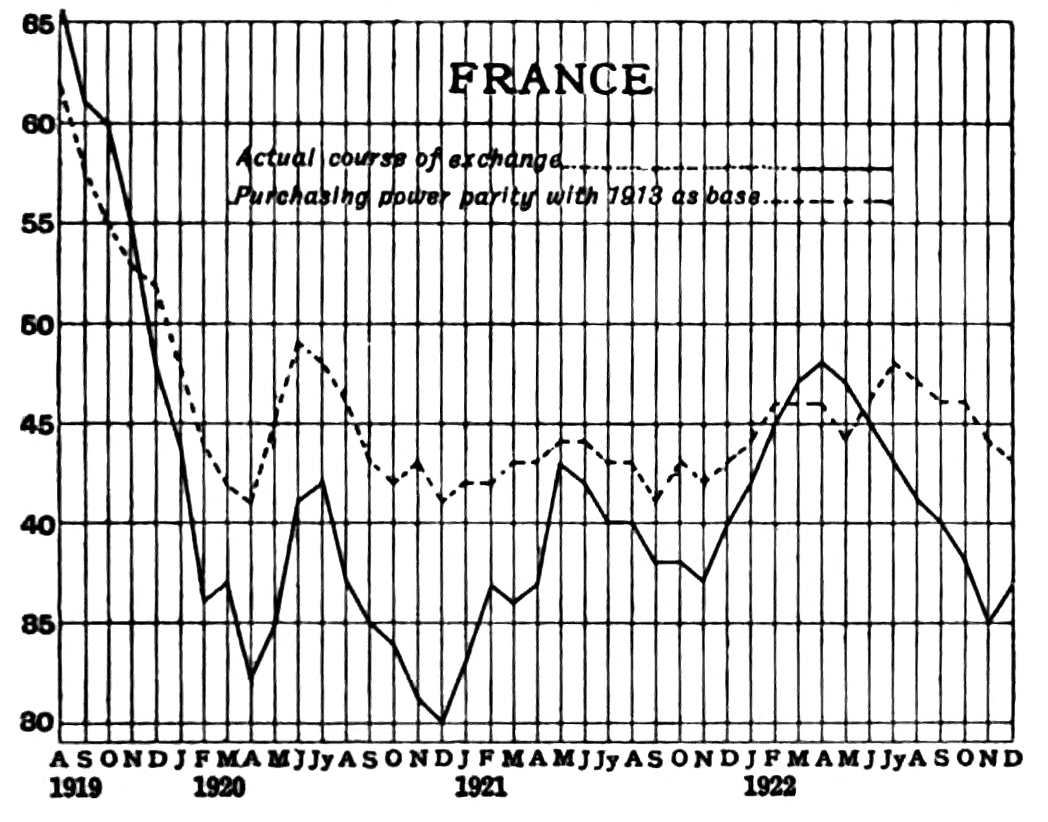

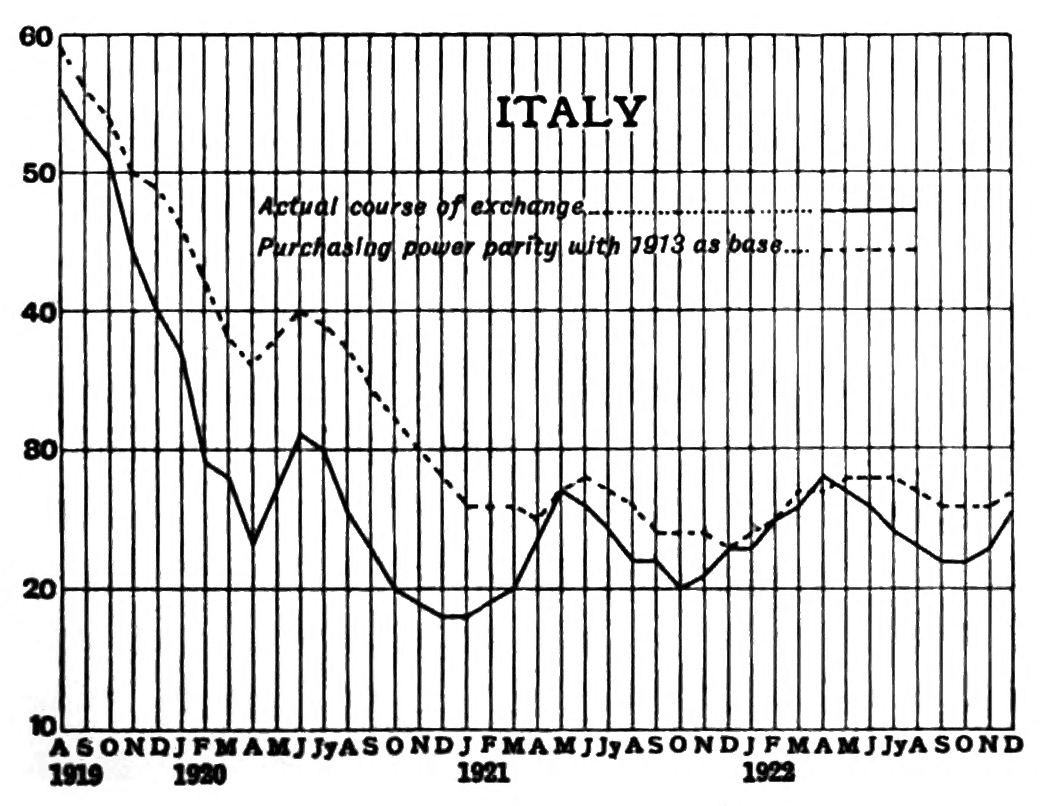

| The Theory of Money and the Exchanges | 74 |

| 1. The Quantity Theory re-stated | 74 |

| 2. The Theory of Purchasing Power Parity | 87 |

| 3. The Seasonal Fluctuation of the Exchanges | 106 |

| 4. The Forward Market in Exchanges | 115viii |

| CHAPTER IV | |

| Alternative Aims in Monetary Policy | 140 |

| 1. Devaluation versus Deflation | 142 |

| 2. Stability of Prices versus Stability of Exchange | 154 |

| 3. The Restoration of a Gold Standard | 163 |

| CHAPTER V | |

| Positive Suggestions for the Future Regulation of Money | 177 |

| 1. Great Britain | 178 |

| 2. The United States | 197 |

| 3. Other Countries | 204 |

| Index | 207 |

[I have utilised, mainly in the first chapter and in parts of the second and third, the material, much revised and re-written, of some articles which were published during 1922 in the Reconstruction Supplements of the Manchester Guardian Commercial.—J. M. K.]

1

Money is only important for what it will procure. Thus a change in the monetary unit, which is uniform in its operation and affects all transactions equally, has no consequences. If, by a change in the established standard of value, a man received and owned twice as much money as he did before in payment for all rights and for all efforts, and if he also paid out twice as much money for all acquisitions and for all satisfactions, he would be wholly unaffected.

It follows, therefore, that a change in the value of money, that is to say in the level of prices, is important to Society only in so far as its incidence is unequal. Such changes have produced in the past, and are producing now, the vastest social consequences, because, as we all know, when the value of money changes, it does not change equally for all persons or for all purposes. A man’s receipts and his outgoings are not all modified in one uniform proportion. Thus a change in prices and rewards,2 as measured in money, generally affects different classes unequally, transfers wealth from one to another, bestows affluence here and embarrassment there, and redistributes Fortune’s favours so as to frustrate design and disappoint expectation.

The fluctuations in the value of money since 1914 have been on a scale so great as to constitute, with all that they involve, one of the most significant events in the economic history of the modern world. The fluctuation of the standard, whether gold, silver, or paper, has not only been of unprecedented violence, but has been visited on a society of which the economic organisation is more dependent than that of any earlier epoch on the assumption that the standard of value would be moderately stable.

