Title: Accounting theory and practice, Volume 2 (of 3)

a textbook for colleges and schools of business administration

Author: Roy B. Kester

Release date: April 15, 2023 [eBook #70556]

Language: English

Original publication: United States: Ronald Press, 1922

Other information and formats: www.gutenberg.org/ebooks/70556

Credits: Richard Tonsing and the Online Distributed Proofreading Team at https://www.pgdp.net (This file was produced from images generously made available by The Internet Archive)

A TEXT-BOOK FOR COLLEGES AND

SCHOOLS OF BUSINESS ADMINISTRATION

BY

ROY B. KESTER, Ph.D., C. P. A.

PROFESSOR OF ACCOUNTING, SCHOOL OF BUSINESS,

COLUMBIA UNIVERSITY

VOLUME II

(SECOND YEAR)

Twelfth Printing

NEW YORK

THE RONALD PRESS COMPANY

1922

Copyright, 1918, by

The Ronald Press Company

To Nancy

As a Tribute of Love and Tender

Memory to Her Mother

[Pg v]

A knowledge of the subject matter of Volume I is a prerequisite to the profitable study of the present work. Therefore, it may be well to review briefly the contents of the latter as an introduction to this book. In Volume I the attempt was made to formulate and illustrate the basic principles upon which the practice of accounting is founded. The principles of debit and credit were developed and their application explained—as related ultimately to the balance sheet and statement of profit and loss. The chief books of original entry (the voucher register excepted) and the various ledgers were described and illustrated. Columnar books, controlling accounts, methods and devices for preventing and detecting errors, methods for the proper handling of purchases, sales, cash, and trade discounts, and some phases of proportion and interest were discussed in detail.

Some special applications of accounting principles, as viewed in relation to the accounting problems involved therein, were also explained and illustrated under such heads as: notes receivable discounted and dishonored; consignments and approval sales; single and joint venture accounts; accounts current, their reconciliation and adjustment; instalment sales; sales for future delivery; single entry, its methods and the results attainable under it; etc.

From the standpoint of business organization, the accounting problems peculiar to the single proprietorship and the partnership were given full treatment. The advantages and disadvantages of the various types of organization, the rights and duties of owners among themselves [Pg vi] and to outsiders, the accounting procedure necessary under different conditions for changing from one form of organization to another, and other like items were set forth. Underlying the entire treatment of the subject was the guiding principle that accounting is never an end in itself, that its right to existence depends solely on the service it can render from the standpoint of administrative and financial management.

In content, the present volume is primarily a study of the corporation, its accounting and financial problems, although most of the material, in so far as it consists of a statement of general principles, is equally applicable to other types of organization. The emphasis of the volume is laid upon the problem of valuation as met in the commercial balance sheet. Chapters IV to XXVII inclusive comprise this portion of the subject matter. The other chapters treat miscellaneous matters, a knowledge of which is essential to the student of accounting. These latter form parts of the work of the second year as mapped out in the author’s scheme of instruction, whereby the whole field of accounting is covered by a well-graded three-year course of study. In this scheme cost accounting should be studied concurrently and as a parallel course with the work of this second volume. Only a bare outline of some of the problems and methods of cost accounting is presented in this volume.

As to the division of the text and its use in the general scheme, it is suggested that the first twenty-seven chapters should comprise the text material for the first semester, leaving the remainder for the second semester in which the chief emphasis should be placed on the solution of problems rather than on the formal classroom lecture. Hence the text material is lessened for this semester’s work, and the student’s main effort is directed towards the application to the problems of business of the principles already established. [Pg vii]

Instead of following the plan of the first volume in placing the practice work for the student at the end of each chapter of text, this material is presented separately in three appendices. It is believed that this will be found a more convenient arrangement.

The author desires to emphasize the need of ample practice work and at the same time to take a stand against the method of teaching accounting exclusively by the so-called laboratory or case method. A happy combination of text containing a statement of principles and showing methods of application, together with practice material intelligently made up so as to require a knowledge of principles before solution, is the desideratum in any course of instruction. Principles, theory, without application are barren and soon slip away, even if seemingly understood at the time. Practice without a thorough grounding in fundamental theory can never be sure of itself. An equitable division of the student’s time between theory and practice portions should be aimed at. In the present volume, while the time required for the practice assignments may at times seem heavy, an attempt has been made to keep it to the minimum deemed essential for adequate training either for general or professional use. It cannot be too emphatically stated that accounting as a profession ranks as to subject matter and the need for its services with the other professions. If it is to enjoy equal honor, dignity, and professional standing, teachers and practitioners must condemn without qualification the idea prevalent among many that a few months’ training suffices to turn out a finished product. Too often has such a course given point to the witticism that an accountant is a bookkeeper without a job. As stated in the preface of Volume I, a course of at least three years’ professional study is now quite generally recognized as essential. Accounting is so broad in its many ramifications that less than that gives inadequate training. [Pg viii]

The reception accorded the first volume and the report of results achieved in the classroom, through its use leads the author to hope that this second volume may have a courteous hearing and trial. Criticisms and suggestions will be much appreciated. The author hopes to be able to offer in the not too remote future the third and concluding volume in this series on general accounting.

The author is indebted for much assistance and counsel. Acknowledgment is due Miss Nina Miller of the Columbia staff and Eric Bodine for help in gathering and preparing much of the material for Chapters XXVIII to XXXIII; to H. A. Inghram of the University of Georgia, for preparation of a large part of Appendix D; to Leo Greendlinger and David E. Boyce for the use of problems prepared by them; and to his good friend, Joseph Gill, for help in reading the proof. To S. B. Koopman and James F. Hughes of the Columbia staff in second year accounting, the author is under special obligation for many suggestions. Mr. Koopman has furnished most of the problems for Appendix B, and has collected those for Appendix C.

As with Volume I, so in shaping the content of the present volume the author has had the good counsel and ever ready help of his chief, Robert H. Montgomery, and desires again to offer goodly acknowledgment, for his debt is large.

Columbia University,

New York City, August 5, 1918.

[Pg ix]

