Very truly Yours Charles N. Fowler

SEVENTEEN TALKS

ON THE

BANKING QUESTION

BETWEEN

UNCLE SAM

AND

| MR. FARMER, | MR. BANKER, |

| MR. LAWYER, | MR. LABORINGMAN, |

| MR. MERCHANT, | MR. MANUFACTURER |

BY

Hon. Charles N. Fowler

WHO WAS A MEMBER OF THE HOUSE OF REPRESENTATIVES FOR SIXTEEN YEARS, A MEMBER OF THE BANKING AND CURRENCY COMMITTEE FOR FOURTEEN YEARS AND CHAIRMAN OF THE COMMITTEE FOR EIGHT YEARS

PUBLISHED BY THE

FINANCIAL REFORM PUBLISHING CO.

ELIZABETH, NEW JERSEY

Copyright, 1913, by

FINANCIAL REFORM PUBLISHING CO.

THE TROW PRESS

NEW YORK

FOREWORD

This book is written in the form of a conversation between Uncle Sam and six men of various occupations. It begins with the A, B, C of the subject and by question and answer goes over all the different phases of the subject precisely as you would expect them to arise under such circumstances. After weeks of study and investigation they finally reach an agreement, based upon their talks, and formulate a Financial and Banking system for the United States.

The Author.

TABLE OF CONTENTS

| PAGE | |

| FIRST NIGHT. The Standard of Value | 7 |

| SECOND NIGHT. What Is Money? | 26 |

| THIRD NIGHT. What Is Currency? | 46 |

| FOURTH NIGHT. Bank Credit Currency | 62 |

| FIFTH NIGHT. What Is Exchange? | 84 |

| SIXTH NIGHT. Value, Price, Wealth, Property, Credit | 101 |

| SEVENTH NIGHT. Commercial Credit, Land Credit, Government Credit | 118 |

| EIGHTH NIGHT. Colonial Credit Money | 144 |

| NINTH NIGHT. United States Notes or Greenbacks | 173 |

| TENTH NIGHT. Reserves | 195 |

| ELEVENTH NIGHT. The Bank | 224 |

| TWELFTH NIGHT. Land Credit Bank | 248 |

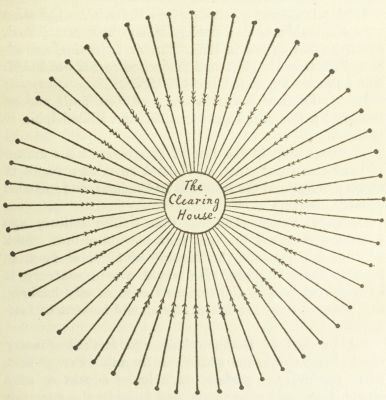

| THIRTEENTH NIGHT. The Clearing House | 289 |

| FOURTEENTH NIGHT. Banking in 1860 | 340 |

| FIFTEENTH NIGHT. Outline of Bill | 368 |

| SIXTEENTH NIGHT. Draft of Bill | 405 |

| SEVENTEENTH NIGHT. Aldrich Plan and Plot Exposed | 459 |

THE STANDARD OF VALUE

Uncle Sam: Gentlemen, I have invited you to take part in one conversation a week upon the much-vexed and all-important question of a financial and banking system for my country. We shall continue these conversations until we arrive at some conclusion which will be satisfactory to all of us, although this may seem difficult at the outset.

To begin with, I want to assure you that our talks shall be absolutely confidential, and nothing that is said at these meetings shall ever go any farther, unless we agree to announce our conclusion. With this understanding we can be brutally frank with each other, and I can expose my hand to you.

The present situation is one demanding immediate attention, and only our ignorance, greed or political cowardice can prevent us from arriving at a satisfactory solution of this problem. We must be sincere and patriotic in our purpose, for we represent practically every phase of our citizenship, and I assume you are typical of the average intelligence of the people.

Here is Mr. Lawyer to steer us clear of legal obstacles, Mr. Laboringman to speak for our millions of daily toilers, Mr. Farmer to point out the disadvantage of agricultural loans, Mr. Merchant to illustrate the defects of our present commercial credits, Mr. Manufacturer to caution us against the conversion of our liquid capital into fixed investments and Mr. Banker to tell us of his woes and enlighten us upon the remedies for all his ills.

What we don't know now, we will each attempt to find out before our talks come to an end. Certainly there is some solution to this question. In short and in fact it must be solved.

I am the laughing stock of the entire civilized world today. For our persistent folly we suffer losses in the aggregate amounting to hundreds of millions of dollars every year. We ought to have, and can have the best and the most efficient banking system in the world. Indeed, we ought to give the laugh to all the other countries in banking, as we do practically in everything else. It is up to us.

Mr. Banker: Uncle Sam, I agree absolutely with what you have just said. I believe it is our duty to sit every week, as you suggest, continuously until we arrive at some conclusion upon which we can all agree. If we do this I believe, since we represent so many callings and are so representative of the various lines of business, we shall find the public approving of our conclusion.

I suggest that we begin with the very A, B, C of this question, and settle one point after another as we go along. If we do this, our differences will disappear as we progress, and the X, Y, Z of this question, or the formation of a financial and banking system, will be comparatively easy in the end.

For example, we must first fix clearly in our minds what a standard of value is, and what our standard of value is, what money is, what currency is, what capital is, what a bank is, and so continue step by step to the end, leaving absolutely nothing for guesswork, if that is at all possible.

The experience of the world has been so broad and complete that our solution of this question is entirely possible, although we have some problems that are peculiar to ourselves.

Mr. Lawyer: That plan suits me exactly, for only recently I made a thorough study of the question of our standard of value. My investigation took me back more than 6,000 years, and I found the subject amusing often as well as intensely interesting, while the result of my research was most satisfactory.

I discovered that everything from baked clay to the[Pg 9] credit of practically every government that has ever existed had been used at some time or other, as a standard of value, or a measure of value.

Mr. Farmer: Mr. Lawyer, just what do you mean by a "standard of value"?

Mr. Lawyer: A "standard of value" is anything that may be selected by which all other things in some particular locality or country are measured.

The Indians of British Columbia used haiquai shells; one string being equal to one beaver skin. In Australia tough green stone and red ochre were used. In Central Africa slaves were used. In Iceland the law made cattle the standard of value. In the Fiji Islands whales' teeth. In the South Sea Islands red feathers were used. In Mexico and Abyssinia salt was used.

Agriculture has produced its standard of value; corn, maize, olive oil, cocoanuts, cocoa-nut oil, tea, tobacco, cacao, beans, wheat, rice.

The pastoral life produced its standard of value; sheep, cattle, goats, horses and practically every other domestic animal, according to the time and place.

The following history of American experience in the development of a standard of value cannot be better restated, and is practically a repetition of the experience of mankind in all the ages, therefore I want to read what Horace White says upon the subject:

"It may be said that Virginia grew her own money for nearly two centuries, and Maryland for a century and a half.

"The first settlers of New England found wampumpeage, sometimes called wampum and sometimes peage, in use among the aborigines as an article of adornment and a medium of exchange. It consisted of beads made from the inner whorls of certain shells found in sea water. The beads were polished and strung together in belts or sashes.

"They were two colors, black and white, the black being double the value of the white. The early settlers of[Pg 10] New England, finding that the fur trade with the Indians could be carried on with wampum, easily fell into the habit of using it as money. It was practically redeemable in beaver skins, which were in constant demand in Europe. The unit of wampum money was the fathom, consisting of 360 white beads worth sixty pence the fathom. In 1648 Connecticut decreed that wampum should be 'strung suitably and not small and great uncomely and disorderly mixt as formerly it hath been.' Four white beads passed as the equivalent of a penny in Connecticut, although six were usually required in Massachusetts and sometimes eight. In the latter colony wampum was at first made legally receivable for debts to the amount of 12d. only. In 1641 the limit was raised to fifty pounds sterling, but only for two years. It was then reduced to forty shillings. It was not receivable for taxes in Massachusetts. The use of wampum money extended southward as far as Virginia.