During the Napoleonic Wars and the period immediately succeeding them the extreme fluctuation of English prices within a single year was 22 per cent; and the highest price level reached during the first quarter of the nineteenth century, which we used to reckon the most disturbed period of our currency history, was less than double the lowest and with an interval of thirteen years. Compare with this the extraordinary movements of the past nine years. To recall the reader’s mind to the exact facts, I refer him to the table on the next page.

I have not included those countries—Russia, Poland, and Austria—where the old currency has long been bankrupt. But it will be observed that,3 even apart from the countries which have suffered revolution or defeat, no quarter of the world has escaped a violent movement. In the United States, where the gold standard has functioned unabated, in Japan, where the war brought with it more profit than liability, in the neutral country of Sweden, the changes in the value of money have been comparable with those in the United Kingdom.

Index Numbers of Wholesale Prices expressed as a Percentage of 1913 (1).

| Monthly Average. | United Kingdom (2). | France. | Italy. | Germany. | U.S.A. (3). | Canada. | Japan. | Sweden. | India. |

| 1913 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | .. |

| 1914 | 100 | 102 | 96 | 106 | 98 | 100 | 95 | 116 | 100 |

| 1915 | 127 | 140 | 133 | 142 | 101 | 109 | 97 | 145 | 112 |

| 1916 | 160 | 189 | 201 | 153 | 127 | 134 | 117 | 185 | 128 |

| 1917 | 206 | 262 | 299 | 179 | 177 | 175 | 149 | 244 | 147 |

| 1918 | 227 | 340 | 409 | 217 | 194 | 205 | 196 | 339 | 180 |

| 1919 | 242 | 357 | 364 | 415 | 206 | 216 | 239 | 330 | 198 |

| 1920 | 295 | 510 | 624 | 1,486 | 226 | 250 | 260 | 347 | 204 |

| 1921 | 182 | 345 | 577 | 1,911 | 147 | 182 | 200 | 211 | 181 |

| 1922 | 159 | 327 | 562 | 34,182 | 149 | 165 | 196 | 162 | 180 |

| 1923A | 159 | 411 | 582 | 765,000 | 157 | 167 | 192 | 166 | 179 |

(1) These figures are taken from the Monthly Bulletin of Statistics of the League of Nations. (2) Statist up to 1919; thereafter the median of the Economist, Statist, and Board of Trade Index Numbers. (3) Bureau of Labour Index Number (revised).

A First half-year.

From 1914 to 1920 all these countries experienced an expansion in the supply of money to spend relatively to the supply of things to purchase, that is to say Inflation. Since 1920 those countries which have4 regained control of their financial situation, not content with bringing the Inflation to an end, have contracted their supply of money and have experienced the fruits of Deflation. Others have followed inflationary courses more riotously than before. In a few, of which Italy is one, an imprudent desire to deflate has been balanced by the intractability of the financial situation, with the happy result of comparatively stable prices.

Each process, Inflation and Deflation alike, has inflicted great injuries. Each has an effect in altering the distribution of wealth between different classes, Inflation in this respect being the worse of the two. Each has also an effect in overstimulating or retarding the production of wealth, though here Deflation is the more injurious. The division of our subject thus indicated is the most convenient for us to follow,—examining first the effect of changes in the value of money on the distribution of wealth with most of our attention on Inflation, and next their effect on the production of wealth with most of our attention on Deflation. How have the price changes of the past nine years affected the productivity of the community as a whole, and how have they affected the conflicting interests and mutual relations of its component classes? The answer to these questions will serve to establish the gravity of the evils, into the remedy for which it is the object of this book to inquire.

5

For the purpose of this inquiry a triple classification of Society is convenient—into the Investing Class, the Business Class, and the Earning Class. These classes overlap, and the same individual may earn, deal, and invest; but in the present organisation of society such a division corresponds to a social cleavage and an actual divergence of interest.

Of the various purposes which money serves, some essentially depend upon the assumption that its real value is nearly constant over a period of time. The chief of these are those connected, in a wide sense, with contracts for the investment of money. Such contracts—namely, those which provide for the payment of fixed sums of money over a long period of time—are the characteristic of what it is convenient to call the Investment System, as distinct from the property system generally.

Under this phase of capitalism, as developed during the nineteenth century, many arrangements were devised for separating the management of property from its ownership. These arrangements were of three leading types: (1) Those in which the proprietor, while parting with the management6 of his property, retained his ownership of it—i.e. of the actual land, buildings, and machinery, or of whatever else it consisted in, this mode of tenure being typified by a holding of ordinary shares in a joint-stock company; (2) those in which he parted with the property temporarily, receiving a fixed sum of money annually in the meantime, but regained his property eventually, as typified by a lease; and (3) those in which he parted with his real property permanently, in return either for a perpetual annuity fixed in terms of money, or for a terminable annuity and the repayment of the principal in money at the end of the term, as typified by mortgages, bonds, debentures, and preference shares. This third type represents the full development of Investment.

Contracts to receive fixed sums of money at future dates (made without provision for possible changes in the real value of money at those dates) must have existed as long as money has been lent and borrowed. In the form of leases and mortgages, and also of permanent loans to Governments and to a few private bodies, such as the East India Company, they were already frequent in the eighteenth century. But during the nineteenth century they developed a new and increased importance, and had, by the beginning of the twentieth, divided the propertied classes into two groups—the “business men” and the “investors”—with partly divergent7 interests. The division was not sharp as between individuals; for business men might be investors also, and investors might hold ordinary shares; but the division was nevertheless real, and not the less important because it was seldom noticed.

By this system the active business class could call to the aid of their enterprises not only their own wealth but the savings of the whole community; and the professional and propertied classes, on the other hand, could find an employment for their resources, which involved them in little trouble, no responsibility, and (it was believed) small risk.

For a hundred years the system worked, throughout Europe, with an extraordinary success and facilitated the growth of wealth on an unprecedented scale. To save and to invest became at once the duty and the delight of a large class. The savings were seldom drawn on, and, accumulating at compound interest, made possible the material triumphs which we now all take for granted. The morals, the politics, the literature, and the religion of the age joined in a grand conspiracy for the promotion of saving. God and Mammon were reconciled. Peace on earth to men of good means. A rich man could, after all, enter into the Kingdom of Heaven—if only he saved. A new harmony sounded from the celestial spheres. “It is curious to observe how, through the wise and beneficent arrangement of Providence, men thus do the greatest service to the public, when they are8 thinking of nothing but their own gain”1; so sang the angels.

1 Easy Lessons on Money Matters for the Use of Young People. Published by the Society for Promoting Christian Knowledge. Twelfth Edition, 1850.

The atmosphere thus created well harmonised the demands of expanding business and the needs of an expanding population with the growth of a comfortable non-business class. But amidst the general enjoyment of ease and progress, the extent, to which the system depended on the stability of the money to which the investing classes had committed their fortunes, was generally overlooked; and an unquestioning confidence was apparently felt that this matter would look after itself. Investments spread and multiplied, until, for the middle classes of the world, the gilt-edged bond came to typify all that was most permanent and most secure. So rooted in our day has been the conventional belief in the stability and safety of a money contract that, according to English law, trustees have been encouraged to embark their trust funds exclusively in such transactions, and are indeed forbidden, except in the case of real estate (an exception which is itself a survival of the conditions of an earlier age), to employ them otherwise.2

2 German trustees were not released from a similar obligation until 1923, by which date the value of trust funds invested in titles to money had entirely disappeared.

As in other respects, so also in this, the nineteenth century relied on the future permanence of its own9 happy experiences and disregarded the warning of past misfortunes. It chose to forget that there is no historical warrant for expecting money to be represented even by a constant quantity of a particular metal, far less by a constant purchasing power. Yet Money is simply that which the State declares from time to time to be a good legal discharge of money contracts. In 1914 gold had not been the English standard for a century or the sole standard of any other country for half a century. There is no record of a prolonged war or a great social upheaval which has not been accompanied by a change in the legal tender, but an almost unbroken chronicle in every country which has a history, back to the earliest dawn of economic record, of a progressive deterioration in the real value of the successive legal tenders which have represented money.