| CHAPTER | PAGE | ||

| I | The Corporation | 1 | |

| The Corporation | |||

| Classification and Definitions | |||

| Method of Ownership | |||

| Working Organization | |||

| Different Classes of Stock | |||

| Common Stock | |||

| Preferred Stock | |||

| Guaranteed Stock | |||

| Founders’ Stock | |||

| Debenture Stock | |||

| Stock of No Par Value | |||

| Watered Stock | |||

| Treasury Stock | |||

| Forfeited Stock | |||

| Bonus Stocks or Bonds | |||

| Accounting for Stocks | |||

| Discount on Stock | |||

| Premium on Stock | |||

| Property Exchanged for Stock | |||

| Treasury Stock Donated | |||

| Bonus Stock | |||

| Treasury Stock Purchased | |||

| Redemption of Preferred Stock | |||

| Forfeited Stock | |||

| Stock of No Par Value | |||

| Distinctive Records | |||

| Stock Ledger | |||

| Minute Book | |||

| Conclusion | |||

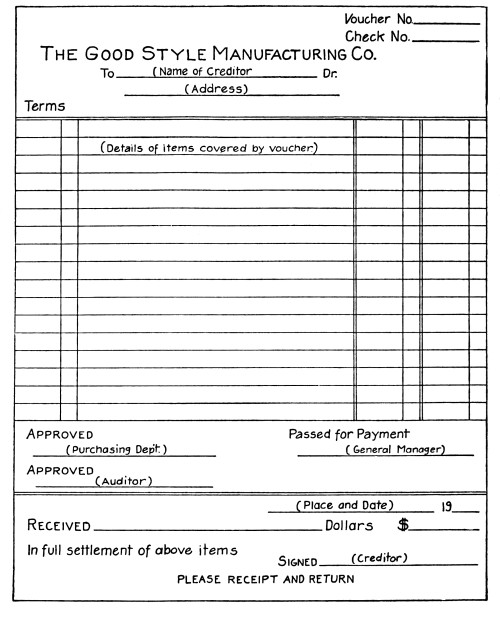

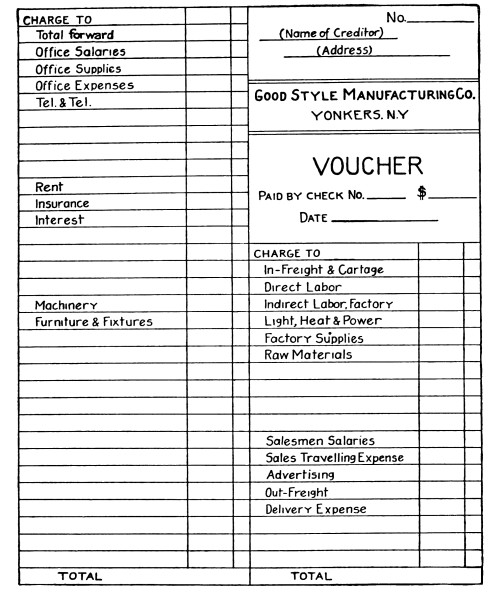

| II | The Voucher System | 26 | |

| Purchasing for the Manufacturing Business | |||

| Expansion of the Purchase Journal | |||

| Development of Voucher System | |||

| Definition and Description of Voucher | |||

| Operation of Voucher System | |||

| Voucher Check | |||

| Form of Voucher Register | |||

| Distribution of Vouchers | |||

| Posting of Summary Totals | |||

| Effect on Cash Book and Bank Account [Pg x] | |||

| Payment of Vouchers | |||

| Voucher Index of Creditors | |||

| Control of Vouchers Payable | |||

| Introduction of System | |||

| Purchase Returns and Allowances | |||

| Partial Payments | |||

| Handling of Notes Payable | |||

| Cash Discount on Purchases | |||

| Modifications of System | |||

| Summary of Operation and Advantages | |||

| III | Factory Costs | 49 | |

| Difference Between Factory and Financial Accounting | |||

| Definitions of Terms | |||

| Special Purposes of Cost Records | |||

| Nature of Raw Materials and Supplies | |||

| Accounting for Material Cost | |||

| Direct and Indirect Labor | |||

| Time-Keeping Records | |||

| Pay-Roll | |||

| Safeguarding the Pay-Roll | |||

| Distribution of Labor Charges | |||

| Expense | |||

| Summary of Manufacturing Cost | |||

| IV | The Balance Sheet | 60 | |

| Business Methods under the Microscope | |||

| The Reading of the Balance Sheet | |||

| Definition | |||

| Relation Between Balance Sheet and Trial Balance | |||

| Form of Balance Sheet | |||

| Purpose and Uses | |||

| Types of Balance Sheet | |||

| Origin of English Form of Balance Sheet | |||

| Variation of English Form | |||

| Balance Sheet Titles | |||

| Grouping and Classification | |||

| Arrangement of Groups | |||

| Report and Account Forms | |||

| Valuation Accounts | |||

| Statutory Requirements as to Frequency of | |||

| Balance Sheets | |||

| Condensation of Information in the Balance Sheet | |||

| Use of Supporting Schedules | |||

| V | General Principles of Valuation | 81 | |

| Content of the Balance Sheet | |||

| Valuations for Rate Regulation | |||

| Valuation for Sale and Purchase | |||

| Other Kinds of Valuations | |||

| Going Concern Valuation | |||

| Kinds of Value | |||

| Source of Data as to Values | |||

| Cost Value the Usual Basis [Pg xi] | |||

| Definition of Capital and Revenue Expenditures | |||

| Organization Expenses | |||

| Definition of Replacements, Renewals, Maintenance, etc. | |||

| Treatment of Renewal of Parts | |||

| Treatment of Cost-Cutting Changes | |||

| Asset Subject to Depreciation a Deferred Charge to Operations | |||

| Authorization of Booking Capital Expenditures | |||

| Repairs on Second-Hand Plant | |||

| Construction Costs | |||

| Distinction Between Capital and Revenue Expenditures | |||

| Often Based on Opinion | |||

| Main Groups of Asset Items | |||

| Valuation of Liability Items | |||

| Over- and Under-Valuation | |||

| The Balance Sheet an Expression of Opinion | |||

| VI | Depreciation—Aspects and Definitions of Terms | 99 | |

| Aspects of Depreciation | |||

| Definitions | |||

| Authoritative Opinions | |||

| Why the Depreciation Factor Arises | |||

| Actual or Absolute Depreciation | |||

| Theoretical Depreciation | |||

| Comparison of Actual and Theoretical Depreciation | |||

| “Accounting” and “Fair” Depreciation | |||

| Complete and Incomplete Depreciation | |||

| Individual and Composite Depreciation | |||

| Physical and Functional Depreciation | |||

| Deferred Maintenance and Accrued Depreciation | |||

| Attitude of the Law | |||

| Decision of Supreme Court | |||

| Recognition of the Depreciation Factor | |||

| Distinction Between Repairs and Renewals | |||

| Depreciation and Plant Efficiency | |||

| Unit Efficiency | |||

| Depreciation and Fluctuations in Market Value | |||

| Distinction Between Depreciation and Depletion | |||

| Effect on Different Kinds of Business | |||

| VII | Depreciation—Its Causes | 120 | |

| Analysis of Causes | |||

| Age as a Cause of Depreciation | |||

| Wear and Tear of Use | |||

| Functional Depreciation | |||

| Inadequacy as a Factor | |||

| Inadequacy Through Change of Policy | |||

| Inadequacy Through Motives of Economy | |||

| Inadequacy Due to Unforeseen Development | |||

| Inadequacy Imposed from Without | |||

| Obsolescence as a Cause | |||

| Treatment of Obsolescence | |||

| Contingent Depreciation | |||

| Terminable Rights [Pg xii] | |||

| Effective Depreciation | |||

| VIII | Depreciation—Factors of Rate Determination | 136 | |

| Fundamental Purpose of Depreciation | |||

| Depreciation a Cost of Operation | |||

| Complication of Short Fiscal Periods | |||

| The Factor of Idle Time | |||

| Depreciation a Means of Financing | |||

| Danger of the Financing Viewpoint | |||

| The Standardization of Depreciation Rates | |||

| Effect of Local Conditions | |||

| Factors in Determining Depreciation Rate | |||

| Bases of Normal Rate | |||

| Policies as to Repairs | |||

| Depreciation Rate an Engineering Problem | |||

| Attitude of Regulatory Bodies | |||

| Methods of Handling Repairs | |||

| IX | Depreciation—Methods of Calculating | 150 | |

| Methods of Calculation | |||

| Factors of Calculation | |||

| Symbols to be Used | |||