"The decline of the beaver trade brought wampum money into disrepute. When it ceased to be exchangeable in large sums for an article of international trade the basis of its value was gone. Moreover it was extensively counterfeited, and the white beads were turned into the more valuable black ones by dyeing. Nevertheless it lingered in the currency of the colonies as small change till the early years of the eighteenth century. While it was in use it fluctuated greatly in value.

"The first General Assembly of Virginia met at Jamestown July 31, 1619, and the first law passed was one fixing the price of tobacco 'at three shillings the beste, and the second sorte at 18d. the pounde.' Tobacco was already the local currency. In 1642 an act was passed forbidding the making of contracts payable in money, thus virtually making tobacco the sole currency.

"The Act of 1642 was repealed in 1656, but nearly all the trading in the Province continued to be done with tobacco as the medium of exchange.

"In 1628 the price of tobacco in silver had been 3s. 6d.[Pg 11] per pound in Virginia. The cultivation increased so rapidly that in 1631 the price had fallen to 6d. In order to raise the price, steps were taken to restrict the amount grown and to improve the quality. The right to cultivate tobacco was restricted to 1,500 polls. Carpenters and other mechanics were not allowed to plant tobacco 'or do any other work in the ground.' These measures were ineffective. The price continued to fall. In 1639 it was only 3d. It was now enacted that half of the good and all of the bad should be destroyed, and that thereafter all creditors should accept 40 lbs. for 100; that the crop of 1640 should not be sold for less than 12d., nor that in 1641 for less than 2s. per lb., under penalty of forfeiture of the whole crop. This law was ineffectual, as the previous ones had been, but it caused much injustice between debtors and creditors by impairing the obligation of existing contracts. In 1645 tobacco was worth only 1-1/2d. and in 1665 only 1d. per lb.

"These events teach us that a commodity which is liable to great and sudden changes of supply is not a desirable one to be used as money.

"In the year 1666 a treaty was negotiated between the colonies of Maryland, Virginia, and Carolina, to stop planting tobacco for one year in order to raise the price. This temporary suspension of planting made necessary some other mode of paying debts. It was accordingly enacted that both public dues and private debts falling due 'in the vacant year from planting' might be paid in country produce at specified rates.

"In 1683 an extraordinary series of occurrences grew out of the low price of tobacco. Many people signed petitions for a cessation of planting for one year for the purpose of increasing the price. As the request was not granted, they banded themselves together and went through the country destroying tobacco plants wherever found. The evil reached such proportions that in April, 1684, the Assembly passed a law declaring that these malefactors had passed beyond the bounds of right, and[Pg 12] that their aim was the subversion of the Government. It was enacted that if any persons, to the number of eight or more, should go about destroying tobacco plants, they should be adjudged traitors and suffer death.

"In 1727 tobacco notes were legalized. These were in the nature of certificates of deposit in Government warehouses issued by official inspectors. They were declared by law current and payable for all tobacco debts within the warehouse district where they were issued. They supply an early example of the distinction between money on the one hand, and Government notes, or Bank notes, on the other. The tobacco in the warehouses was a real medium of exchange. The tobacco notes were always payable to bearer for the delivery of this money. They were redeemable in tobacco of a particular grade, but not in any specified lots. Counterfeiting the notes was made a felony. In 1734 another variety of currency, called 'crop notes,' was introduced. These were issued for particular casks of tobacco, each cask being branded and the marks specified on the notes.

"The circulating medium of the New England colonies was quite as fantastic as that of Virginia. Merchantable beaver was legally receivable for debts at 10s. per pound. In 1631 the General Court of Massachusetts ordered that corn should pass for payment of all debts at the price it was usually sold for, unless money or beaver skins were expressly stipulated. In other words, a debt payable in pounds, shillings, and pence might be paid at the debtor's option in any one of three ways; in corn at the market price, in beaver at 10s. per pound, or in the metallic money of England. For more than half a century this order continued in force and operation, other things being added to the list from time to time.

"In 1635 musket balls were made receivable to the extent of 12d. in one payment.

"In 1640 Indian corn was made current at 4s. per bushel, wheat at 6s., rye and barley at 5s., and peas at 6s.[Pg 13] Dried fish was added to the list. Taxes might be paid in these articles and also in cattle, the latter to be appraised.

"The need of metallic currency was severely felt. In 1654 it was ordered that no coin should be exported, except 20s. to pay each one's traveling expenses, on penalty of forfeiture of the offender's whole estate.

"The cost of carrying the country produce taken for taxes amounted to 10 per cent of the collections. A constable once collected 130 bushels of peas as taxes in Springfield. He found that he could transport this portion of the public revenue most cheaply by boat. Launching it on the Connecticut River, he shipped so much water on board at the falls that the peas were spoiled. Thus we learn that money ought to be easy of carriage and not liable to injury by exposure to the elements.

"In 1670 it was ordered for the first time that contracts made in silver should be paid in silver.

"In 1675, during King Philip's war, the need of metallic money for public use was so great that a deduction of 50 per cent was offered on all taxes so paid.

"The first local currency of New Netherlands was wampum, but it was subordinate to the silver coinage of the mother country; that is, it was reckoned in terms of that coinage as fixed by the Dutch West India Company from time to time. It was fixed at six white beads for a stiver. Wampum was not made in the province, but was imported from the east end of Long Island, the principal seat of production. It is mentioned in a letter from the Patroons of New Netherlands to the States General in June, 1634, as 'being in a manner the currency of the country with which the produce of the country is paid for,' the produce of the country being furs.

"Beaver soon became current here, as in New England, and for the same reason, its currency value being fixed by the company at 8 florins per skin. As 5 wampum beads were equal to 1 stiver and 20 stivers to 1 florin, and 8 florins to 1 skin, the ratio of wampum to beaver was 960 to 1. The market ratio did not coincide with the[Pg 14] legal ratio very long. Nor was the legal ratio of either wampum or beaver to silver maintained; for, in 1656, Director Stuyvesant wrote to the company urging that beaver be rated at 6 florins instead of 8, and wampum at 8 for a stiver instead of 6, as these rates were nearer the commercial values.

"In 1719 the Assembly of South Carolina made rice receivable for taxes, 'to be delivered in good barrels upon the bay in Charlestown.' In the following year a tax of 1,200,000 pounds of rice was levied, and commissioners were appointed to issue rice orders to public creditors, in anticipation of collection, at the rate of 30s. per 100 lb., in the following form:

"'This order entitles the bearer to one hundred weight of well-cleaned merchantable rice to be paid to the commissioners that receive the tax on the second Tuesday in March, 1723.'

"Rice orders were made receivable for all purposes, and counterfeiting was made felony without benefit of clergy.

"In eastern Tennessee and Kentucky, early in the nineteenth century, deer skins and raccoon skins were receivable for taxes and served the purposes of currency.

"When California was first invaded by gold seekers there were a few Mexican coins in circulation there, not nearly sufficient to answer the needs of the growing community. The immigrants brought more or less metallic money with them. The smaller coins were those of many different countries, chiefly Spanish. For want of sufficient coins, the first trading was done largely with gold dust, sometimes by weighing it in scales, sometimes by guesswork. A 'pinch' of gold dust about as large as a pinch of snuff had a current value and was a common measure in places where there was no means of weighing. At a public meeting in San Francisco, September 9, 1848, it was resolved by unanimous vote that $16 per ounce was a fair price for placer gold. This rate was at once adopted in all business transactions. By and by private[Pg 15] coiners of gold came into the field. The Legislature was at first alarmed by the appearance of these unaccustomed pieces, and passed a law to prohibit circulation and to close the shops where they were made. It was soon found, however, that they were a great convenience. Then the law was repealed. Several establishments immediately went to work assaying and coining gold. One of these was at Salt Lake City, whose productions were known as Mormon coins. Only one of these establishments, that of Moffat & Co., of San Francisco, conformed exactly to the government standard of weight and fineness. All the others, however, including the Mormon ones, circulated freely, and were received on deposit by the banking houses until the government set up an assay office and began to stamp octagonal pieces of $50, called 'slugs,' and afterwards those of $20 each. This was done in 1851; the San Francisco mint was not ready till 1854. The Moffat coins continued to circulate after the mint had gone into operation, since everybody had confidence in their goodness. It is estimated that $50,000,000 of private coins were struck. They were received in the Atlantic cities at their assay value only."