Moreover, this progressive deterioration in the value of money through history is not an accident, and has had behind it two great driving forces—the impecuniosity of Governments and the superior political influence of the debtor class.

The power of taxation by currency depreciation is one which has been inherent in the State since Rome discovered it. The creation of legal-tender has been and is a Government’s ultimate reserve; and no State or Government is likely to decree its own bankruptcy or its own downfall, so long as this instrument still lies at hand unused.

10

Besides this, as we shall see below, the benefits of a depreciating currency are not restricted to the Government. Farmers and debtors and all persons liable to pay fixed money dues share in the advantage. As now in the persons of business men, so also in former ages these classes constituted the active and constructive elements in the economic scheme. Those secular changes, therefore, which in the past have depreciated money, assisted the new men and emancipated them from the dead hand; they benefited new wealth at the expense of old, and armed enterprise against accumulation. The tendency of money to depreciate has been in past times a weighty counterpoise against the cumulative results of compound interest and the inheritance of fortunes. It has been a loosening influence against the rigid distribution of old-won wealth and the separation of ownership from activity. By this means each generation can disinherit in part its predecessors’ heirs; and the project of founding a perpetual fortune must be disappointed in this way, unless the community with conscious deliberation provides against it in some other way, more equitable and more expedient.

At any rate, under the influence of these two forces—the financial necessities of Governments and the political influence of the debtor class—sometimes the one and sometimes the other, the progress of inflation has been continuous, if we consider long11 periods, ever since money was first devised in the sixth century B.C. Sometimes the standard of value has depreciated of itself; failing this, debasements have done the work.

Nevertheless it is easy at all times, as a result of the way we use money in daily life, to forget all this and to look on money as itself the absolute standard of value; and when, besides, the actual events of a hundred years have not disturbed his illusions, the average man regards what has been normal for three generations as a part of the permanent social fabric.

The course of events during the nineteenth century favoured such ideas. During its first quarter, the very high prices of the Napoleonic Wars were followed by a somewhat rapid improvement in the value of money. For the next seventy years, with some temporary fluctuations, the tendency of prices continued to be downwards, the lowest point being reached in 1896. But while this was the tendency as regards direction, the remarkable feature of this long period was the relative stability of the price level. Approximately the same level of price ruled in or about the years 1826, 1841, 1855, 1862, 1867, 1871, and 1915. Prices were also level in the years 1844, 1881, and 1914. If we call the index number of these latter years 100, we find that, for the period of close on a century from 1826 to the outbreak of war, the maximum fluctuation in either direction was12 30 points, the index number never rising above 130 and never falling below 70. No wonder that we came to believe in the stability of money contracts over a long period. The metal gold might not possess all the theoretical advantages of an artificially regulated standard, but it could not be tampered with and had proved reliable in practice.

At the same time, the investor in Consols in the early part of the century had done very well in three different ways. The “security” of his investment had come to be considered as near absolute perfection as was possible. Its capital value had uniformly appreciated, partly for the reason just stated, but chiefly because the steady fall in the rate of interest increased the number of years’ purchase of the annual income which represented the capital.3 And the annual money income had a purchasing power which on the whole was increasing. If, for example, we consider the seventy years from 1826 to 1896 (and ignore the great improvement immediately after Waterloo), we find that the capital value of Consols rose steadily, with only temporary set-backs, from 79 to 109 (in spite of Goschen’s conversion from a 3 per cent rate to a 2¾ per cent rate in 1889 and a 2½ per cent rate effective in 1903), while the purchasing power of the annual dividends, even after allowing for the reduced rates of interest, had increased 50 per13 cent. But Consols, too, had added the virtue of stability to that of improvement. Except in years of crisis Consols never fell below 90 during the reign of Queen Victoria; and even in ’48, when thrones were crumbling, the mean price of the year fell but 5 points. Ninety when she ascended the throne, they reached their maximum with her in the year of Diamond Jubilee. What wonder that our parents thought Consols a good investment!

3 If (for example) the rate of interest falls from 4½ per cent to 3 per cent, 3 per cent Consols rise in value from 66 to 100.

Thus there grew up during the nineteenth century a large, powerful, and greatly respected class of persons, well-to-do individually and very wealthy in the aggregate, who owned neither buildings, nor land, nor businesses, nor precious metals, but titles to an annual income in legal-tender money. In particular, that peculiar creation and pride of the nineteenth century, the savings of the middle class, had been mainly thus embarked. Custom and favourable experience had acquired for such investments an unimpeachable reputation for security.

Before the war these medium fortunes had already begun to suffer some loss (as compared with the summit of their prosperity in the middle ’nineties) from the rise in prices and also in the rate of interest. But the monetary events which have accompanied and have followed the war have taken from them about one-half of their real value in England, seven-eighths in France, eleven-twelfths14 in Italy, and virtually the whole in Germany and in the succession states of Austria-Hungary and Russia.

The loss to the typical English investor of the pre-war period is sufficiently measured by the loss to the investor in Consols. Such an investor, as we have already seen, was steadily improving his position, apart from temporary fluctuations, up to 1896, and in this and the following year two maxima were reached simultaneously—both the capital value of an annuity and also the purchasing power of money. Between 1896 and 1914, on the other hand, the investor had already suffered a serious loss—the capital value of his annuity had fallen by about a third, and the purchasing power of his income had also fallen by nearly a third. This loss, however, was incurred gradually over a period of nearly twenty years from an exceptional maximum, and did not leave him appreciably worse off than he had been in the early ’eighties or the early ’forties. But upon the top of this came the further swifter loss of the war period. Between 1914 and 1920 the capital value of the investor’s annuity again fell by more than a third, and the purchasing power of his income by about two-thirds. In addition, the standard rate of income tax rose from 7½ per cent in 1914 to 30 per cent in 1921.4 Roughly estimated in round numbers, the change may be represented thus in15 terms of an index of which the base year is 1914:

4 Since 1896 there has been the further burden of the Death Duties.

| Purchasing Power of the Income of Consols.5 | Do. after deduction of Income Tax at the standard rate. | Money price of the capital value of Consols. | Purchasing Power of the capital value of Consols. | |

| 1815 | 61 | 59 | 92 | 56 |

| 1826 | 85 | 90 | 108 | 92 |

| 1841 | 85 | 90 | 122 | 104 |

| 1869 | 87 | 89 | 127 | 111 |

| 1883 | 104 | 108 | 138 | 144 |

| 1896 | 139 | 145 | 150 | 208 |

| 1914 | 100 | 100 | 100 | 100 |

| 1920 | 34 | 26 | 64 | 22 |

| 1921 | 53 | 39 | 56 | 34 |

| 1922 | 62 | 50 | 76 | 47 |

5 Without allowance for the reduction of the interest from 3 to 2½ per cent.

The second column well illustrates what a splendid investment gilt-edged stocks had been through the century from Waterloo to Mons, even if we omit altogether the abnormal values of 1896–97. Our table shows how the epoch of Diamond Jubilee was the culminating moment in the prosperity of the British middle class. But it also exhibits with the precision of figures the familiar bewailed plight of those who try to live on the income of the same trustee investments as before the war. The owner of consols in 1922 had a real income, one half of what he had in 1914 and one third of what he had in 1896. The whole of the improvement of the nineteenth century had been obliterated, and his16 situation was not quite so good as it had been after Waterloo.