| 1. Proportional Methods | |||

| (a) Straight Line Method | |||

| (b) Working Hours Method | |||

| (c) Composite Life Method | |||

| (d) Service Output Method | |||

| 2. Variable Percentage Methods | |||

| (a) Fixed Percentage of Diminishing Value Method | |||

| (b) Changing Percentage of Cost Less Scrap Method | |||

| (c, d) Arbitrary Methods | |||

| 3. Compound Interest Methods | |||

| (a) Sinking Fund Method | |||

| (b) Annuity Method | |||

| (c) Unit Cost Method | |||

| 4. Miscellaneous Methods | |||

| (a) Maintenance Method | |||

| (b) Replacement Method | |||

| (c) The Fifty Per Cent Method | |||

| (d) Appraisal Method | |||

| (e) Insurance Method | |||

| (f) Gross Earnings Method | |||

| Condition Per Cent | |||

| X | Depreciation—Appraisement of the various Methods | 173 | |

| General Considerations | |||

| Ideal Basis for Distribution of Depreciation Charge | |||

| 1. Proportional Methods | |||

| (a) Straight Line Method | |||

| (b) Working Hours Method | |||

| (c) Composite Life Method | |||

| (d) Service Output Method [Pg xiii] | |||

| 2. Variable Percentage Methods | |||

| (a) Fixed Per Cent of Diminishing Value Method | |||

| (b) Sum of Expected Life-Periods Method | |||

| (c, d) Arbitrary Methods | |||

| 3. Compound Interest Methods | |||

| General Considerations | |||

| (a) Sinking Fund Method | |||

| (b) Annuity Method | |||

| (c) Unit Cost Method | |||

| 4. Miscellaneous Methods | |||

| (a) Maintenance Method | |||

| (b) Replacement Method | |||

| (c) Fifty Per Cent Method | |||

| (d) Appraisal Method | |||

| (e) Insurance Method | |||

| (f) Percentage of Gross Earnings Method | |||

| Effect on Return on Investment | |||

| XI | Recording Depreciation on the Books | 187 | |

| Methods Commonly Employed | |||

| Renewals and Replacements | |||

| Subsidiary Records | |||

| Grouping and Classification of Plant Assets | |||

| Form of Plant Ledger | |||

| Asset Record | |||

| Periodic Revision of Rates | |||

| Frequency of Revision of Rates | |||

| Test of Condition Per Cent | |||

| Composite and Group Rates | |||

| The Reserve as an Index of Financial Condition | |||

| The Reserve in Relation to Expanding Plant | |||

| Reserve as Related to Efficiency | |||

| Reserve Not Based on Cost of Replacement | |||

| The Financing of Replacements | |||

| Secret Reserve | |||

| Insufficient Charge | |||

| Appreciation as an Offset to Depreciation | |||

| Appreciation Due to Physical Changes | |||

| Appreciation Due to Adaptation to Use | |||

| Unearned Increment | |||

| Depreciation Policy and Stockholders | |||

| XII | Cash and Mercantile Credits | 210 | |

| Introduction | |||

| What Cash Includes | |||

| Stamps Remitted as Cash | |||

| Temporary Cash Disbursements | |||

| Disposition of Cash Funds | |||

| Cash Held Abroad | |||

| Accounts and Notes Receivable [Pg xiv] | |||

| Objection to the Title, Accounts Receivable | |||

| Risk for Credit Losses | |||

| Risk and Length of Credit Period | |||

| Analysis of Customers’ Accounts as the Basis | |||

| for Estimate of Bad Debts | |||

| Basis of Estimate of Bad Debts | |||

| Discounts and Collection Costs | |||

| Valuation of Other Receivable Items on Open Account | |||

| Loss on Notes Receivable | |||

| Interest on Notes Receivable | |||

| Balance Sheet Titles for Notes Receivable | |||

| XIII | Merchandise Stock-in-Trade | 225 | |

| Definition and Scope of Term | |||

| Valuation at Market or Cost Price | |||

| Objections to Valuation at Less than Cost | |||

| Anticipation of Profits or Losses Undesirable | |||

| Method of Treatment and Summary | |||

| Depreciation of Stock-in-Trade | |||

| Full Costs of Stock-in-Trade | |||

| The Distribution of Costs Over Stock-in-Trade | |||

| The Pricing of the Inventory | |||

| Valuation of Manufacturing Inventory | |||

| Contracts and Length of Cost Period | |||

| Valuation of Scrap | |||

| Inventory-Taking | |||

| Perpetual Inventory | |||

| XIV | Temporary Investments; Accrued and Deferred Items | 241 | |

| Temporary Investments |

|||

| Nature of Temporary Investments | |||

| Valuation of Temporary Investments | |||

| Reserve for Investment Fluctuations | |||

| “Stock Rights” on Investments | |||

| Cost of Investments | |||

| Valuation of Bonds | |||

| Valuation of Unissued Stock | |||

| Valuation of Treasury Stock | |||

| Summary of Valuation Formula | |||

| Accrued and Deferred Items |

|||

| Nature of Accrued Income | |||

| Inadequacy of Cash Method of Handling Accruals | |||

| Correct Method of Handling Accruals | |||

| Showing of Accrued Items on Balance Sheet | |||

| Valuation of Accrued Items | |||

| Accounting for Accrued Income | |||

| Illustration of Different Methods of Recording Accrued Items | |||

| Prepaid Items—Definitions and Kinds | |||

| Valuation of Prepaid Items | |||

| Danger of Overvaluation [Pg xv] | |||

| Accounting for Deferred Debit and Other Items | |||

| XV | Permanent Investments | 258 | |

| Nature of Permanent Investments | |||

| Permanent Investments as an Aid to Operation | |||

| Valuation of Permanent Investments | |||

| Holding Company and Subsidiary Enterprises | |||

| Controlling Investments | |||

| Advances to Subsidiary Concerns | |||

| Rules for Valuation | |||

| Investments in Partial Holdings | |||

| Investments Producing No Income | |||

| Bond Values and Market Interest Rates | |||

| Nature of Bond Discount or Premium | |||

| Record of Bond Investments | |||

| Amortization of Bond Discount and Premium | |||

| Formulas for Compound Interest | |||

| Formulas for Annuities | |||

| Formulas for Bond Valuation | |||

| Valuation of Sinking Funds | |||

| Valuation of Investments in Land | |||

| XVI | Machinery and Tools, Furniture and Fixtures, | ||

| and Other Equipment | 279 | ||

| General Considerations | |||

| Distinction between Personalty and Real Property | |||

| Machinery and Tools | |||

| Accounting Records | |||

| Operation of Machine Accounts | |||

| Valuation of Machinery and Tools | |||

| Estimate of Depreciation | |||

| History of Machine | |||

| Standards of Operation | |||