The foregoing illustrations drawn from our own history serve to explain the nature of money and the processes by which mankind learns to distinguish between good money and bad.

Mr. Farmer: In all that has been said there is nothing stranger nor more interesting than what is going on today.

Uap is one of the most interesting of the South Sea Islands. It is the Western outpost of the Carolines, which were purchased by Germany from Spain for $3,300,000 at the close of the Spanish-American War. The form of money used by the people and the perfection of the system of currency is as interesting as anything in the history of the human race.

The small change consists of pieces of pearl shell and small round stones. Large sums are represented by fei.[Pg 16] These are big circular stones in the form of wheels ranging in diameter from one to twelve feet. In the centre of each is a hole through which a pole is thrust to facilitate carriage from one spot to another.

These coins are not minted on the island, nor has any addition been made to the supply of them for a number of years. They were originally fashioned in the Pelao Islands, and brought thence to Uap in canoes over a stretch of four hundred miles of ocean. A very large fei could not be changed into smaller coin without seriously disturbing the currency of the island. The owner of one of these twelve-foot masses of wealth is a sort of J.P. Morgan. Like the man with the million dollar bill in Mark Twain's story, he does not need to break his money in order to pay for anything he may buy, but readily secures all that he desires on credit.

It speaks volumes for the honesty of the islanders that all this stone money is left out of doors standing against the sides of the huts. The annals of Uap do not contain a single record of the theft of a fei, but perhaps the difficulty of disposing of such unwieldy cash may be a potent factor in the matter. Not only is the ownership of a large fei equivalent to the command of an unlimited amount of currency, but abstract possession seems to entail the same advantage.

Many years ago a canoe carrying one of these large stones was sunk a few miles off the island. Although the fei went to the bottom of the ocean and has lain there ever since, the man to whom it was consigned enjoyed all the advantages that would have accrued from its delivery to him. During his lifetime he was accredited one of the wealthiest men of Uap. Not only that, but he bequeathed his interest in the submerged fei to his son, and it has been passed on in like manner through four or five generations, securing all the advantages of substantial wealth to each.

Mr. Lawyer: Metal of some kind has been used as far back as the records of time go, and strange as it may[Pg 17] seem, gold was the first metal to be used as well as the first to be discovered, as a standard of value, or measure of value. Iron was used in Sparta, spikes in Central Africa, nails in Scotland, lead in Burmah, copper, tin and silver in Rome. Silver and gold were used in China a thousand years ago. In her palmy days gold bracelets and rings were weighed out in Egypt, measuring value.

For the past two hundred years there has been a distinct evolution of the world's present standard of value going on, sometimes it has been gold, sometimes it has been silver, sometimes nations have tried to have both. During the last hundred years the struggle to use both has gone on persistently until within the last twenty-five or thirty years.

William A. Shaw states that in France during a period of one hundred years, the ratio between gold and silver had been changed one hundred and fifty times. The controversy of this period has well been called the "Battle of the Standards."

A constantly increasing trade between the nations of the earth has made a common standard of value more and more important, while the ever-increasing refinement in the exchange of commodities among the peoples of the earth has made a single standard absolutely essential.

Experience has wrought the change, and now the entire commercial world has gold as its standard of value.

It is interesting to observe how gold because of its peculiar fitness, as compared with any other commodity, was finally selected and adopted as the world's standard of value.

If we were to study for months for the purpose of ascertaining what the characteristics of the world's standard of value should be, we would define the characteristics of gold as particularly distinguished from any other metal or thing.

First: Gold has by far a greater stability of value than any other substance. It is very doubtful whether there[Pg 18] is a perceptible change, at least any such change of value, as could be agreed upon. It is so small.

Second: Gold has portability, or the facility of transportation from one part of the country to the other, or from one nation to the other, that makes it desirable as compared with any other metal, that is to be thought of for a standard of value. For example, the same value in silver weighs thirty times as much.

Third: The divisibility of gold at the mint into convenient pieces for trade and commerce is all that can be desired.

Fourth: It has, practically speaking, perfect durability. It will not corrode, or waste away, except by wear, and waste by wear is now largely obviated by the use of some representative, such as our gold certificate.

Fifth: Gold possesses homogeneity or perfect uniformity of structure and material.

Sixth: Gold possesses cognizability, or can be readily known or recognized.

It was undoubtedly all these inherent qualities, these prerequisites that led to those legislative enactments which have during the last hundred years singled out this yellow metal as the most fit arbiter of the world's trade.

The first legislative act that seemed to lead to this ultimate decision of the world was passed by the House of Commons in 1774, but not until 1816 was the law passed that definitely settled the question of the standard of value for Great Britain. The very same law passed in that year, now nearly one hundred years ago, remains in force to this day.

In 1853, the United States followed Great Britain in an attempt to establish the gold standard. We reduced the weight of our silver coins, smaller than one dollar, and made them legal tender for only five dollars in amount. The silver dollar was not considered in this legislation of 1853, and not until February 12, 1873, did the gold dollar become the unit of value, when the gold standard was unequivocally established. The silver dol[Pg 19]lar was at that time worth about two cents more than a gold dollar, and therefore it was omitted from the coinage. This was the famous crime of '73, about which the men now wearing gray hair, or no hair, heard so much in the '80's and early '90's. Yes, we were hearing this as late as 1896, when it was the Battle Cry of the Presidential Campaign.

It may be stated that practically the whole civilized world, with the single exception of Great Britain, has come to the single gold standard, since 1873.

The only country now remaining upon the silver basis, or that has not taken steps to place itself upon a gold basis, is, according to the report of the Director of the Mint, the Central American States, which are of comparatively no commercial importance whatever.

Mr. Merchant: How much gold is there in the world today?

Mr. Lawyer: It was estimated in 1890 that the amount of gold accumulated was approximately $4,000,000,000 (four thousand million dollars).

The amount of gold produced during the last twenty-two years, or since 1890, by all the countries of the world approximates $6,500,000,000 (six thousand five hundred million dollars). Of course a deduction, or allowance, must be made for what has been used outside of monetary purposes, or in industrial consumption, approximately $1,500,000,000 (one thousand five hundred million dollars). A deduction should also be made for what has been absorbed by India, about $700,000,000 (seven hundred million dollars), and also by Egypt, about $200,000,000 (two hundred million dollars), or nearly $1,000,000,000 (one thousand million dollars), by these two countries.

The Director of the Mint in his report, Page 53, says:

"In statistics of the precious metals India is the most important country of Asia, and has long been one of the most important in the world. The Government of India has advised this bureau that the uncoined gold imported[Pg 20] into that country might be considered to be used for ornaments and in manufactures. This amounted in 1910 to $47,026,698.

"The movement to India deserves to be treated in a class by itself. A large part of the gold and silver that goes there sinks out of sight, and whether it is made into ornaments or buried in the ground, is withdrawn at least in large part from the monetary stock of the world. Some of it may be brought out in periods of emergency, such as times of famine, and reconverted into money, but in the past a steady stream of the precious metals has moved into India and disappeared as a factor in the commercial world. Sir James Wilson, K.C.S.I., for many years in the Government service in India, in a comprehensive address delivered before the East India Association of London, on June 14, 1911, reported the net imports of gold by India since 1840 at about $1,200,000,000, or one-tenth of the world's production in that time.

"It may be questioned whether the economists who are expressing fears as to the effects that may result from the production of gold at the present rate are aware of the amount of that metal taken by India since the gold standard was definitely established, and the Government began to pay out sovereigns freely. That occurred in 1900. For the ten-year period, 1890-1899, the net imports plus the country's own production were $135,800,000; for the eleven years, 1900-1910, they aggregated $433,800,000. For the British fiscal years ended March 31, 1911, they amounted to $90,487,000, or about one-quarter of the world's production after the industrial consumption was provided for.