Some mitigating circumstances should not be overlooked. Whilst the war was a period of the dissipation of the community’s resources as a whole, it was a period of saving for the individuals of the saving class, who with their larger holdings of the securities of the Government now have an increased aggregate money claim on the receipts of the Exchequer. Also, the investing class, which has lost money, overlaps, both socially and by the ties of family, with the business class, which has made money, sufficiently to break in many cases the full severity of the loss. Moreover, in England, there has been a substantial recovery from the low point of 1920.

But these things do not wash away the significance of the facts. The effect of the war, and of the monetary policy which has accompanied and followed it, has been to take away a large part of the real value of the possessions of the investing class. The loss has been so rapid and so intermixed in the time of its occurrence with other worse losses that its full measure is not yet separately apprehended. But it has effected, nevertheless, a far-reaching change in the relative position of different classes. Throughout the Continent the pre-war savings of the middle class, so far as they were invested in bonds, mortgages, or bank deposits, have been largely or entirely wiped out. Nor can it be doubted that this experience must17 modify social psychology towards the practice of saving and investment. What was deemed most secure has proved least so. He who neither spent nor “speculated,” who made “proper provision for his family,” who sang hymns to security and observed most straitly the morals of the edified and the respectable injunctions of the worldly-wise,—he, indeed, who gave fewest pledges to Fortune has yet suffered her heaviest visitations.

What moral for our present purpose should we draw from this? Chiefly, I think, that it is not safe or fair to combine the social organisation developed during the nineteenth century (and still retained) with a laisser-faire policy towards the value of money. It is not true that our former arrangements have worked well. If we are to continue to draw the voluntary savings of the community into “investments,” we must make it a prime object of deliberate State policy that the standard of value, in terms of which they are expressed, should be kept stable; adjusting in other ways (calculated to touch all forms of wealth equally and not concentrated on the relatively helpless “investors”) the redistribution of the national wealth, if, in course of time, the laws of inheritance and the rate of accumulation have drained too great a proportion of the income of the active classes into the spending control of the inactive.

18

It has long been recognised, by the business world and by economists alike, that a period of rising prices acts as a stimulus to enterprise and is beneficial to business men.

In the first place there is the advantage which is the counterpart of the loss to the investing class which we have just examined. When the value of money falls, it is evident that those persons who have engaged to pay fixed sums of money yearly out of the profits of active business must benefit, since their fixed money outgoings will bear a smaller proportion than formerly to their money turnover. This benefit persists not only during the transitional period of change, but also, so far as old loans are concerned, when prices have settled down at their new and higher level. For example, the farmers throughout Europe, who had raised by mortgage the funds to purchase the land they farmed, now find themselves almost freed from the burden at the expense of the mortgagees.

But during the period of change, while prices are rising month by month, the business man has a further and greater source of windfall. Whether he is a merchant or a manufacturer, he will generally buy before he sells, and on at least a part of his stock he will run the risk of price changes. If, therefore, month after month his stock appreciates on his hands, he is always selling at a better price than he19 expected and securing a windfall profit upon which he had not calculated. In such a period the business of trade becomes unduly easy. Any one who can borrow money and is not exceptionally unlucky must make a profit, which he may have done little to deserve. The continuous enjoyment of such profits engenders an expectation of their renewal. The practice of borrowing from banks is extended beyond what is normal. If the market expects prices to rise still further, it is natural that stocks of commodities should be held speculatively for the rise, and for a time the mere expectation of a rise is sufficient, by inducing speculative purchases, to produce one.

Take, for example, the Statist index number for raw materials month by month from April, 1919, to March, 1920:

| April, 1919 | 100 |

| May | 108 |

| June | 112 |

| July | 117 |

| August | 120 |

| September | 121 |

| October | 127 |

| November | 131 |

| December | 135 |

| January, 1920 | 142 |

| February | 150 |

| March | 146 |

It follows from this table that a man, who borrowed money from his banker and used the proceeds to purchase raw materials selected at random, stood to make a profit in every single month of this period with the exception of the last, and would have cleared 46 per cent on the average of the year. Yet bankers were not charging at this time above 7 per cent for their advances, leaving a clear profit of between20 30 and 40 per cent per annum, without the exercise of any particular skill, to any person lucky enough to have embarked on these courses. How much more were the opportunities of persons whose business position and expert knowledge enabled them to exercise intelligent anticipation as to the probable course of prices of particular commodities! Yet any dealer in or user of raw materials on a large scale who knew his trade was thus situated. The profits of certain kinds of business to the man who has a little skill or some luck are certain in such a period to be inordinate. Great fortunes may be made in a few months. But apart from all such, the steady-going business man, who would be pained and insulted at the thought of being designated speculator or profiteer, may find windfall profits dropping into his lap which he has neither sought nor desired.

Economists draw an instructive distinction between what are termed the “money” rate of interest and the “real” rate of interest. If a sum of money worth 100 in terms of commodities at the time when the loan is made is lent for a year at 5 per cent interest, and is only worth 90 in terms of commodities at the end of the year, the lender receives back, including his interest, what is only worth 94½. This is expressed by saying that while the money rate of interest was 5 per cent, the real rate of interest had actually been negative and equal to minus 5½ per cent. In the same way, if at the end of the period the value of21 money had risen and the capital sum lent had come to be worth 110 in terms of commodities, while the money rate of interest would still be 5 per cent the real rate of interest would have been 15½ per cent.

Such considerations, even though they are not explicitly present to the minds of the business world, are far from being academic. The business world may speak, and even think, as though the money rate of interest could be considered by itself, without reference to the real rate. But it does not act so. The merchant or manufacturer, who is calculating whether a 7 per cent bank rate is so onerous as to compel him to curtail his operations, is very much influenced by his anticipations about the prospective price of the commodity in which he is interested.

Thus, when prices are rising, the business man who borrows money is able to repay the lender with what, in terms of real value, not only represents no interest, but is even less than the capital originally advanced; that is, the real rate of interest falls to a negative value, and the borrower reaps a corresponding benefit. It is true that, in so far as a rise of prices is foreseen, attempts to get advantage from this by increased borrowing force the money rates of interest to move upwards. It is for this reason, amongst others, that a high bank rate should be associated with a period of rising prices, and a low bank rate with a period of falling prices. The apparent abnormality of the money rate of interest22 at such times is merely the other side of the attempt of the real rate of interest to steady itself. Nevertheless in a period of rapidly changing prices, the money rate of interest seldom adjusts itself adequately or fast enough to prevent the real rate from becoming abnormal. For it is not the fact of a given rise of prices, but the expectation of a rise compounded of the various possible price-movements and the estimated probability of each, which affects money rates; and in countries where the currency has not collapsed completely, there has seldom or never existed a sufficient general confidence in a further rise or fall of prices to cause the short-money rate of interest to rise above 10 per cent per annum, or to fall below 1 per cent.6 A fluctuation of this order is not sufficient to balance a movement of prices, up or down, of more than (say) 5 per cent per annum,—a rate which the actual price movement has frequently exceeded.

6 The merchant, who borrows money in order to take advantage of a prospective high real rate of interest, has to act in advance of the rise in prices, and is calculating on a probability, not upon a certainty, with the result that he will be deterred by a movement in the money rate of interest of much less magnitude than the contrary movement in the real rate of interest, upon which indeed he is reckoning, yet is not reckoning with certainty.