| Abnormal Operation | |||

| Map of Machine Location | |||

| Methods of Application of Depreciation | |||

| Basis of Valuation | |||

| Scrap Material | |||

| Accounting for Tools | |||

| Depreciation on Hand Tools | |||

| Valuation of Home-Made Machinery and Tools | |||

| Expenditure for Rearrangement of Machinery | |||

| Definition of Furniture and Fixtures | |||

| Valuation of Furniture and Fixtures | |||

| Delivery Equipment—Definition and Valuation | |||

| Carriers and Containers—Valuation | |||

| Patterns, Molds, etc.—Valuation | |||

| Disposal of Assets | |||

| XVII | Buildings, Land, and Wasting Assets | 297 | |

| Definition of Real Property | |||

| Cost of Buildings | |||

| Valuation of Buildings | |||

| Betterments on Leased Buildings [Pg xvi] | |||

| Application of Depreciation | |||

| Accounting for Land | |||

| Valuation of Land | |||

| Depreciation or Appreciation of Land | |||

| Appreciation of Land Values | |||

| Depreciation in Land Values | |||

| Valuation of Land Investments | |||

| Mortgages on Land | |||

| Donated Land | |||

| Land as Stock-in-Trade | |||

| Wasting Assets—Definition and Characteristics | |||

| Dividends May Include Return of Capital | |||

| Basis of Depletion Charge | |||

| Application of Income Tax to Wasting Assets | |||

| Depreciation on Buildings and Machinery of a Wasting Asset | |||

| Unusual Risks | |||

| Water Rights | |||

| Leaseholds | |||

| XVIII | Intangible Assets—Patents, Franchises, Good-Will | 316 | |

| General Considerations | |||

| Patents a Monopoly Grant | |||

| Purchase of Patents | |||

| Patents Developed Within the Plant | |||

| Patents Purchased and Not Used | |||

| Elements of Depreciation on Patents | |||

| Service Life of Patents | |||

| Booking Depreciation on Patents | |||

| Accounting Classification of Depreciation on Patents | |||

| Royalties | |||

| Relation of Depreciation Rate to Cost of Manufacture | |||

| Sale Price of Patents | |||

| Copyrights | |||

| Trade Secrets | |||

| Trade-Marks | |||

| Franchises—Definition and Kinds | |||

| Depreciation on Franchises | |||

| Organization Expenses | |||

| Good-Will—Definition and Nature | |||

| Local and Personal Character of Good-Will | |||

| Difficulty of Valuing Good-Will | |||

| Creation of Good-Will by Advertising | |||

| Valuation of Good-Will Based on Normal Profits | |||

| Valuation of Good-Will Based on Excess Profits | |||

| Valuation of Good-Will Based on Capitalization of Profits | |||

| False Good-Will to Cover Capital Deficiency | |||

| Periodic Revaluation of Good-Will | |||

| XIX | Liabilities on the Balance Sheet; Current and | ||

| Contingent Liabilities | 339 | ||

| Form and Valuation | |||

| Arrangement on Balance Sheet [Pg xvii] | |||

| Items Within Groups | |||

| Cancellation of Liabilities Against Assets | |||

| Inventory of Liabilities | |||

| Contingent Liabilities | |||

| Current Liabilities |

|||

| Loans from Bank | |||

| General Classification of Notes | |||

| Accounts Payable | |||

| Accrued Expenses | |||

| Booking of Accrued Expenses | |||

| Deferred Credits | |||

| Nature of Contingent Liabilities |

|||

| Statement of Contingent Liabilities | |||

| Notes and Drafts Transferred | |||

| Guarantees as a Contingent Liability | |||

| Long-Term Leases | |||

| Purchases for Future Delivery | |||

| Pending Lawsuits | |||

| Stock Not Fully Paid | |||

| Accumulated Dividends on Preferred Stock | |||

| Signature to Surety Bond | |||

| XX | Fixed Liabilities—Bonds and Mortgages | 356 | |

| Nature of Fixed Liabilities | |||

| Purpose of Fixed Liabilities | |||

| Corporation Bonds | |||

| Nature of Bonds | |||

| Difference Between Bond and Real Estate Mortgages | |||

| Kinds of Corporation Bonds | |||

| Authority for the Issue of Bonds | |||

| Financial Considerations Involved in Issue | |||

| Bonds versus Stock Issues | |||

| Accounting for Bond Issue | |||

| Entry of Issue on Books | |||

| Entry of Premium or Discount on Books | |||

| Entry of Interest Payments on Books | |||

| Relation of Bond Interest to Premium or Discount | |||

| Example of True Interest Cost | |||

| Presentation on Balance Sheet | |||

| Other Fixed Liabilities | |||

| XXI | Capital Stock and its Valuation | 372 | |

| Problems in Valuation | |||

| Kinds of Stock | |||

| Par, Real, and Market Values | |||

| Value Dependent upon Earning Capacity | |||

| Increase of Book Capitalization | |||

| Capitalization on Cost | |||

| The Law and Stock Issues | |||

| Treatment of Discount or Premium | |||

| Valuation of Stock Issued for Property [Pg xviii] | |||

| Valuation of Treasury Stock | |||

| Redemption and Reduction of Capital Stock | |||

| Dividend Stock | |||

| Stock Issued as a Bonus | |||

| Unissued and Treasury Stock on the Balance Sheet | |||

| Preferred Stock Covered by Redemption Contract | |||

| XXII | Profits | 387 | |

| Difficulty of Determining Profits | |||

| Economic Definition | |||

| Legal Definition | |||

| Accounting Definition | |||

| Methods of Determining Profits | |||

| The Problem a Question of Valuation | |||

| Effect of Asset Losses on Future Profits | |||

| Legal Decisions as to Asset Losses | |||

| Loss Charged Against Current Profits | |||

| Loss Treated as Deferred Expense Charge | |||

| Loss Charged to Capital | |||

| Profit on Work in Progress | |||

| Goods Made for Stock but Not Sold | |||

| Goods Made to Order | |||

| Profits on Long-Term Contracts | |||

| Profit on Goods Awaiting Delivery | |||

| Interdepartment Profits | |||

| Profits Due to Appreciation of Assets | |||

| Capital Profits | |||

| XXIII | Surplus and Reserves | 407 | |

| Definition | |||

| Creation of Margin | |||

| Disposition of Profits | |||

| Reserves | |||

| Different Meanings of Reserves | |||

| Reserve for Bad Debts | |||

| Under- and Over-Estimate of Reserves | |||

| Depletion Reserves | |||

| Operating Reserves for Accrued Costs | |||

| Collection Costs Not under Contract | |||

| Sales Discounts on the Balance Sheet | |||

| Distinction Between Reserves and Accrued Items | |||

| Contingent Reserves | |||

| Deferred Income—Misuse of Term | |||