"If this ability on the part of India to take and pay for gold proves to be permanent, it is apparent that there will be no over supply to trouble the rest of the world."

The finance department of the Government of India, in its report for the fiscal year ended March 31, 1911, commenting upon these figures, says:

"'The gold figures are striking, but it is equally re[Pg 21]markable that the increase in gold has not been at the expense of silver; the country, in other words, continues to take practically the same amount of silver, but it prefers that the addition to the imports of treasure which it has been able to claim should be in the form of gold.'"

Sir James Wilson, in the address alluded to, sums up his explanation by saying:

"'As for India, her prosperity is steadily advancing. Great numbers of her people prefer to spend their savings on gold rather than on other commodities. The probability is that altogether apart from questions of currency India will continue to absorb gold in ever increasing quantities.'

"The Egyptian situation is somewhat like that of India. The country is on a gold basis, and for thirty years has been steadily taking gold in the settlement of its trade balances. The high price of cotton in recent years, and the increasing production of the country explains the trade balances, but there is some mystery about the way the gold disappears from view. It does not enter into bank stocks, and it is difficult to understand how a country of its size and population, and in which the masses of the people are so poor, can absorb so much gold coin. In the first period under review the customs records show net imports by $58,670,000, and in the second period, $146,660,000. For the year 1910 they were $30,000,000.

"Some light is shed upon the situation by the following statement in an address by Lord Cromer, made in London, in 1907:

"'A little while ago I heard of an Egyptian gentleman who died leaving a fortune of £80,000 [$400,000], the whole of which was in gold coin in his cellars. Then, again, I heard of a substantial yeoman who bought property for £25,000 ($125,000). Half an hour after the contract was signed he appeared with a train of donkeys bearing on their backs the money, which had been buried in his garden. I hear that on the occasion of a fire in a provincial town no less than £5,000 ($25,000) was found[Pg 22] hidden in earthen pots. I could multiply instances of this sort. There can be no doubt that the practice of hoarding is carried on to an excessive degree.'"

In round figures the approximate amount of gold remaining for commercial or banking purposes is approximately $4,000,000,000 (four thousand million dollars), in addition to what we had in 1890, making a total of $8,000,000,000 (eight thousand million dollars).

Of this total amount the United States has $1,800,000,000 (one thousand eight hundred million dollars), or nearly one-quarter of the monetary gold supply of the world.

However, if we had our proper proportion of the world's monetary gold, considered from the standpoint of our bank resources, we should have upwards of $3,000,000,000 (three thousand million dollars).

Mr. Banker: How do you make that out?

Mr. Lawyer: The banking resources of the entire world are now about $55,000,000,000, while those of the United States are about $25,000,000,000, or two-fifths of the bank resources of the world, and therefore we are entitled to two-fifths of the eight billion of monetary gold of the world. This would give us $3,200,000,000.

While, as I have just said, it is true that there have been no discoveries of new fields since 1890, with the exception of the Klondike, a most important event occurred in the discovery of the Cyanide process, which was, with the circumstances attending it, well described by the Mining World and Engineering Record of London, which said:

"The discovery of the Cyanide process must be regarded as one of the greatest achievements of modern time. And there can be no doubt that Cyaniding will be held by the coming generation for its importance, not so much to the mineral industries directly, as for its bearing upon world economies in rendering possibly a greatly increased output of gold and silver year after year. In a comparatively brief twenty-year interval since[Pg 23] 1890, when Messrs. McArthur and Forrest brought the modern perfected Cyanide process prominently before the mining world, the output of gold has amounted to 284,081,289 fine ounces. This is a most astonishing showing, especially when compared with a total output of 401,311,148 fine ounces for the entire 397 years previous from 1493 to 1890, a period lacking just three years of being four centuries.

"For the great expansion in the world's output, particularly noticeable in the past fifteen years, the spread of the Cyanide process is directly responsible. Nor, if we except the Klondike, has this record production been boomed by the development of new fields. The cream of the world's gold fields had already been skimmed in previous years in California, Australia, South Africa, Siberia, India, and elsewhere. It is mainly on the cast-off leavings of the old field that the Cyanide process has achieved a record production of the yellow metal. And among those leavings, we must not forget the innumerable low-grade properties whose exploitation has been rendered fundamentally possible only by the Cyanide process. It is these latter which now furnish the bulk of the world's supply of gold, and upon which the world must depend very largely for its future requirements."

Mr. Banker: Those figures are startling. We must be getting more gold than we need for banking purposes.

Mr. Lawyer: On the contrary, our banking resources are increasing faster than our gold supply. In 1890 the banking resources of the world were estimated at $16,000,000,000, less than one-third of what they are today. That is, the banking resources have trebled since 1890, and the gold supply for reserve or monetary purposes has only doubled.

Mr. Banker: What about the gold supply for the future?

Mr. Lawyer: The production during the past four years has been about stationary, averaging $450,000,000 each year. You must remember there have been no gold[Pg 24] discoveries of any consequence during the past ten years, and it is very probable that the production will remain almost stationary for a few years to come. At present it looks as though the gold supply, and the demand for gold for monetary purposes, would run along about equal. Of course the more intimate the business relations of the nations of the earth become, the more efficient will the reserve of gold become, because the reserves of the world will become more and more mobilized, and therefore more efficient in the conduct of the world's business.

Mr. Merchant: From what you have said, and as a result of my own study, I am convinced that the adoption of the Gold Standard was a natural selection. It was the survival of the fittest.

Thousands of books have been written upon this subject, and libraries literally filled with them.

In 1896, when the Presidential campaign was fought out on this question, my investigation led me into an extended historical review of the use of metals as money. I found that it had been in use by the Babylonians, the Egyptians, the Greeks, the Romans, the Chinese, the Europeans during the middle ages, and that the struggle between gold and silver during the last two hundred years had resulted to the advantage of the people, to the commerce of every nation and to the whole world. This last struggle was not whether gold or silver should be the standard of value, but whether both should or could be used as the standard of value. That is, could we have a double standard. The decision has been unequivocal and universally in favor of a single standard of value, and that standard gold.

But the double or bi-metallic standard had been a troublesome question long before that. Professor Ridgeway says that from the first to the last the Greek communities were engaged in an endless quest after bi-metallism * * *, but while the gold unit never varies in any part of Hellas, until a late epoch, the silver coins exhibit differences not merely between one district and[Pg 25] another, but even between one period and another in the same city or state. There is incontrovertible evidence to prove that the same trouble was caused by the fluctuation in the relative value of gold and silver, as arises in modern times. DelMar also states that gold Greek coins remained constant while the silver ones varied, and had to be adjusted.

At present, it may be stated as a general truth, that all other things throughout the commercial world are now measured by gold, or very soon will be, as all the commercial nations of the earth, with a single exception, have taken steps looking to the adoption of the Gold Standard.

The Gold Standard is the evolution of the ages.

WHAT IS MONEY?

Uncle Sam: At our talk last Wednesday evening we all agreed upon two facts, and these were fundamental to the consideration of a financial and banking system for me.

The first fact was this: that Gold is the Standard of Value all the world over, as well as our standard.

The second fact: that a Standard of Value was something by which the value of all other things is measured.

It must necessarily follow then, and be perfectly clear to all of us that everything we produce, and everything that we buy and sell is measured by Gold. In other words that Gold is our money and that our money is Gold.

Mr. Lawyer: Uncle Sam, you say "Gold is our Money." Now, it seems to me as though there must be something done to gold to make it money, even though all our money is gold.

Mr. Banker: Yes, something is done to gold to make it money, and to circulate it as money. Just three things are done to gold to make it possible to circulate it as money.

First, we have established a degree of fineness. The gold coin we circulate as money is nine-tenths pure gold, or nine-tenths fine, and one-tenth of cheaper metal. This is added to give it an increased hardness so that the loss by rubbing the gold against other things will not be so great. This loss is called the abrasion of gold.

Second, we have established a unit of value in gold which is one dollar, composed of twenty-five and eight-tenths grains of gold, nine-tenths pure, or fine.