Germany has recently provided an illustration of the extraordinary degree in which the money rate of interest can rise in its endeavour to keep up with the real rate, when prices have continued to rise for so long and with such violence that, rightly or23 wrongly, every one believes that they will continue to rise further. Yet even there the money rate of interest has never risen high enough to keep pace with the rise of prices. In the autumn of 1922, the full effects were just becoming visible of the long preceding period during which the real rate of interest in Germany had reached a high negative figure, that is to say during which any one who could borrow marks and turn them into assets would have found at the end of any given period that the appreciation in the mark-value of the assets was far greater than the interest he had to pay for borrowing them. By this means great fortunes were snatched out of general calamity; and those made most who had seen first, that the right game was to borrow and to borrow and to borrow, and thus secure the difference between the real rate of interest and the money rate. But after this had been good business for many months, every one began to take a hand, with belated results on the money rate of interest. At that time, with a nominal Reichsbank rate of 8 per cent, the effective gilt-edged rate for short loans had risen to 22 per cent per annum. During the first half of 1923, the rate of the Reichsbank itself rose to 24 per cent, and subsequently to 30, and finally 108 per cent, whilst the market rate fluctuated violently at preposterous figures, reaching at times 3 per cent per week for certain types of loan. With the final currency collapse of July-September 1923, the open market24 rate was altogether demoralised, and reached figures of 100 per cent per month. In face, however, of the rate of currency depreciation, even such figures were inadequate, and the bold borrower was still making money.

In Hungary, Poland, and Russia—wherever prices were expected to collapse yet further—the same phenomenon was present, exhibiting as through a microscope what takes place everywhere when prices are expected to rise.

On the other hand, when prices are falling 30 to 40 per cent between the average of one year and that of the next, as they were in Great Britain and in the United States during 1921, even a bank rate of 1 per cent would have been oppressive to business, since it would have corresponded to a very high rate of real interest. Any one who could have foreseen the movement even partially would have done well for himself by selling out his assets and staying out of business for the time being.

But if the depreciation of money is a source of gain to the business man, it is also the occasion of opprobrium. To the consumer the business man’s exceptional profits appear as the cause (instead of the consequence) of the hated rise of prices. Amidst the rapid fluctuations of his fortunes he himself loses his conservative instincts, and begins to think more of the large gains of the moment than of the lesser, but permanent, profits of normal business. The welfare25 of his enterprise in the relatively distant future weighs less with him than before, and thoughts are excited of a quick fortune and clearing out. His excessive gains have come to him unsought and without fault or design on his part, but once acquired he does not lightly surrender them, and will struggle to retain his booty. With such impulses and so placed, the business man is himself not free from a suppressed uneasiness. In his heart he loses his former self-confidence in his relation to society, in his utility and necessity in the economic scheme. He fears the future of his business and his class, and the less secure he feels his fortune to be the tighter he clings to it. The business man, the prop of society and the builder of the future, to whose activities and rewards there had been accorded, not long ago, an almost religious sanction, he of all men and classes most respectable, praiseworthy and necessary, with whom interference was not only disastrous but almost impious, was now to suffer sidelong glances, to feel himself suspected and attacked, the victim of unjust and injurious laws,—to become, and know himself half-guilty, a profiteer.

No man of spirit will consent to remain poor if he believes his betters to have gained their goods by lucky gambling. To convert the business man into the profiteer is to strike a blow at capitalism, because it destroys the psychological equilibrium26 which permits the perpetuance of unequal rewards. The economic doctrine of normal profits, vaguely apprehended by every one, is a necessary condition for the justification of capitalism. The business man is only tolerable so long as his gains can be held to bear some relation to what, roughly and in some sense, his activities have contributed to society.

This, then, is the second disturbance to the existing economic order for which the depreciation of money is responsible. If the fall in the value of money discourages investment, it also discredits enterprise.

Not that the business man was allowed, even during the period of boom, to retain the whole of his exceptional profits. A host of popular remedies vainly attempted to cure the evils of the day; which remedies themselves—subsidies, price and rent fixing, profiteer hunting, and excess profits duties—eventually became not the least part of the evils.

In due course came the depression, with falling prices, which operate on those who hold stocks in a manner exactly opposite to rising prices. Excessive losses, bearing no relation to the efficiency of the business, took the place of windfall gains; and the effort of every one to hold as small stocks as possible brought industry to a standstill, just as previously their efforts to accumulate stocks had over-stimulated it. Unemployment succeeded Profiteering as the27 problem of the hour. But whilst the cyclical movement of trade and credit has, in the good-currency countries, partly reversed, for the time being at least, the great rise of 1920, it has, in the countries of continuing inflation, made no more than a ripple on the rapids of depreciation.

It has been a commonplace of economic text-books that wages tend to lag behind prices, with the result that the real earnings of the wage-earner are diminished during a period of rising prices. This has often been true in the past, and may be true even now of certain classes of labour which are ill-placed or ill-organised for improving their position. But in Great Britain, at any rate, and in the United States also, some important sections of labour were able to take advantage of the situation not only to obtain money wages equivalent in purchasing power to what they had before, but to secure a real improvement, to combine this with a diminution in their hours of work (and, so far, of the work done), and to accomplish this (in the case of Great Britain) at a time when the total wealth of the community as a whole had suffered a decrease. This reversal of the usual course has not been due to an accident and is traceable to definite causes.

The organisation of certain classes of labour—railwaymen, miners, dockers, and others—for the28 purpose of securing wage increases is better than it was. Life in the army, perhaps for the first time in the history of wars, raised in many respects the conventional standard of requirements,—the soldier was better clothed, better shod, and often better fed than the labourer, and his wife, adding in war time a separation allowance to new opportunities to earn, had also enlarged her ideas.

But these influences, while they would have supplied the motive, might have lacked the means to the result if it had not been for another factor—the windfalls of the profiteer. The fact that the business man had been gaining, and gaining notoriously, considerable windfall profits in excess of the normal profits of trade, laid him open to pressure, not only from his employees but from public opinion generally; and enabled him to meet this pressure without financial difficulty. In fact, it was worth his while to pay ransom, and to share with his workmen the good fortune of the day.

Thus the working classes improved their relative position in the years following the war, as against all other classes except that of the “profiteers.” In some important cases they improved their absolute position—that is to say, account being taken of shorter hours, increased money wages, and higher prices, some sections of the working classes secured for themselves a higher real remuneration for each unit of effort or work done. But we cannot estimate29 the stability of this state of affairs, as contrasted with its desirability, unless we know the source from which the increased reward of the working classes was drawn. Was it due to a permanent modification of the economic factors which determine the distribution of the national product between different classes? Or was it due to some temporary and exhaustible influence connected with inflation and with the resulting disturbance in the standard of value?

A violent disturbance of the standard of value obscures the true situation, and for a time one class can benefit at the expense of another surreptitiously and without producing immediately the inevitable reaction. In such conditions a country can without knowing it expend in current consumption those savings which it thinks it is investing for the future; and it can even trench on existing capital or fail to make good its current depreciation. When the value of money is greatly fluctuating, the distinction between capital and income becomes confused. It is one of the evils of a depreciating currency that it enables a community to live on its capital unawares. The increasing money value of the community’s capital goods obscures temporarily a diminution in the real quantity of the stock.

The period of depression has exacted its penalty from the working classes more in the form of unemployment than by a lowering of real wages, and State assistance to the unemployed has greatly30 moderated even this penalty. Money wages have followed prices downwards. But the depression of 1921–22 did not reverse or even greatly diminish the relative advantage gained by the working classes over the middle class during the previous years. In 1923 British wage rates stood at an appreciably higher level above the pre-war rates than did the cost of living, if allowance is made for the shorter hours worked.

In Germany and Austria also, but in a far greater degree than in England or in France, the change in the value of money has thrown the burden of hard circumstances on the middle class, and hitherto the labouring class have by no means supported their full proportionate share. If it be true that university professors in Germany have some responsibility for the atmosphere which bred war, their class has paid the penalty. The effects of the impoverishment, throughout Europe, of the middle class, out of which most good things have sprung, must slowly accumulate in a decay of Science and Art.