| Proprietorship Reserves | |||

| Secret Reserves | |||

| Argument for Secret Reserve | |||

| Argument Against Secret Reserve | |||

| Earmarking of Reserves | |||

| Continuity of Reserve Policy | |||

| Covered Reserves | |||

| Classification of Reserves | |||

| Legitimate Use of Surplus Account [Pg xix] | |||

| Statement of Surplus | |||

| XXIV | Dividends | 428 | |

| Introduction | |||

| Disposition of Corporation Profits | |||

| Shareholders’ Rights as to Profits | |||

| Directors’ Control over Profits | |||

| Provisos as to Declaration of Dividends | |||

| Stockholders’ Rights to Dividends | |||

| Declaration of Dividends | |||

| Liability of Director | |||

| Revocation of Dividends | |||

| Payment of Dividends | |||

| Dividends Paid as Salaries | |||

| Methods of Paying Dividends | |||

| Borrowing to Pay Dividends | |||

| Dividends Paid in Property, or by Borrowing on Property | |||

| Bond and Scrip Dividends | |||

| Stock Dividends | |||

| Dividends Proportional to Holdings | |||

| To Whom Payable | |||

| Accounting Record | |||

| Relation of Capital Losses to Dividends | |||

| Liquidating Dividends | |||

| XXV | The Sinking Fund | 447 | |

| Origin and Use | |||

| Definitions | |||

| Mathematical Principles on which Based | |||

| Accumulation Based on Agreement | |||

| Effect of Settlement of Debt | |||

| Relation of Fund to Profits | |||

| Accounting for Sinking Fund | |||

| The Sinking Fund on the Balance Sheet | |||

| Entries to Sinking Fund | |||

| Booking the Trustee’s Report | |||

| Treatment of Income and Expense | |||

| Final Disposition of Fund | |||

| Treatment of Sinking Fund Reserve | |||

| Relation Between Depreciation and Sinking Fund | |||

| XXVI | Problems in Connection with the | ||

| Profit and Loss Summary | 466 | ||

| Interrelation of Profit and Loss and Balance Sheet | |||

| Periodic Adjustments | |||

| Interest as a Cost of Manufacture | |||

| Arguments Against the Inclusion of Interest | |||

| Problem of Charging Interest on Books | |||

| Unrealized Profits | |||

| Corporation Dividends | |||

| Discount on Bonds | |||

| Sinking Funds | |||

| Working Capital | |||

| The Correction of Closing Errors [Pg xx] | |||

| XXVII | The Profit and Loss Summary—Form and Content | 477 | |

| Standardization of Form | |||

| Synonymous Terms | |||

| Cost of Goods Sold—Manufacturing Concern | |||

| Cost of Goods Sold—Trading Concern | |||

| Further Differentiation of Terms | |||

| Desirability of Uniformity in Terms Used | |||

| Profit and Method of Showing | |||

| Form of Presentation—Account Form | |||

| Non-Technical or Report Form | |||

| Examples of Forms of Presentation | |||

| Form for Manufacturers and Merchants | |||

| Content and Manner of Showing | |||

| Supporting Schedules | |||

| Adjustment of Inventories | |||

| Selling Expense and Administrative Schedules | |||

| Schedules for Special Needs | |||

| XXVIII | Liquidation of a Corporation | 493 | |

| Reasons for Liquidating—Partial and Complete Liquidation | |||

| Current Assets Transferred into Fixed Assets | |||

| Tying up Cash in Stocks of Material | |||

| Unwise Use of Cash for Paying Dividends | |||

| Inability to Secure Cash for Refunding Operations | |||

| Excessive Borrowing on Short-Term Securities | |||

| Losses in Conducting the Business | |||

| Loss Through Fraud, Theft, or Unavoidable Causes | |||

| Methods of Liquidation | |||

| Liquidation under Bankruptcy | |||

| Liquidation under Voluntary Dissolution | |||

| Liquidation under Receivership | |||

| Status of Creditors in Liquidation | |||

| Accounting for Liquidation | |||

| XXIX | Combinations and Consolidations | 507 | |

| Reason for Combination | |||

| Types of Consolidation | |||

| Accounting for the Holding Company | |||

| Distinction between Consolidation and Merger | |||

| Formation of Consolidation and Merger | |||

| Principles of Valuation of the Constituent Companies | |||

| Fundamental Principle of Equalization of Conditions | |||

| Valuation of Partnership | |||

| Earning Capacity | |||

| Good-Will | |||

| Capitalization of a Consolidation or a Merger | |||

| Payment of Amalgamated Interests | |||

| Closing the Books of the Merged Concerns | |||

| Opening the Books of the Merger [Pg xxi] | |||

| XXX | Branch House Accounting | 521 | |

| Advantages of Branch and Agency System | |||

| Agency and Branch Differentiated | |||

| Degree of Control Desired | |||

| Factors of Successful Management | |||

| Main Principles of Branch Accounting | |||

| Agency Accounts | |||

| Branch Accounting Records | |||

| Illustration of Simple Branch Accounts | |||

| Illustration of More Complex Branch Accounts | |||

| Purchases | |||

| Sales | |||

| Adjustments on Branch and Head Office Books | |||

| Example of Adjusting Entries | |||

| Reports from the Branch | |||

| Examples of Reports | |||

| XXXI | Branch House Accounting (Continued) | 542 | |

| Foreign Exchange | |||

| The Accounting Problem of the Foreign Branch | |||

| Accounts Opened on Books | |||

| Handling Fluctuations in Foreign Exchange | |||

| Conversion of Branch Results | |||

| Illustrative Bookkeeping Problems | |||

| Local Supervision of the Foreign Branch | |||

| The Foreign Sales Agency | |||

| Method of Conversion of Results | |||

| The Foreign Purchasing Agency | |||

| XXXII | Suspense Accounts; Numbered Accounts; | ||

| Adjustment of Fire Losses | 556 | ||

| Suspense Accounts |

|||

| Definition of Suspense Accounts—General Purpose | |||

| Reserve for Doubtful Accounts as a Suspense Account | |||

| Use of Suspense Ledger | |||

| Accounts Receivable Hypothecated | |||

| Accounting for Accounts Receivable Discounted | |||

| Numbered Accounts |

|||

| Allotment of Numbers to Accounts | |||

| Adjustment of Fire Losses |

|||

| The Insurance Contract | |||

| Requirements in Case of Loss | |||

| Determination of Value of Loss | |||

| Adjustment of Differences | |||

| Effect of Coinsurance Clause | |||

| Method of Record-Keeping to Facilitate Ready Adjustment | |||

| Adjusting Entries for Fire Losses [Pg xxii] | |||