Third, Uncle Sam here cuts up the gold into pieces as follows: he makes a two dollar and a half piece, which contains two and a half times as much gold as our unit[Pg 27] of value and stamps each piece two and a half dollars. It is known as a quarter eagle, being one-quarter of the ten dollar piece which is called the eagle. He makes a five dollar piece which contains five times as much gold as our unit of value and stamps each piece five dollars. It is also known as a half eagle. He makes a piece which contains ten times as much gold as our unit of value and he stamps it ten dollars. It is also known as the eagle. He makes a piece which contains twenty times as much gold as our unit of value and stamps it twenty dollars. It is also known as the double eagle. This is called making coins, or coining money.

These four gold coins constitute all the money there is in the United States, for Uncle Sam does not make pieces containing twenty-five and eight-tenths grains of gold, nine-tenths pure, or fine any more, and stamp them one dollar because this piece of gold was so small as to be inconvenient, indeed an actual nuisance. Uncle Sam stopped making these coins in 1890.

Uncle Sam: That is right, and I don't make any more gold pieces now containing fifty times as much gold as my unit of value for the same reason that I don't make any of the dollar pieces. A fifty dollar piece was found to be inconvenient and in a way an actual nuisance.

Mr. Laboringman: Well, Uncle Sam, I would like to have a few of such nuisances, and if any of you fellows have any of these two nuisances, even the one dollar pieces about your persons, I wish you would allow me to relieve you of all you have of either kind. When it comes to getting rid of that kind of a nuisance, you don't seem to be in a hurry about it. However, just remember that I stand ready at all times to remove a nuisance of that kind, if it happens to be bothering any of you.

Mr. Merchant: We will remember that and give you the first chance.

Mr. Laboringman: Well, you might as well forget it, for I'll never get the chance.

Mr. Manufacturer: Mr. Banker, did I understand you[Pg 28] to say that the four gold coins you have mentioned, the two and a half, the five dollar, ten dollar and twenty dollar gold pieces constitute all the money that there is in the United States?

Mr. Banker: That is precisely what I said, and I stand ready to prove it. Yes, to demonstrate it absolutely, and if I don't convince everyone of you that I am right, I'll eat all the other stuff you call money that you can bring me.

Mr. Lawyer: Here is a gold certificate, isn't that money?

Mr. Banker: Mr. Lawyer, please hand me that certificate. Here is what it says on its face: "This certifies that there have been deposited in the Treasury of the United States of America Ten Dollars in Gold Coin payable to the bearer on demand." It is perfectly evident, Mr. Lawyer, that this is nothing but a warehouse receipt for ten dollars, stored in Washington subject to the demand of the holder. There is just the same difference between that and the gold coin as there is between a trunk and a trunk check. You would not hold up a trunk check, and tell me that it was a trunk. This certificate is no more money than a trunk check is a trunk.

Mr. Lawyer: You are right, Mr. Banker. There is nothing so absolutely essential in our talk, as illustrated by this incident, as the use of correct, exact language. And I am very glad that you have impressed this fact so indelibly upon our minds at the outset.

Mr. Farmer: Did you say, Mr. Banker, that all the money there was in the United States were the gold coins? Then you said that if you didn't convince the rest of us that that was the fact, you would eat all the other stuff that we call money that we would bring you. Now, it seems to me as though that was just one of your smooth, slick tricks of getting what we have got in our pockets, as usual. How does that strike the rest of you boys? Now, I have a few silver slugs here, Mr. Banker, that will[Pg 29] keep you busy chewing until you pass over, if you try that game on us.

Mr. Banker: That is all right, Mr. Farmer, but you wait until you hear me out.

Now, let us agree upon one fact, and that is this, that Uncle Sam over there is not making or coining any other pieces of gold than the four pieces I have just described, and that none of the one dollar or fifty dollar pieces are now in circulation. Do you all agree that that is a fair assumption under the circumstances?

Uncle Sam: Yes, that is a perfectly fair assumption that all of the gold now in circulation consists of the four pieces I am now making, the two and a half, five, ten and twenty dollar pieces. But, if they constitute all the money I have in circulation, I am mightily fooled, and it is high time I was put right.

Mr. Banker: Well, that is what I am going to do. I am going to put you right, for you have not only been fooled yourself, but you've been fooling the people long enough as well.

Three hundred and fifty years B.C., one of the greatest philosophers, and one of the wisest men that ever lived, described the development and evolution of money, and defined what money was better than any man ever has since, I think. That man was Aristotle. Aristotle's account of the origin and definition of money was as follows:

"It is plain that in the first Society (that is in the household) there was no such thing as barter, but that it took place when the community became enlarged: for the former had all things in common, while the latter, being separated, must exchange with each other according to their needs, just as many barbarous tribes now subsist by barter; for these merely exchange one useful thing for another, as, for example, giving and receiving wine for grain and other things in like manner. This kind of trading is not contrary to nature, nor does it resemble a gainful occupation, being merely the complement of[Pg 30] one's natural independence. From this, nevertheless, it came about logically that as the machinery for bringing in what was wanted, and of sending out a surplus was inconvenient, the use of money was devised as a matter of necessity. For not all the necessaries of life are easy of carriage; wherefore, to effect their exchanges, men contrived something to give and take among themselves, which being valuable in itself, had the advantage of being easily passed from hand to hand for the needs of life—such as iron, or silver, or something else of that kind, of which they first determined merely the size and weight, but eventually put a stamp on it in order to save the trouble of weighing, for the stamp was placed there as the sign of its value."

Wilbur Aldrich says: "Gold, and no other thing, sustains all the functions of money. Gold is money as soon as it is taken from the earth, without smelting, without refining, without minting and without limitation."

Horace White says: "Nobody would give that which has cost him labor in exchange for something which he could obtain without labor."

Mr. Merchant: Mr. Banker, you quoted a man there, Mr. Aldrich, I think it was, who said that gold alone possessed all the functions of money. Just what do you mean by the "functions of money"?

Mr. Banker: I am glad that you asked that very question, because those functions have determined the place of gold in the world's business, and made it the standard of value of the world, and consequently the money of the world.

Those functions are these:

First: Gold is a measure of value; that is, all other things are measured in gold.

Second: Gold is divided into units, such as our dollar, the English sovereign, the French franc, the German mark, and so determines prices.

Third: Gold is a medium of exchange.

Fourth: Gold is a storehouse of value; that is, the peo[Pg 31]ple of the world hold it as an absolutely safe form of property, varying less in value than anything else they can possess.

Fifth: It is such a permanent form of value that it is made the basis or standard of future or deferred payments: not only at the end of a year, but at the end of twenty-five or fifty years.

Mr. Merchant: I would like to ask you whether you think there is anything in this claim that gold is cheaper today than twenty years ago? Whether it is falling in value, and as a consequence prices of everything else, which must be compared with gold, are rising?

Mr. Banker: No, sir, I do not think that the increased output of gold is the cause of higher prices. The increased prices can be more than accounted for in other ways. Think of it. There are:

1. The Trusts,

2. The Middleman,

3. Advertising,

4. Unscientific Management,

5. Overcapitalization,

6. Monopoly! Monopoly!

7. Extravagance,

8. Militarism,

9. Exhaustion of Soil,

10. High Rates of Interest on Agricultural Loans,

11. Unnecessary Disease,

12. Concentration of Population in Cities,

13. Shorter Hours by one-quarter,

14. Increased Wages by one-quarter at least; in some instances, 150%,

15. Shorter Hours for Women,

16. Child Labor Laws,

17. Minimum Wage Laws,

18. Workmen's Compensation Acts,

19. Insurance Against Unemployment,

20. Old Age Pensions.

Mr. Laboringman: Well, I don't know what you fellows think, but I am for everyone of these forward movements that make for a better humanity, morally, intellectually and physically; and I'm utterly opposed to the unfair advantages that any man, or corporation, has over any other man, or any other corporation. A just government rules its people through just laws, and guarantees equal opportunities under the operation of those laws.