We conclude that Inflation redistributes wealth in a manner very injurious to the investor, very beneficial to the business man, and probably, in modern industrial conditions, beneficial on the whole to the earner. Its most striking consequence is its injustice to those who in good faith have committed31 their savings to titles to money rather than to things. But injustice on such a scale has further consequences. The above discussion suggests that the diminution in the production of wealth which has taken place in Europe since the war has been, to a certain extent, at the expense, not of the consumption of any class, but of the accumulation of capital. Moreover, Inflation has not only diminished the capacity of the investing class to save but has destroyed the atmosphere of confidence which is a condition of the willingness to save. Yet a growing population requires, for the maintenance of the same standard of life, a proportionate growth of capital. In Great Britain for many years to come, regardless of what the birth-rate may be from now onwards (and at the present time the number of births per day is nearly double the number of deaths), upwards of 250,000 new labourers will enter the labour market annually in excess of those going out of it. To maintain this growing body of labour at the same standard of life as before, we require not merely growing markets but a growing capital equipment. In order to keep our standards from deterioration, the national capital must grow as fast as the national labour supply, which means new savings of at least £250,000,0007 per annum at present.32 The favourable conditions for saving which existed in the nineteenth century, even though we smile at them, provided a proportionate growth between capital and population. The disturbance of the pre-existing balance between classes, which in its origins is largely traceable to the changes in the value of money, may have destroyed these favourable conditions.

7 That is to say, it costs not less than £1000 in new capital outlay to equip a working man with organisation and appliances, which will render his labour efficient, and to house and supply himself and his family. Indeed this is probably an underestimate.

On the other hand Deflation, as we shall see in the second section of the next chapter, is liable, in these days of huge national debts expressed in legal-tender money, to overturn the balance so far the other way in the interests of the rentier, that the burden of taxation becomes intolerable on the productive classes of the community.

If, for any reason right or wrong, the business world expects that prices will fall, the processes of production tend to be inhibited; and if it expects that prices will rise, they tend to be over-stimulated. A fluctuation in the measuring-rod of value does not alter in the least the wealth of the world, the needs of the world, or the productive capacity of the world. It ought not, therefore, to affect the character or the volume of what is produced. A movement of relative prices, that is to say of the comparative prices of33 different commodities, ought to influence the character of production, because it is an indication that various commodities are not being produced in the exactly right proportions. But this is not true of a change, as such, in the general price level.

The fact that the expectation of changes in the general price level affects the processes of production, is deeply rooted in the peculiarities of the existing economic organisation of society, partly in those described in the preceding sections of this chapter, partly in others to be mentioned in a moment. We have already seen that a change in the general level of prices, that is to say a change in the measuring-rod, which fixes the obligation of the borrowers of money (who make the decisions which set production in motion) to the lenders (who are inactive once they have lent their money), effects a redistribution of real wealth between the two groups. Furthermore, the active group can, if they foresee such a change, alter their action in advance in such a way as to minimise their losses to the other group or to increase their gains from it, if and when the expected change in the value of money occurs. If they expect a fall, it may pay them, as a group, to damp production down, although such enforced idleness impoverishes society as a whole. If they expect a rise, it may pay them to increase their borrowings and to swell production beyond the point where the real return is just sufficient to recompense society as a whole for the effort made.34 Sometimes, of course, a change in the measuring-rod, especially if it is unforeseen, may benefit one group at the expense of the other disproportionately to any influence it exerts on the volume of production; but the tendency, in so far as the active group anticipate a change, will be as I have described it.8 This is simply to say that the intensity of production is largely governed in existing conditions by the anticipated real profit of the entrepreneur. Yet this criterion is the right one for the community as a whole only when the delicate adjustment of interests is not upset by fluctuations in the standard of value.

8 The interests of the salaried and wage-earning classes will, in so far as their salaries and wages tend to be steadier in money-value than in real-value, coincide with those of the inactive capitalist group. The interests of the consumer will, in so far as he can vary the distribution of his floating resources between cash and goods purchased in advance of consumption, coincide with those of the active capitalist group; and his decisions, made in his own interests, may serve to reinforce the effect of those of the latter. But that the interests of the same individual will often be those of one of the groups in one of his capacities and of the other in another of his capacities, does not save the situation or affect the argument. For his losses in one capacity depend only infinitesimally on him personally refraining from action in his other capacity. The facts, that a man is a cannibal at home and eaten abroad, do not cancel out to render him innocuous and safe.

But there is a further reason, connected with the above but nevertheless distinct, why modern methods of production require a stable standard,—a reason springing to a certain extent out of the character of the social organisation described above, but aggravated by the technical methods of present-day productive processes. With the development of international trade, involving great distances between35 the place of original production and the place of final consumption, and with the increased complication of the technical processes of manufacture, the amount of risk which attaches to the undertaking of production and the length of time through which this risk must be carried are much greater than they would be in a comparatively small self-contained community. Even in agriculture, whilst the risk to the consumer is diminished by drawing supplies from many different sources, which average the fluctuations of the seasons, the risk to the agricultural producer is increased, since, when his crop falls below his expectations in volume, he may fail to be compensated by a higher price. This increased risk is the price which producers have to pay for the other advantages of a high degree of specialisation and for the variety of their markets and their sources of supply.

The provision of adequate facilities for the carrying of this risk at a moderate cost is one of the greatest of the problems of modern economic life, and one of those which so far have been least satisfactorily solved. The business of keeping the productive machine in continuous operation (and thereby avoiding unemployment) would be greatly simplified if this risk could be diminished or if we could devise a better means of insurance against it for the individual entrepreneur.

A considerable part of the risk arises out of fluctuations in the relative value of a commodity compared with that of commodities in general during the interval36 which must elapse between the commencement of production and the time of consumption. This part of the risk is independent of the vagaries of money, and must be tackled by methods with which we are not concerned here. But there is also a considerable risk directly arising out of instability in the value of money. During the lengthy process of production the business world is incurring outgoings in terms of money—paying out in money for wages and other expenses of production—in the expectation of recouping this outlay by disposing of the product for money at a later date. That is to say, the business world as a whole must always be in a position where it stands to gain by a rise of price and to lose by a fall of price. Whether it likes it or not, the technique of production under a régime of money-contract forces the business world always to carry a big speculative position; and if it is reluctant to carry this position, the productive process must be slackened. The argument is not affected by the fact that there is some degree of specialisation of function within the business world, in so far as the professional speculator comes to the assistance of the producer proper by taking over from him a part of his risk.

Now it follows from this, not merely that the actual occurrence of price changes profits some classes and injures others (which has been the theme of the first section of this chapter), but that a general fear of falling prices may inhibit the productive process37 altogether. For if prices are expected to fall, not enough risk-takers can be found who are willing to carry a speculative “bull” position, and this means that entrepreneurs will be reluctant to embark on lengthy productive processes involving a money outlay long in advance of money recoupment,—whence unemployment. The fact of falling prices injures entrepreneurs; consequently the fear of falling prices causes them to protect themselves by curtailing their operations; yet it is upon the aggregate of their individual estimations of the risk, and their willingness to run the risk, that the activity of production and of employment mainly depends.

There is a further aggravation of the case, in that an expectation about the course of prices tends, if it is widely held, to be cumulative in its results up to a certain point. If prices are expected to rise and the business world acts on this expectation, that very fact causes them to rise for a time and, by verifying the expectation, reinforces it; and similarly, if it expects them to fall. Thus a comparatively weak initial impetus may be adequate to produce a considerable fluctuation.

Three generations of economists have recognised that certain influences produce a progressive and continuing change in the value of money, that others produce in it an oscillatory movement, and that the latter act cumulatively in their initial stages but produce the conditions for a reaction after a certain38 point. But their investigations into the oscillatory movements have been chiefly confined, until lately, to the question what kind of cause is responsible for the initial impetus. Some have been fascinated by the idea that the initial cause is always the same and is astronomically regular in the times of its appearance. Others have maintained, more plausibly, that sometimes one thing operates and sometimes another.

It is one of the objects of this book to urge that the best way to cure this mortal disease of individualism is to provide that there shall never exist any confident expectation either that prices generally are going to fall or that they are going to rise; and also that there shall be no serious risk that a movement, if it does occur, will be a big one. If, unexpectedly and accidentally, a moderate movement were to occur, wealth, though it might be redistributed, would not be diminished thereby.