| XXXIII | Statistics in Business; Private Books; Journal | ||

| Vouchers; Building Expenses and Income | 581 | ||

| Statistics in Business |

|||

| Value of Business Statistics | |||

| Railroad Statistics | |||

| Manufacturing Statistics | |||

| Mercantile Statistics | |||

| Use of Graphs in the Presentation of Statistics | |||

| Advantages of the Use of Graphs | |||

| Principles of Graph Construction | |||

| Private Books |

|||

| Purpose and Content | |||

| Operation of Private Books | |||

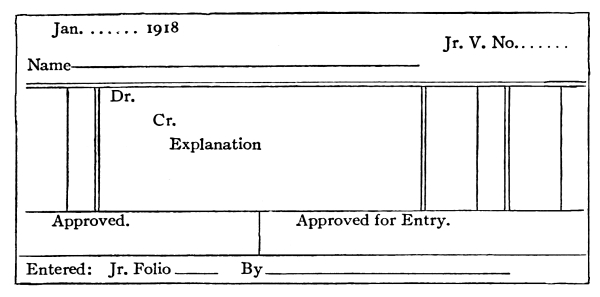

| Journal Vouchers |

|||

| Need for the Journal Voucher | |||

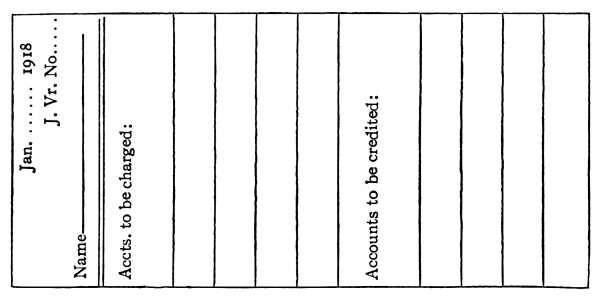

| Index to Journal Vouchers | |||

| Content of Voucher | |||

| Other Methods of Authorizing Entries | |||

| Building Expenses and Income |

|||

| Allocation of Building Expense | |||

| XXXIV | The Consolidated Balance Sheet and | ||

| Profit and Loss Summary | 600 | ||

| Purpose and Function | |||

| Problem of Partial Ownership | |||

| Conditions under which Used | |||

| The Setting Up of the Consolidated Balance Sheet | |||

| Showing of Intercompany Accounts | |||

| Showing of Notes Discounted | |||

| Reconcilement of Current Accounts | |||

| Valuation of Inventory | |||

| Reserve for Intercompany Profits | |||

| Valuation of Inventory—Minority Interests | |||

| Valuation of Liabilities | |||

| Showing of Capital Stock | |||

| Showing of Surplus | |||

| Showing of Deficit | |||

| Showing of Profit and Loss Summary | |||

| The Consolidated Profit and Loss Summary | |||

| Illustration of Consolidated Balance Sheet | |||

| XXXV | Accounts and Reports of Receivers and Trustees | 620 | |

| Appointment of Assignee or Receiver | |||

| Appointment of Trustee | |||

| Accounts and Reports of a Receiver in Equity | |||

| Reports to the Court | |||

| Accounts and Reports in Bankruptcy Proceedings |

|||

| Initial Statements Presented to the Court | |||

| Reports and Accounts of Receiver or Trustee [Pg xxiii] | |||

| Liquidating Dividends | |||

| Relative Standing of the Creditors | |||

| Statement of Affairs | |||

| Basis of Valuations in Statement of Affairs | |||

| Deficiency Account | |||

| Illustration of Statement of Affairs and Deficiency Account | |||

| Realization and Liquidation Account |

|||

| Evolution of the Realization and Liquidation Account | |||

| Supporting Schedules | |||

| The Question of Cash | |||

| The Handling of Valuation Reserves | |||

| Illustration of Realization and Liquidation Statement | |||

| Uses to which Realization and Liquidation Statement May be Put | |||

| Liquidation of a Partnership by Instalments |

|||

| Nature of the Problem | |||

| Illustration of Liquidation by Instalments | |||

| Appendix | A—Practice Work for Student—First Half-Year | 655 | |

| B—Practice Work for Student—Second Half-Year | 694 | ||

| C—Miscellaneous Problems for Supplementary Work | 727 | ||

| D—Review Questions | 755 | ||

FORMS AND CHARTS

| Page | |

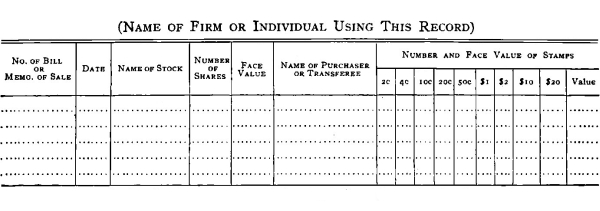

| Stock Book or Stock Ledger | 22 |

| Stock Book to be Kept by Brokers | |

| (New York Form Prescribed by Comptroller) | 23 |

| Stock Book to be Kept by Corporations and Transfer Agents | |

| (New York Form Prescribed by Comptroller) | 23 |

| Voucher | 30, 31 |

| Voucher Check—Double | 33 |

| Voucher Check—Single | 34 |

| Voucher Register | 35 |

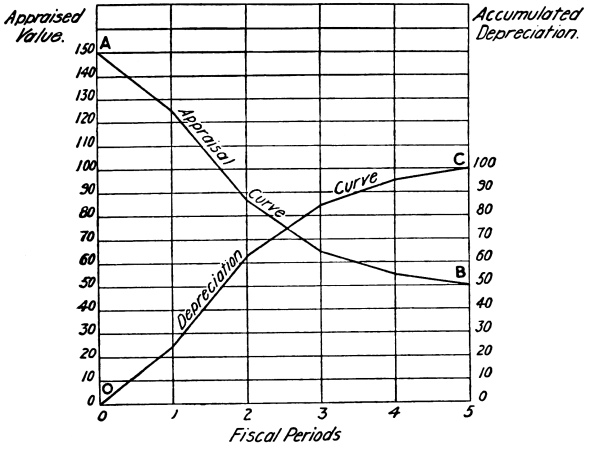

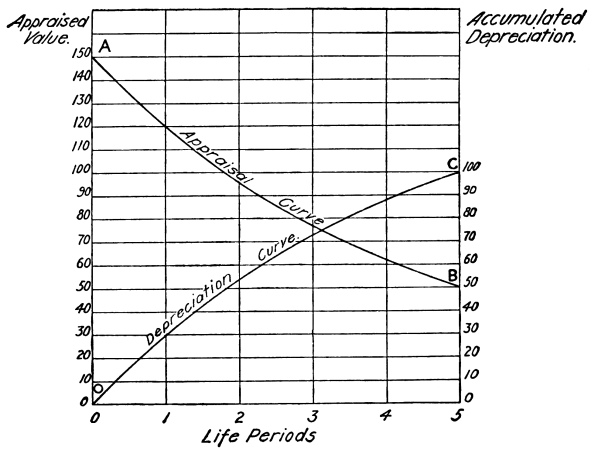

| Chart Showing Actual and Theoretical Depreciation | 105 |

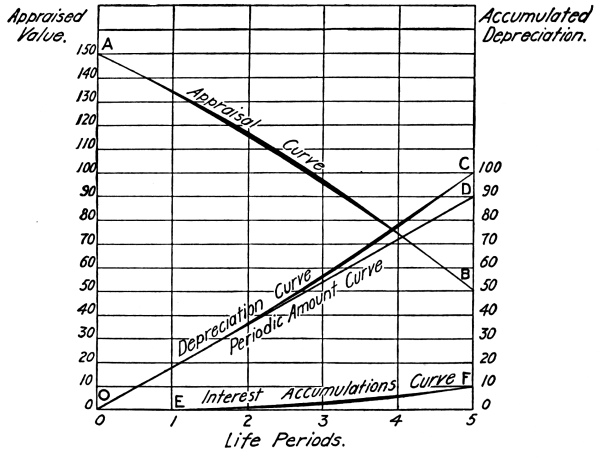

| Chart Showing Progress of Uniform Depreciation | |

| and of Diminishing Efficiency | 115 |

| Graphic Chart—Straight Line Method | 153 |

| Graphic Chart—Working Hours Method | 155 |

| Graphic Chart—Fixed Percentage of Diminishing Value Method | 158 |

| Graphic Chart—Sinking Fund Method | 162 |

| Graphic Chart—Annuity Method | 166 |

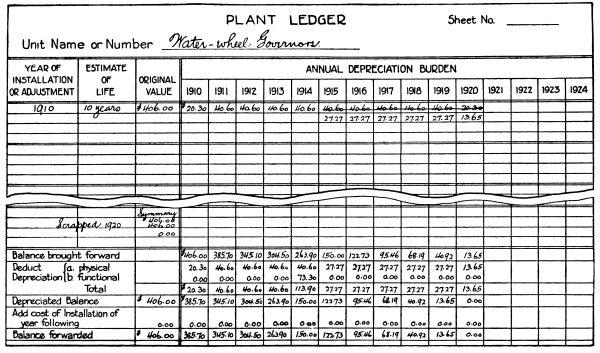

| Plant Ledger | 193 |

| Branch Report to Head Office | 541 |

| Head Office Ledger Account—Summary of Branch Expenses | 541 [Pg xxiv] |

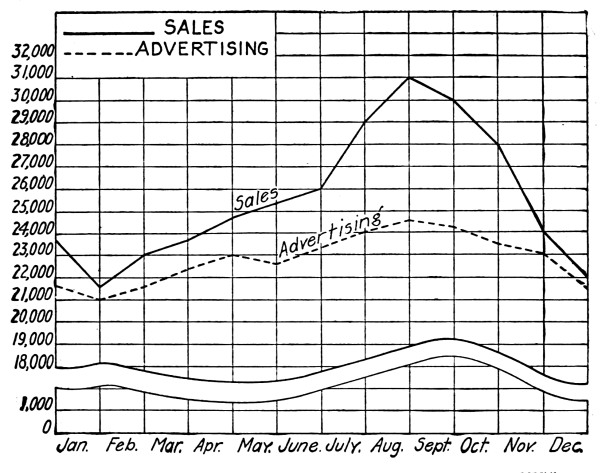

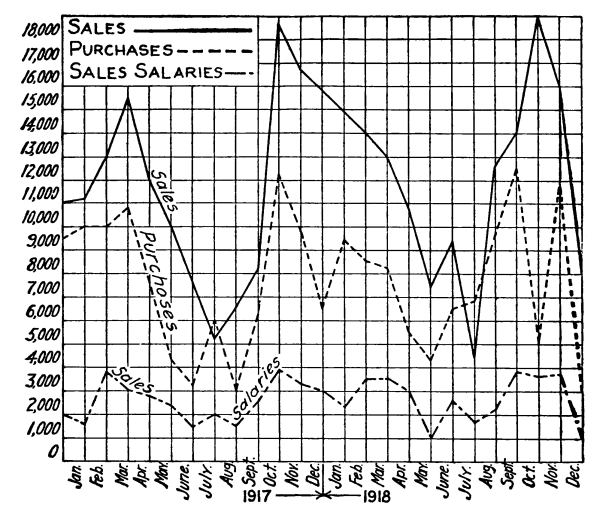

| Chart Showing Comparison of Sales with Cost of Advertising | 585 |

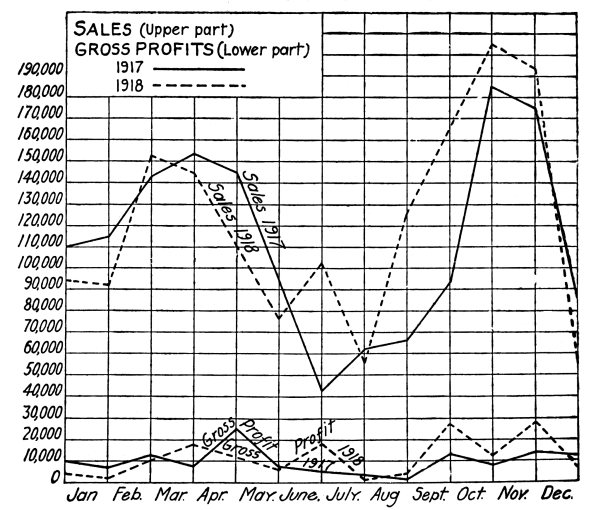

| Chart Showing Comparison of Sales with Gross Profits | 586 |

| Chart Showing Comparison of Sales, Purchases, | |

| and Sales Salaries | 587 |

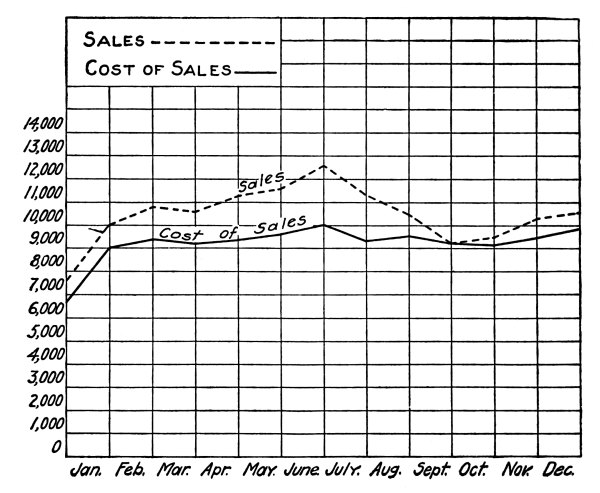

| Chart Showing Comparison of Sales with Cost of Sales | 588 |

| Journal Voucher | 593 |

| Card Index for Journal Vouchers | 594, 595 |

[Pg 1]

Accounting—Theory and Practice

The Corporation

In Volume I, Chapters XLVIII and XLIX, the fundamental characteristics of the corporation were explained and discussed briefly and some of its peculiar accounting features were set forth. Here these matters will be gone into more fully and additional aspects of this type of organization will be treated. In Volume I were explained the advantages and disadvantages of the corporate form, the procedure incident to the formation of a corporation, its charter, officers, working organization and management, the records peculiar to a corporation, the showing of proprietorship, opening the corporation’s books, booking premium and discount on stock, change from partnership to corporation, the distribution of profits, dividends, etc. Only so much of the information already presented will now be repeated as may be necessary to make the treatment here complete.

Classification and Definitions

As instruments for the transaction of business, corporations may be classified in a number of ways. First, all corporations are either public or private. Public corporations are the governmental [Pg 2] organizations set up to transact the collective business of a city, a county, a township, or school district.

Private corporations are divided into two subclasses, stock and non-stock. Under stock corporations are included all those organized to carry on business for a profit. Under non-stock corporations are included all those organized to carry on non-profit-making enterprises, such as libraries, hospitals, religious organizations, eleemosynary undertakings, etc.