Mr. Banker: So I think we all are, or will be, very soon. Every lover of his country, everyone who recognizes that the government exists for man—manhood and womanhood—must be for these purposes, but all these things will require a readjustment, and will take time. I am only saying that these things more than account for all your high prices, but let me finish.

21. During the past ten years, 10,000,000 of our people have shifted, or gone, from the country to the cities. Food producers have decreased, and food consumers have increased by 10,000,000. Our population has increased 47% and our food products only 30% since 1890.

22. The hundreds of millions that have gone into automobiles, not one dollar in a thousand of which produces anything but a good time, or a joy ride, is a burden on production, and has been affecting prices, because they are nothing but luxuries.

23. Then there are all the other conveniences of life, such as telephones, electric light, etc.

Again, gentlemen, let us note where the gold has gone to during the last ten years, the period of increase in price. Germany got only $40,000,000, although her business has expanded enormously. England took only $30,000,000, while France took $300,000,000, Russia $200,000,000, and we absorbed $1,100,000,000. During the same time India took $433,000,000. Will anyone say that the prices in these various countries have in any way shown or reflected the amount of gold taken or absorbed?

Let some one come forward and prove that gold has[Pg 33] become cheaper by pointing out that prices in the various countries indicate its effects upon commodities. Lastly, let them explain the fact that while the banking resources of the world have increased from $16,000,000,000 to over $55,000,000,000, or increased three and one-half times, the gold for monetary purposes has only doubled, or increased from $4,000,000,000 to $8,000,000,000.

Mr. Merchant: I am more than satisfied and pleased that I asked you that question, for I knew it would be constantly bobbing up and bothering us, as we went along. When I interrupted you, you were speaking of gold and its functions as money.

Mr. Banker: Yes, and I assert that no other substance or thing possesses these functions, qualifications or characteristics, at least in no such degree as gold. Does anyone here deny that?

Mr. Lawyer: I think we must all agree to that, and further I would say that anything that did not possess all these functions, qualifications or characteristics in combination cannot very well be called money. To illustrate, if anything was used as a medium of exchange but depended upon its relation to gold for its acceptance it could not be called money.

I am fully aware that we speak of "cash" and "money," as anything we get in exchange for property, but this language does not mean anything definite, except as to the transaction.

I want to lay this down as an absolute rule, and something that no one of us should forget or overlook during our conversations.

"We should be careful to avoid calling any kind of credit instrument money, no matter how much used as a medium of exchange."

Let me read that again.

Uncle Sam: Now, let me see just what you mean by that. If I understand you, I think that is an attack upon me, upon my credit. For if my recollection serves me right, the United States Notes, or Greenbacks, have been[Pg 34] called money, and treated as money ever since I issued them during the war, way back in 1862, I think it was.

Mr. Banker: Well, Uncle Sam, do you think calling a thing something which it is not makes it that thing? To say that the moon is made of green cheese does not make it so. Now, here's one of your United States Notes, or Greenbacks. Do you recollect what you printed on that at the time you issued it, and have been printing on it ever since? This is what it says:

"The United States will pay the bearer $5.00."

That promise, or agreement, can mean but one thing, and that is that you will pay the bearer five times one dollar, or five times twenty-five and eight-tenths grains of gold, nine-tenths fine.

Now, it must be perfectly clear to you, indeed, the conclusion is incontrovertible, that that $5.00 United States Note, by which you agree to pay me $5.00 cash, can't be the $5.00 itself.

Mr. Farmer: No, by jocks, I know that is true. Tom Jones gave me a written agreement to deliver me a horse last Monday morning. I sent my boy over with his written promise for the horse, and he refused to deliver the horse. Certainly, his promise was not the horse; that's perfectly clear to me, for I did not get the horse, and that's the same kind of a deal that this United States Note is.

Mr. Laboringman: Yes, but Uncle Sam is no such flunker as that.

Mr. Banker: Well, he flunked from 1862 until 1879, for about seventeen years, and he came within an ace of flunking again in 1894. He is liable to flunk any time it suits him, if he should get into a tight place.

Uncle Sam: That's so, and the misfortune and the shame of it is, that I am left in a position where I am compelled to flunk.

Mr. Banker: I agree with you, but that only adds additional proof that this $5.00 bill, which is your promissory note, your I.O.U., or old due bill, given for boots,[Pg 35] mules and ammunition during the war, is not money at all, but a mere promise to pay money.

As you have just said, it is most unfortunate that you have been left in this position by your boys who have been going to Congress for the past fifty years, apparently without the intelligence, or courage, to relieve you of this disgraceful situation.

Uncle Sam: Well, if these United States Notes are nothing but my promissory notes, or due bills, agreeing to pay money, it is self-evident that they are not money. You have completely satisfied me on that point. Mr. Banker, how much of that kind of stuff have I got out?

Mr. Banker: $346,000,000.

Uncle Sam: Great Scott, I presume if I should get into trouble with some first-class nation, and have to go to war for a few years, and the people began to wonder whether I was going to pull through and pay my debts, that is to doubt my ability to stand the bill, and all that $346,000,000, then that $5.00 United States Note would not pass for $5.00.

Mr. Banker: Precisely so; that very note passed for only $1.75 at one time in 1864, or only 35 cents on the dollar.

Uncle Sam: Well, I wish Congress would get busy and pay these things off, so that I would be prepared for business, if anything should turn up compelling me to fight.

Mr. Manufacturer: From what you have said, Mr. Banker, and what Uncle Sam admits, I guess we all agree that the United States Notes, or Greenbacks, are not money at all, but just ordinary debts, or demands for money, and therefore cannot themselves be money, of course. But what have you to say about this National Bank Note here? How does this differ from the United States Notes or Greenbacks? Don't you admit that this is some sort or kind of money?

Mr. Banker: I do not. It is no more money than the United States Note. Just read what it says:

Mr. Manufacturer: I will. This is what it says:

"The First National Bank of New York will pay the bearer $5.00."

Mr. Banker: Don't you see that that bill is a mere I.O.U. of the Bank, nothing but a promise to pay five times twenty-five and eight-tenths grains of gold, nine-tenths fine, to the bearer? It does not differ in the slightest degree from the United States Note except that one is the promise of the First National Bank of New York, and the other the promise of Uncle Sam to pay $5.00. You can no more say that a promise of a bank to pay money is money than you can say that a promise of Uncle Sam to pay money is money. Both are debts, and both are demands for money, and therefore neither can be money.

Mr. Farmer: Gentlemen, while I must admit that Mr. Banker has completely, yes, absolutely, gotten away with the United States Notes and National Bank Notes and convinced us that they are not money at all, just watch me choke him with this silver slug, weighing 412½ grains, and bearing two invincible superscriptions.

First: "In God we trust."

Second: "United States of America, One Dollar." Mr. Banker, what have you to say about our Silver Dollar? Do you mean to tell me it is not money? That's what I want to know. Think of it, this dollar of our daddies not money.

Mr. Banker: Well, Mr. Farmer, if you'll follow me for half a minute, I will only have to ask you whether you yourself think it is money; and I will abide by your own decision. But, what I would rather do is to put it to a vote of the crowd, and if it is not unanimous I'll give it up.

Here is a 1 cent piece, bearing one of your invincible superscriptions, "United States of America, One cent." We have more to trust God for in one of these cents than we have in your Silver Dollar, and therefore it was a[Pg 37] grave oversight when Uncle Sam left off the other invincible superscription, "In God we trust," since this piece of bronze is worth only about one-thousandth part of a one-hundredth part of our Gold Dollar, or .0011890. Here is one of our nickels, bearing the same invincible superscription, "United States of America, V cents," which is worth about two-thousandths of one-hundredth part of a Gold Dollar, or .0026743. Here is a 10 cent piece, worth about 4 cents, or .04456, and here is a 25 cent piece, worth about 11 cents, or .11141. Here is a 50 cent piece, worth about 22 cents, or .22283. Here is the sacred dollar of our daddies, worth about 47 cents, or .47651.

Now, all these pieces of metal belong to the same class of coin from the cent to the dollar included, and are merely token coins.

Mr. Merchant: Well, what is a token coin?