To procure this result by removing all possible influences towards an initial movement, whether such influences are to be found in the skies only or everywhere, would seem to be a hopeless enterprise. The remedy would lie, rather, in so controlling the standard of value that, whenever something occurred which, left to itself, would create an expectation of a change in the general level of prices, the controlling authority should take steps to counteract this expectation by setting in motion some factor of a contrary tendency. Even if such a policy were not wholly successful,39 either in counteracting expectations or in avoiding actual movements, it would be an improvement on the policy of sitting quietly by, whilst a standard of value, governed by chance causes and deliberately removed from central control, produces expectations which paralyse or intoxicate the government of production.

We see, therefore, that rising prices and falling prices each have their characteristic disadvantage. The Inflation which causes the former means Injustice to individuals and to classes,—particularly to investors; and is therefore unfavourable to saving. The Deflation which causes falling prices means Impoverishment to labour and to enterprise by leading entrepreneurs to restrict production, in their endeavour to avoid loss to themselves; and is therefore disastrous to employment. The counterparts are, of course, also true,—namely that Deflation means Injustice to borrowers, and that Inflation leads to the over-stimulation of industrial activity. But these results are not so marked as those emphasised above, because borrowers are in a better position to protect themselves from the worst effects of Deflation than lenders are to protect themselves from those of Inflation, and because labour is in a better position to protect itself from over-exertion in good times than from under-employment in bad times.

40

Thus Inflation is unjust and Deflation is inexpedient. Of the two perhaps Deflation is, if we rule out exaggerated inflations such as that of Germany, the worse; because it is worse, in an impoverished world, to provoke unemployment than to disappoint the rentier. But it is not necessary that we should weigh one evil against the other. It is easier to agree that both are evils to be shunned. The Individualistic Capitalism of to-day, precisely because it entrusts saving to the individual investor and production to the individual employer, presumes a stable measuring-rod of value, and cannot be efficient—perhaps cannot survive—without one.

For these grave causes we must free ourselves from the deep distrust which exists against allowing the regulation of the standard of value to be the subject of deliberate decision. We can no longer afford to leave it in the category of which the distinguishing characteristics are possessed in different degrees by the weather, the birth-rate, and the Constitution,—matters which are settled by natural causes, or are the resultant of the separate action of many individuals acting independently, or require a Revolution to change them.

41

A Government can live for a long time, even the German Government or the Russian Government, by printing paper money. That is to say, it can by this means secure the command over real resources,—resources just as real as those obtained by taxation. The method is condemned, but its efficacy, up to a point, must be admitted. A Government can live by this means when it can live by no other. It is the form of taxation which the public find hardest to evade and even the weakest Government can enforce, when it can enforce nothing else. Of this character have been the progressive and catastrophic inflations practised in Central and Eastern Europe, as distinguished from the limited and oscillatory inflations, experienced for example in Great Britain and the United States, which have been examined in the preceding chapter.

The Quantity Theory of Money states that the42 amount of cash which the community requires, assuming certain habits of business and of banking to be established, and assuming also a given level and distribution of wealth, depends on the level of prices. If the consumption and production of actual goods are unaltered but prices and wages are doubled, then twice as much cash as before is required to do the business. The truth of this, properly explained and qualified, it is foolish to deny. The Theory infers from this that the aggregate real value of all the paper money in circulation remains more or less the same, irrespective of the number of units of it in circulation, provided the habits and prosperity of the people are not changed,—i.e. the community retains in the shape of cash the command over a more or less constant amount of real wealth, which is the same thing as to say that the total quantity of money in circulation has a more or less fixed purchasing power.9

Let us suppose that there are in circulation 9,000,000 currency notes, and that they have altogether a value equivalent to 36,000,000 gold dollars.10 Suppose that the Government prints a further 3,000,000 notes, so that the amount of currency is now 12,000,000; then, in accordance with the above theory, the 12,000,000 notes are still43 only equivalent to $36,000,000. In the first state of affairs, therefore, each note = $4, and in the second state of affairs each note = $3. Consequently the 9,000,000 notes originally held by the public are now worth $27,000,000 instead of $36,000,000, and the 3,000,000 notes newly issued by the Government are worth $9,000,000. Thus by the process of printing the additional notes the Government has transferred from the public to itself an amount of resources equal to $9,000,000, just as successfully as if it had raised this sum in taxation.

10 It will simplify the argument to ignore the fact that the value of gold in terms of commodities is itself a fluctuating one, and to treat the value of a currency in terms of gold as a rough measure of its value in terms of “real resources” generally.

On whom has the tax fallen? Clearly on the holders of the original 9,000,000 notes, whose notes are now worth 25 per cent less than they were before. The inflation has amounted to a tax of 25 per cent on all holders of notes in proportion to their holdings. The burden of the tax is well spread, cannot be evaded, costs nothing to collect, and falls, in a rough sort of way, in proportion to the wealth of the victim. No wonder its superficial advantages have attracted Ministers of Finance.

Temporarily, the yield of the tax is even a little better for the Government than by the above calculation. For the new notes can be passed off at first at the same value as though there were still only 9,000,000 notes altogether. It is only after the new notes get into circulation and people begin to spend them that they realise that the notes are worth less than before.

44

What is there to prevent the Government from repeating this process over and over again? The reader must observe that the aggregate note issue is still worth $36,000,000. If, therefore, the Government now prints a further 4,000,000 notes, there will be 16,000,000 notes altogether, which by the same argument as before are worth $2.25 each instead of $3, and by issuing the 4,000,000 notes the Government has, just as before, transferred an amount of resources equal to $9,000,000 from the public to itself. The holders of notes have again suffered a tax of 25 per cent in proportion to their holdings.

Like other forms of taxation, these exactions, if overdone and out of proportion to the wealth of the community, must diminish its prosperity and lower its standards, so that at the lower standard of life the aggregate value of the currency may fall and still be enough to go round. But this effect cannot interfere very much with the efficacy of taxing by inflation. Even if the aggregate real value of the currency falls for these reasons to a half or two-thirds of what it was before, which represents a tremendous lowering of the standards of life, this only means that the quantity of notes which the Government must issue in order to obtain a given result must be raised proportionately. It remains true that by this means the Government can still secure for itself a large share of the available surplus of the community.

45

Has the public in the last resort no remedy, no means of protecting itself against these ingenious depredations? It has only one remedy,—to change its habits in the use of money. The initial assumption on which our argument rested was that the community did not change its habits in the use of money.

Experience shows that the public generally is very slow to grasp the situation and embrace the remedy. Indeed, at first there may be a change of habit in the wrong direction, which actually facilitates the Government’s operations. The public is so much accustomed to thinking of money as the ultimate standard, that, when prices begin to rise, believing that the rise must be temporary, they tend to hoard their money and to postpone purchases, with the result that they hold in monetary form a larger aggregate of real value than before. And, similarly, when the fall in the real value of the money is reflected in the exchanges, foreigners, thinking that the fall is abnormal and temporary, purchase the money for the purpose of hoarding it.

But sooner or later the second phase sets in. The public discover that it is the holders of notes who suffer taxation and defray the expenses of government, and they begin to change their habits and to economise in their holding of notes. They can do this in various ways:—(1) instead of keeping some part of their ultimate reserves in money they can spend this money on durable objects, jewellery or46 household goods, and keep their reserves in this form instead; (2) they can reduce the amount of till-money and pocket-money that they keep and the average length of time for which they keep it,11 even at the cost of great personal inconvenience; and (3) they can employ foreign money in many transactions where it would have been more natural and convenient to use their own.