Under the head of stock corporations we may have the following subclasses: (a) industrial or manufacturing, (b) commercial or trading, (c) public utility or quasi-public, and (d) financial, i.e., banks, trust companies, insurance companies, etc.

From the standpoint of the sovereignty to which allegiance is due, corporations are either domestic or foreign. A corporation is domestic in the state in which it is organized; foreign in any other state or country. Thus corporations chartered in New York are domestic in New York and foreign in New Jersey and Canada. A foreign corporation may be at a distinct disadvantage with a domestic corporation. To obviate this, one occasionally sees a separate incorporation in every state in which a concern intends to do business. Very infrequently is a domestic corporation subject to more stringent supervision and regulation than a foreign.

From the standpoint of the fact of incorporation, corporations may be classed as (1) de jure and (2) de facto, the former comprising those which have met fully all legal requirements for incorporation, the latter comprising those which have not met fully all legal requirements but are to all intents and purposes corporations in fact.

Method of Ownership

Business corporations are sometimes spoken of as “open” or “close.” An [Pg 3] open corporation is one in which ownership of the stock is not held closely but is being passed about, traded in, or transferred from one owner to a new. A close corporation is one in which the stock is held very closely in order to retain control and keep profits and trade secrets within a small compass of ownership. Thus some corporations are strictly family affairs; others are held by a few families or a small group.

What is known as a corporation “sole,” while little known now, virtually exists in some close corporations, as where one man holds all but two shares of stock. The incorporation of a single individual is not legally possible in this country.

The corporation, because of its peculiar advantages over other forms of business organization, has become the accepted form for most large enterprises. The gathering together of large capital funds, the ease and efficiency of management and control, continuous life, the facility of transfer of ownership, and the limited liability of the stockholders, make the corporate form attractive to the investor and absolutely necessary to the large businesses carried on today. In some states encouragement is given the small business to incorporate; in the State of New York, for example, the minimum limit of capitalization is only $500. In a few other states the old-time fear of the corporate form is still expressed in their general corporation laws in which the minimum limit for corporate capitalization is set as high as $10,000.

Working Organization

The peculiar features of the stock corporation are the method of ownership and working organization. This latter is effected through a board of directors who are responsible directly to the owners at periodic intervals. Within the board are its officers and committees to whom duties are assigned by by-laws, custom, common consent or action of the board. Under these official heads are the rank and file of the [Pg 4] organization—department heads, clerks, employees, etc. It is not necessary to treat here this phase of the organization further.

Different Classes of Stock

The collective capital of a corporation is divided into shares of equal value. Ownership of a share or shares in a corporation is evidenced by formal certificates of stock. Each share carries with it the same privileges, powers, and duties of ownership as every other share of the same class. It represents a pro rata share of the total interest of its class. There may be several different kinds or classes of ownership within the corporation, these classes will have different privileges, and there may be other points of differentiation. The reason for setting up these different classes is almost always to secure additional capital from outside sources by making the investment as attractive as possible. Upon a reorganization, an adjustment of the various interests concerned may require a grading of ownership, a differentiation by classes in order equitably to satisfy the claims of all interested parties. These various classes of stock ownership will be discussed under the following heads:

Common Stock

Common or ordinary stock is that which is evidence of ordinary ownership in the corporation. The share of ownership of the original organizers of the corporation is usually in the common stock. The common stockholder is a sort of remainderman, a residuary legatee. Upon dissolution, after the special claims and privileges of the other [Pg 5] classes of owners have been satisfied, the common stockholders come in for their share. After the satisfaction of the claims of preferred owners, the common stockholders have a right to all that is left, their rights being simply residuary. They are subsequent to those of the other classes and to that extent inferior to them, though they may be more valuable.

Preferred Stock

Preferred stock has some kind of preference over the common. Such stocks differ among themselves, there being no standardized features applicable in every way to all kinds of preferred stocks. The basic purpose of the various preferences is to make the stock attractive from an investment standpoint. Common to all preferred stocks, however, is a preference as to dividends. Whenever profits have been made and have been set aside for dividend purposes, the preferred stockholders receive their dividends ahead of the common stockholders. If only sufficient profits are available to meet the requirements of the preferred stockholders and are appropriated for that purpose, the common owners receive nothing. Stock may be preferred as to assets as well as to profits. By this is meant that in case of dissolution the net assets remaining after payment of all outside claims are applied first to satisfy the interests of the owners of preferred stock and any remainder then goes to the common stockholders.