Mr. Banker: A token coin is a piece of metal bearing the stamp of the Government, and passing at its face value, though the metal it contains is worth less than its face value.

This definition covers every piece of metal coin Uncle Sam makes except our gold coins, which are worth just as much and no more in the form of coin than they are in the form of metal, or gold bars. Now, Mr. Farmer, I want you to understand that the silver dollar is included in these token coins.

Mr. Manufacturer: Well, please tell me why do people take these pieces of money at their face value, when they are worth so much less than they pretend to be?

Mr. Banker: For the very simple reason that Uncle Sam over there redeems all the coins, smaller than one dollar, when presented to him in sums of five dollars or more, and because it is made the duty of his Secretary of the Treasury to maintain the face value of our silver dollar with our gold dollar by exchanging gold dollars for silver dollars, if anyone asks him to do so.

If the Government should pass a law refusing to re[Pg 38]deem our silver dollars with gold dollars, our silver dollar would then pass for just what the silver it contains would be worth from day to day. It is now worth 47 cents. In 1902 it was worth 40 cents. In other words, our silver dollar is not its own redeemer at 100 cents any more than the United States Notes or the National Bank Notes are their own redeemers. A silver dollar is a demand or a check calling for a gold dollar. The silver dollar, the United States Note, the National Bank Note all pass at their face value because they are convertible into gold, and are temporarily redeemed by Uncle Sam in gold, while gold is its own redeemer, and a ten dollar gold piece, or any other gold coin, is worth just as much, if hammered into a spike, or melted into a slug, as when it bears the stamp of Uncle Sam, certifying its quality and its quantity.

Mr. Lawyer: Mr. Banker, what are subsidiary coins?

Mr. Banker: All these token coins are properly called subsidiary coins. Let me read to you what Horace White says on that point:

"The word 'subsidiary' is usually applied to coins which constitute the small change of a country, and which are legal tender only for limited amounts. In the United States the silver dollar must be classed as subsidiary also; for, although it is full legal tender, the Government does not coin it for private individuals as it coins gold. It is subsidiary or subordinate to gold coin."

Mr. Laboringman: Uncle Sam, why do you make these token or subsidiary coins?

Uncle Sam: I make token or subsidiary coins out of silver, nickel, and copper just as a matter of convenience to the people, and as a result of custom also.

Mr. Lawyer: I think what Horace White says upon that point is particularly good, and answers your question, Mr. Laboringman, completely. White says:

"If subsidiary silver coins circulate at a value which is largely imaginary, the question may be asked, why not make them of some other metal, or even of paper?[Pg 39] There are no reasons except custom and convenience. A coin, not heavier than a half dollar, is more convenient than a piece of paper; it is cleaner, and in the long run is probably cheaper, as it does not require frequent renewal. A cheaper coin might be made out of some other metal, but it is generally best to conform to the habits of the people. Having been always accustomed to a silver subsidiary coinage no good reason is apparent why we should depart from it."

Mr. Merchant: Of course, you must use something besides gold to make the 50, 25, 10 and 1 cent pieces out of, because even a gold dollar would be found to be impracticable on account of its size. It would take a microscope to find a piece of gold worth only 5 cents.

Mr. Laboringman: And it would take a telescope to find a piece of gold worth only 1 cent.

Mr. Banker: Mr. White has this to say also about the silver dollar: "The silver dollar is a larger kind of subsidiary coin, and should be treated by the Government exactly as the smaller ones are treated. The Government has received the value of a gold dollar for every silver one emitted, and is therefore bound in equity to redeem the dollars as it redeems the halves, quarters and dimes.... There are additional reasons, however, for direct redemption of the silver dollar. One is that such coins are unlimited legal tender between individuals. Another is that there is a certain amount of public apprehension and lack of confidence touching any coin which passes for more than its metallic value."

"McLeod says that in 1691 in a posthumous work Sir William Petty pointed out that one metal only should be adopted as the standard unit, and other metals should be issued as subsidiary to the standard unit. The same doctrine was advocated with great force and at great length by Locke in 1693, and also by Harris in the middle of the last century, and was finally embodied in the great masterpiece of the subject 'Lord Liverpool's Coins of the Realm,' published in 1805."

Now, gentlemen, it must be apparent to everyone that a silver dollar is only another form of a debt of Uncle Sam over there, and that unless he continues to stand ready to exchange gold dollars for silver dollars, and so keep the silver dollars in circulation at 100 cents, they would circulate at their metal or bullion value, or at about 47 cents.

Mr. Farmer, do you think that stamping One Dollar upon that silver coin, added one-hundredth part of a cent to it, or affected its value in the slightest degree? Are you not convinced that it is not money at all, but a mere debt of Uncle Sam and that it is a mere demand for One Dollar in gold, and nothing more?

Mr. Farmer: I am bound to admit that you have surprised me, indeed paralyzed me, for I thought the Silver Dollar was money, but it is certainly exactly the same sort of thing that the Greenback and the National Bank Note is, and if they are not money, neither is the Silver Dollar money.

Mr. Merchant: I am sure we all agree on that point now, but what about this silver certificate? Do you pretend, Mr. Banker, that all our Silver Certificates are not money either?

Mr. Banker: That is just what I assert, but I claim still more than that with regard to the Silver Certificate; for, if you will read it, you will find that it is only a warehouse receipt for silver dollars, which have been deposited in the United States Treasury; and therefore is not a promise to pay anything, but simply to deliver so many silver dollars, which, as I have just demonstrated, must be redeemed in gold to keep them going for 100 cents on the dollar.

Mr. Lawyer: I am going to ask one question in this connection, and that is this. The United States Notes are a legal tender for everything except to pay taxes on goods coming into the country and interest on the debt and silver dollars are a legal tender, unless the contract is made payable in something else. Does not the fact that the[Pg 41] United States Note and the Silver Dollar are legal tender, make them money?

Mr. Laboringman: What's legal tender?

Mr. Lawyer: Anything which can be lawfully used in payment of a debt, or which creditors are compelled to accept, is called legal tender currency.

Mr. Banker: The fact that the United States Note and Silver Dollar are legal tender does not change the real character of either of them. Don't you know that the very fact that you are compelled, or think you are compelled, to make anything legal tender, to make it go for something it is not, lowers its value and depreciates that very thing?

The price of the United States Notes or Greenbacks from the day they were issued, until January 1, 1879, the date Uncle Sam redeemed his promise to pay gold for them, was simply a quotation of the government credit. This credit ranged from $1.00 to 35 cents. White says: "The difference between these extreme quotations may be taken to represent changes in the public credit, or various vicissitudes and states of mind, dependent upon the war."

Again he says: "In 1864 Congress attempted to check the depreciation of the currency by closing the gold exchange, and prohibiting sales of gold or foreign exchange for future delivery. The premium on gold advanced more rapidly after the passage of this Act than before, and Congress repealed it two weeks later."

Mr. Laboringman: Now, men, let me see if I understand what this is all about. If I have caught on to just what you have been saying about gold, which is all the money we have, and all these promises to pay money, these United States Notes, Bank Notes and Silver Dollars, the difference between gold coins and these promises is the same as the difference between a meal and a meal ticket. And when you come to the Silver Certificate that is only an order for a meal ticket.

Uncle Sam: By Jove, he's hit the thing plump and[Pg 42] square on the head, hasn't he, boys? But what I want to know now is how many of these meal tickets I've got out in one form or another? And, Mr. Banker, I want to know another thing. I want to know how many cans of pork and beans I have on hand to meet the meal tickets with?

Mr. Banker: Well, Uncle Sam, as I look at it you have 1,659,000,000 meal tickets out, and only 150,000,000 cans of pork and beans to meet the demand for meals.

Uncle Sam: Great Scott, what unbounded confidence the people must have in me not to shove those meal tickets in, before I get ready to supply the meals. What is worrying me is this, if anything should happen to cause any suspicion on that score, the jig would be up with me, and I can see the end of my credit; but of course that wouldn't be my finish. Now, what I want done is this: I want to shift these meal tickets over to the banks where they belong, or make full provision for them myself, so that I can stop worrying, and shall be ready for business, if called upon to meet a first-class nation in a protracted war.