11 In Moscow the unwillingness to hold money except for the shortest possible time reached at one period a fantastic intensity. If a grocer sold a pound of cheese, he ran off with the roubles as fast as his legs could carry him to the Central Market to replenish his stocks by changing them into cheese again, lest they lost their value before he got there; thus justifying the prevision of economists in naming the phenomenon “velocity of circulation”! In Vienna, during the period of collapse, mushroom exchange banks sprang up at every street corner, where you could change your krone into Zurich francs within a few minutes of receiving them, and so avoid the risk of loss during the time it would take you to reach your usual bank. It became a seasonable witticism to allege that a prudent man at a café ordering a bock of beer should order a second bock at the same time, even at the expense of drinking it tepid, lest the price should rise meanwhile.

By these means they can get along and do their business with an amount of notes having an aggregate real value substantially less than before. For example, the notes in circulation become worth altogether $20,000,000 instead of $36,000,000, with the result that the next inflationary levy by the Government, falling on a smaller amount, must be at a greater rate in order to yield a given sum.

When the public take alarm faster than they can change their habits, and, in their efforts to avoid loss, run down the amount of real resources, which they hold in the form of money, below the working47 minimum, seeking to supply their daily needs for cash by borrowing, they get penalised, as in Germany in 1923, by prodigious rates of money-interest. The rates rise, as we have seen in the previous chapter, until the rate of interest on money equals or exceeds the anticipated rate of the depreciation of money. Indeed it is always likely, when money is rapidly depreciating, that there will be recurrent periods of scarcity of currency, because the public, in their anxiety not to hold too much money, will fail to provide themselves even with the minimum which they will require in practice.

Whilst economists have sometimes described these phenomena in terms of an increase in the velocity of circulation due to loss of confidence in the currency; nevertheless there are not, I think, many passages in economic literature where the matter is clearly analysed. Professor Cannan’s article on “The Application of the Apparatus of Supply and Demand to Units of Currency” (Economic Journal, December 1921) is one of the most noteworthy. He points out that the common assumption that “the elasticity of demand for money is unity” is equivalent to the assertion that a mere variation in the quantity of money does not affect the willingness and habits of the public as holders of purchasing power in that form. But in extreme cases this assumption does not hold; for if it did, there would be no limit to the sums which the Government could extract from48 the public by means of inflation. It is, therefore, unsafe to assume that the elasticity of demand is necessarily unity. Professor Lehfeldt followed this up in a subsequent issue of the Economic Journal (December 1922) by a calculation of the actual elasticity of demand for money in some recent instances. He found that between July 1920 and April 1922, the elasticity of demand for money fell to an average of about ·73 in Austria, ·67 in Poland, and ·5 in Germany. Thus in the last stages of inflation the prodigious increase in the velocity of circulation may have as much, or more, effect in raising prices and depreciating the exchanges than the increase in the volume of notes. The note-issuing authorities often cry out against what they regard as the unfair and anomalous fact of the notes falling in value more than in proportion to their increased volume. Yet it is nothing of the kind; it is merely the result of the one method to evade a crushing burden left open to the public, who discover for themselves, sooner than the financiers, that the law of unit elasticity in their demand for money can be escaped.

Nevertheless, it is evident that so long as the public use money at all, the Government can continue to raise resources by inflation. Moreover, the conveniences of using money in daily life are so great that the public are prepared, rather than forego them, to pay the inflationary tax, provided it is not raised to a prohibitive level. Like other conveniences of life the49 use of money is taxable, and, although for various reasons this particular form of taxation is highly inexpedient, a Government can get resources by a continuous practice of inflation, even when this is foreseen by the public generally, unless the sums they seek to raise in this way are very grossly excessive. Just as a toll can be levied on the use of roads or a turnover tax on business transactions, so also on the use of money. The higher the toll and the tax, the less traffic on the roads, and the less business transacted, so also the less money carried. But some traffic is so indispensable, some business so profitable, some money-payments so convenient, that only a very high levy will stop completely all traffic, all business, all payments. A Government has to remember, however, that even if a tax is not prohibitive it may be unprofitable, and that a medium, rather than an extreme, imposition will yield the greatest gain.

Suppose that the rate of inflation is such that the value of the money falls by half every year, and suppose that the cash used by the public for retail purchases in shops is turned over 100 times a year (i.e. stays in one pocket for half a week on the average); then this is only equivalent to a turnover tax of ½ per cent on each transaction. The public will gladly pay such a tax rather than suffer the trouble and inconvenience of barter with trams and tradesmen. Even if the value of the money falls by half50 every month, the public, by keeping their pocket-money so low that they turn it over once a day on the average instead of only twice a week, can still keep the tax down to the equivalent of less than 2 per cent on each transaction, or more precisely 4d. in the £. Even such a terrific rate of depreciation as this is not sufficient, therefore, to counterbalance the advantages of using money rather than barter in the trifling business of daily life. This is the explanation why, even in Germany and in Russia, the Government’s notes remained current for many retail transactions.

For certain other purposes, however, to which money is put in a modern community, the inflationary tax becomes prohibitive at a much earlier stage. As a store of value, for example, money is rapidly discarded, as soon as further depreciation is confidently anticipated. As a unit of account, for contracts and for balance sheets, it quickly becomes worse than useless, although for such purposes the privilege of the current money as legal-tender for the discharge of debts stands in the way of its being discarded as soon as it ought to be.

In the last phase, when the use of the legal-tender money has been discarded for all purposes except trifling out-of-pocket expenditure, inflationary taxation has at last defeated itself. For in that case the total value of the note issue, which is sufficient to meet the public’s minimum requirements, amounts to51 a figure relatively so trifling that the amount of resources which the government can hope to raise by yet further inflation—without pushing it to a point at which the money will be discarded even for out-of-pocket trifles—is correspondingly small. Thus at last, unless it is employed with some measure of moderation, this potent instrument of governmental exaction breaks in the hands of those that use it, and leaves them at the same time with the rest of their fiscal system in total ruins;—out of which, in the ebb and flow of the economic life of nations, may emerge once more a reformed and admirable system. The chervonetz of Moscow and the krone of Vienna are already stabler units than the franc or the lira.

All these matters can be illustrated from the recent experiences of Germany, Austria, and Russia. The following tables show the gold value of the note issues of these countries at various dates:

| Germany. | Volume of Note Issue in Milliard Paper Marks. | Number of Paper Marks = 1 Gold Mark. | Value of Note Issue in Milliard Gold Marks. |

| December 1920 | 81 | 17 | 4·8 |

| December 1921 | 122 | 46 | 2·7 |

| March 1922 | 140 | 65 | 2·2 |

| June 1922 | 180 | 90 | 2·0 |

| September 1922 | 331 | 349 | 0·9 |

| December 1922 | 1,293 | 1,778 | 0·7 |

| February 1923 | 2,266 | 11,200 | 0·2 |

| March 1923 | 4,956 | 4,950 | 1·0 |

| June 1923 | 17,000 | 45,000 | 0·4 |

| August 1923 | 116,000 | 1,000,000 | 0·116 |

52

| Austria. | Volume of Note Issue in Milliard Paper Krone. | Number of Paper Krone = 1 Gold Krone. | Value of Note Issue in Million Gold Krone. |

| June 1920 | 17 | 27 | 620 |

| December 1920 | 30 | 70 | 430 |

| December 1921 | 174 | 533 | 326 |

| March 1922 | 304 | 1,328 | 229 |

| June 1922 | 550 | 2,911 | 189 |

| September 1922 | 2,278 | 14,473 | 157 |

| December 1922 | 4,080 | 14,473 | 282 |

| March 1923 | 4,238 | 14,363 | 295 |

| August 1923 | 5,557 | 14,369 | 387 |

| Russia. | Volume of Note Issue in Milliard Paper Roubles. | Number of Paper RoublesB = 1 Gold Rouble. | Value of Note Issue in Million Gold Roubles. |

| January 1919 | 61 | 103 | 592 |