By the way, Mr. Banker, just how did you make those meal tickets amount to 1,659,000,000 and that I had on hand only 150,000,000 cans of pork and beans to meet the meal tickets with? You must remember it takes one can of pork and beans to redeem one meal ticket.

Mr. Banker: Uncle Sam, you will remember that you have $346,000,000 of United States Notes to pay. You have also $563,000,000 Silver Dollars to redeem, and there are $750,000,000 National Bank Notes, making a total of $1,659,000,000, all resting on your $150,000,000 of gold in the reserve of your Treasury.

Uncle Sam: Yes, but I don't have to pay those National Bank Notes, do I?

Mr. Banker: Well, Uncle Sam, it's this way, you know, you have to pay them out of a 5% fund created by the bankers, but the bankers can turn right around and ask[Pg 43] you to redeem the United States Notes which you pay them for the National Bank Notes, in gold.

Uncle Sam: Mr. Banker, tell me another thing. If these silver certificates are nothing but warehouse receipts calling for silver dollars, and the silver dollars are nothing but token coins, then all these silver certificates are nothing but token or subsidiary coins in another form.

Mr. Banker: That is literally true.

Uncle Sam: And you say I have $563,000,000 of silver dollars out good for nothing but token or subsidiary coin?

Mr. Banker: Precisely so.

Uncle Sam: Now, what I want to know is this. How much of this silver is needed today to supply the people with the token or subsidiary coin, up to and including the $2.00 bills; that is, the $2.00 bill, the $1.00 bill, 50, 25, 10 and 5 cent pieces?

Mr. Banker: There are in circulation today about $400,000,000 of these various forms of subsidiary or token coins, or about $4.00 for every man, woman and child in this country.

Uncle Sam: What is the total amount of silver in the country then, of all kinds, silver dollars and pieces of silver less than one dollar? Tell me that.

Mr. Banker: There are, as I just said a moment ago, $563,000,000 of silver dollars and $147,000,000 of silver pieces less than one dollar, or a total of $710,000,000.

Uncle Sam: Well, well, you frighten me, for at the rate of four dollars each, the amount necessary for the convenience of the people, I am stacked up ahead for at least fifty years, or until we have about 200,000,000 of people; for you say we have all told $710,000,000 of silver coins in the country now. I want to tell you gentlemen, right now, that I want to get out of this hole, and I want to keep your mind steadily on that point as we go along.

The whole situation is a most embarrassing one. Tell me how much gold coin we have scattered about everywhere over the country?

Mr. Banker: There is about $1,850,000,000 of gold available in the country.

Uncle Sam: Then I am confident there is great plenty for the present, if we can devise some plan, or scheme, to avail ourselves of it.

Mr. Lawyer: I am convinced of that also, but the trouble is going to be to bring it together, centralize it and so mobilize it that we can make the most of it. We have learned one great and most important lesson tonight, and that is that the only money we have is gold, and that we cannot substitute an agreement to pay gold, a debt, a mere demand for gold itself, for it. Such a proposal when you think of it is an absurdity, a contradiction of terms.

To state the result of our conversation, or our conclusion, as I understand it, it is this: Money must be coined out of a commodity that is just as valuable in the form of a commodity as it is in the form of coin. A piece of gold weighing just the same as a $20 gold coin, if as pure, is worth just as much as a $20 gold piece.

Last Wednesday evening we all agreed that, as the result of our conversation, gold was the standard of value of the entire world, and was our standard of value as well.

Tonight, as I understand the result of our talk, we all agree that the only money we have in this country is gold coin; that our money is gold coin, and that our gold coin is our money.

Next Wednesday night let us investigate our currency and ask ourselves "What is currency?"

Before we separate, I want to read to you what Webster says currency is, because I want you to be thinking over the matter in the mean time. Webster says:

"Currency is the state or quality of being current; a continual course or passing from person to person or hand to hand; general acceptance; circulation."

Mr. Laboringman: You mean something that everyone takes and is glad to get.

Mr. Lawyer: Precisely so; it is that which is in circulation, or is given and taken as having value, or is representing value, as the currency of the country.

If we all keep this definition in mind, we shall have very little trouble next Wednesday evening in agreeing upon what currency is, and what it ought to be.

Uncle Sam: I want you men to remember one thing, and that is this, that we want no currency in this country that isn't as good as gold, and currently redeemed in gold coin to prove it. Nothing will satisfy Uncle Sam but the best, and don't you forget it. On top of that I want to plant another proposition, and that is this: It's not my business to be exchanging gold for that currency either. Compel the banks to do that, for that is their business.

But first, we will settle what our currency is, and what it ought to be.

Good Night.

WHAT IS CURRENCY?

Uncle Sam: Well, boys, when we parted last Wednesday night, it was agreed that we should take up for consideration and discussion tonight the question, "What is Currency?" And just before we left Mr. Lawyer read Webster's definition of Currency.

Mr. Merchant: I am very glad that he did so because it gave me a start, and set me to thinking, and as a result I became very much interested in the subject.

Mr. Banker: I have made the question of currency a study now for several years, and regard it of prime importance in any financial and banking system; but especially so considering the peculiar conditions existing in this country with our vast extent of territory, and the many distinct commercial centers there are here, each specializing in some one kind of production or industry. But more particularly is a right form of currency essential in this country because of the great number of our individual, independent banks now exceeding 25,000.

Mr. Manufacturer: Well, Mr. Banker, it strikes me that you are getting a trifle on to a side line. Let us get right down to business, and see if we can make any progress in determining just what Currency is, what kind we have and what kind we ought to have, if any change is to be made.

To my mind, and I have put all the spare time I had upon the question, that definition when fully understood described currency perfectly, and will help us amazingly in arriving at a clear idea of just what currency is as well as what it is not. Let me restate a part of it, which I think covers all of it. "Currency is that which is in circulation, or is given and taken as having value, or as representing value." That is, currency may have value[Pg 47] in itself, as illustrated by our gold coin, or may only represent value, as illustrated by our gold certificate.

Again, the definition described another quality, when it said that "currency passes from person to person, or from hand to hand; general acceptance; circulation." To be a piece of currency then, a thing may or may not have actual value, as a gold coin, or as a gold certificate, which can be exchanged for the coin. But the thing must have general acceptance, that is, it must be received by the people generally, as a matter of course, and without hesitation, and without taking anything from it, or adding anything to it, such as a stamp, or a signature.

That is, a piece of currency having passed through a thousand hands, remains identically the same thing, except the ordinary wear to which it has been subjected.

Mr. Merchant: Mr. Banker, taking that explanation as correct, what would you say that our currency consists of?

Mr. Banker: Our currency consists of the following things:

First: Gold coin, which is generally accepted, and has actual full value.

Second: Gold certificates, which are generally accepted, but have no actual value.

Third: All token, or subsidiary coin, including the silver dollar.

Fourth: Silver certificates.

Fifth: United States Notes.

Sixth: Bond-secured National Bank Notes.

Mr. Merchant: I read an article recently in which checks and drafts were spoken of as currency. Can it be possible that they can properly be called "currency"?

Mr. Banker: Certainly not. They come under an entirely different head, and I hope we shall spend an evening considering them very soon. Checks and drafts never pass from person to person and from hand to hand and are not of general acceptance. Herein lies the mark of distinction. Checks and drafts do not pass from person[Pg 48] to person and from hand to hand and are always of special acceptance, that is, they are considered before they pass. They are taken according to the strength of the makers, acceptors and endorsers and usually pass only by endorsement. We must make no such mistake because it will lead to a confusion of ideas.

Mr. Merchant: Mr. Banker, you have just told us of what our currency consisted. Gold coin, gold certificates, token coins, silver certificates, United States Notes and our bond-secured Bank Notes. Taken altogether I presume you would call that our currency system. Do you call it a good system?

Mr. Banker: It is our currency system, but it is without doubt the worst currency system in the world, if you include only respectable commercial nations.

Mr. Merchant: Well, Mr. Banker, what is wrong with it?