Cumulative and Non-Cumulative. Preferred stock carries with it a definitely stated minimum rate of dividend. The preferred claim to the profits may be cumulative or non-cumulative. In the one case, if profits are insufficient at any time to meet the preferred dividend requirements or are not appropriated for that purpose, the claims of the preferred owners accumulate from period to period until satisfied in full. This satisfaction must take place before the ordinary owners can have any share in the profits. The rate of [Pg 6] accumulation is the specified minimum and usually interest on unpaid dividends is allowed when the company finally settles these preferred claims. Of course, since dividends can be declared only out of profits, no claim for preferred dividends or any other kind can exist unless sufficient profits have been made. Non-cumulative stock is stock on which the dividend claim does not, if unsatisfied at any time, accumulate from period to period. Preferred stock is cumulative unless otherwise specified.

Dividends on cumulative stock do not have to be paid just because sufficient profits have been made. Declaration of dividends rests entirely with the board of directors who may see fit to appropriate profits to other purposes. A holder of non-cumulative stock may be very unjustly discriminated against in favor of the common stockholder by the withholding of all profits for a number of periods until a large amount has been accumulated. This is then disbursed as a dividend to the common owners after the deduction of as much as may be necessary to satisfy the preferred owner for the current period. On this account a non-cumulative stock is not attractive to investors.

Participating and Non-Participating. Preferred stock may be participating or non-participating. It is said to be participating when the terms under which it is issued provide that it shall share in any dividend in excess of its own specified minimum. Thus, if it is 6% preferred, after the preferred receives its 6% the common stock receives a like dividend, and then the preferred and common may share alike or in any agreed ratio in any further dividends declared in that year. Both participating and non-participating stock is either cumulative or non-cumulative. Preferred stock is non-participating when it is limited to the rate of dividend specified in the terms of its issue.

Redeemable and Convertible. Other features met in some preferred [Pg 7] stocks are redeemability and convertibility. Preferred stock may be issued under a contract to redeem it, after a certain length of time, at a named figure—frequently par plus one year’s dividend. Redemption may be either at the option of the holder or the company. Redemption may be serial, i.e., a certain amount called at stated intervals for redemption. Preferred stock is convertible when under the contract in the terms of its issue it may be converted into some other form of ownership or obligation. Thus, provision may be made that after a certain time has elapsed, preferred shares may be converted into common according to specified rates of conversion; or conversion into bonds of the company is sometimes provided for. Many nice adjustments may become necessary from an accounting viewpoint, when redemption or conversion take place at any ratio other than book values.

Guaranteed Stock

Stock which is issued under a guarantee to pay a specified dividend is said to be guaranteed stock. Inasmuch as dividends can be declared only out of profits, a company cannot guarantee its own stock—or rather a guarantee on the company’s own issue must always be dependent or contingent upon the earning of profits sufficient for that purpose. Stock issued by one company and guaranteed by another may with strict propriety be called guaranteed stock. Thus, a large company may enter into a contract of lease with a smaller concern whereby the compensation shall be, let us say, an 8% dividend guaranteed to all holders of the stock of the smaller concern. Such a guarantee is not contingent but becomes a lien or claim on the guarantor company, regardless of the amount of its earnings.

Founders’ Stock

In England there is issued what is known as “founders’” stock, a stock [Pg 8] preferred as to its share of dividends. Thus, a comparatively small portion of the common stock authorized might be set aside as founders’ or promoters’ shares with the stipulation that these founders’ shares shall receive a dividend out of proportion to the ratio which they bear to the total common stock. The provision might be that these shares shall receive one-half or one-third—or any other specified share—more dividends than shall be given to the common owners. Instead of being preferred stock with specified dividend rate, it is preferred over the rest of the shares of the group from which it was originally set aside but its share of dividends is dependent upon the dividends given the rest of the shares. The par value of the founders’ shares might represent only one-twentieth of the value of the rest of the group, while their share of the dividends would be, say, one-fourth as much as that of the other shares. This preference as to amount of dividends may give founders’ shares a much higher market value than the other shares. Provision is sometimes made for their redemption, as usually there is such a marked difference between their amount ratio and their dividend ratio as compared with the other shares, that dissatisfaction among the owners results. Outstanding founders’ shares may then interfere seriously with the marketability of the other shares.

Debenture Stock

The term debenture stock is applied to a class of liabilities rather than to proprietorship items. In England debentures of various kinds are frequently used. A recent book[1] thus describes them: “In Great Britain the term ‘debenture stock’ is used to designate an unsecured loan issued in irregular amounts. If the amounts were fixed and equal, the issue would be called ‘debenture bonds’ or simply ‘debentures.’ Debenture stock is a debt of [Pg 9] the corporation and does not resemble stock as used in this country.” Debenture stock has not proven popular in this country, although used to some extent in Canada. The Public Service Commission of the State of New York defines debenture stocks as “those issued under contract to pay absolutely thereon at specified intervals a specified return.” These stocks, while usually of limited life like bonds, are sometimes “perpetual and give the holders no right to demand the repayment of their capital, and the company no right to repay it.”[2] When issued as perpetual, they somewhat resemble capital stock, as the term stock is used in this country. Because of the fixed and absolute charge for interest—or dividends as it is sometimes called—which these stocks carry, they are much more of the nature of bonds than of a stock indicating proprietorship. Debenture stocks are therefore to be classed as liabilities.

Stock of No Par Value

A characteristic of most stock is that it bears a specified par value which must be uniform for all the shares within a class. The par value of the different classes may differ, however. In most states no regulation is made of the amount of par value. A par value of $100 is customary for industrial and commercial concerns, and of $1 for mining companies. Between those limits, and even beyond them, one finds stocks of almost any par value.

In the State of New York the issuance of stock of no par value is allowed. Both preferred and common classes may be issued without par value, but if the preferred shares have preference as to assets, the certificates for preferred shares shall state “the amount which the holders of each of such preferred shares shall be entitled to receive on account of principal from the surplus assets of the corporation in preference to the holders of other shares.” With this exception, none of the certificates may express any nominal or par value and this [Pg 10] statement of the amount of preference is regarded as an expression of par value for this purpose. Each share is equal to every other share within its class.

Every certificate of such stock must bear plainly on its face the number of shares which it represents and the number of shares the corporation is authorized to issue. Regardless of the price paid for a share of such stock, all shares issued by the corporation shall be “deemed fully paid and non-assessable and the holder of such shares shall not be liable to the corporation or its creditors in respect thereof.”

To the heedless a named value on a certificate of stock is sometimes misleading as to the real value of the stock. The no-par-value stock overcomes this in that a prospective purchaser is at once put on his guard to find out the worth of the stock. Another advantageous feature is that the questionable practices sometimes indulged in of booking stocks sold at a discount have no place here because the stocks, having no par value, cannot be sold at a discount and the record of their sale will carry therefore the price at which they were sold. Some points in connection with booking this stock will be discussed later.

Watered Stock

So-called watered stock is stock which has a higher nominal value than the true value of the properties for which it has been issued. Thus, if $1,000,000 worth—par value—of stock is issued for the purchase of property which has a marketable value of only $750,000, the stock is said to be watered to the extent of $250,000. The bookkeeping equation requires that an equality be shown between the properties purchased and the par value of the stock, and this is usually done by inflating the value of the properties when they are brought onto the books.

Treasury Stock

Treasury stock, when the term is used properly, is stock which has been [Pg 11] once issued as fully paid and which through purchase or gift comes back into possession of the issuing company. Stock which has never been issued should not be called treasury stock. The distinction between the two lies in the liability (or freedom from it) to further contribution, in case of need to meet the claims of creditors, on the part of stockholders who have bought their shares at less than par value.

In some states the sale of stock at less than par is forbidden. In those states where the practice is allowed, the purchaser of a previously unissued share at less than par is liable to the creditors (if the assets are insufficient to satisfy their claims) for a further contribution equal to the difference between par value and the price paid for the stock. If, though he pays less than par, the stock is issued to him by the corporation as fully paid and non-assessable, he is not liable to the corporation for any further payment to entitle him to all the rights and privileges of a shareholder; but he may be liable in case of need to outside creditors who have a right to expect always that assets of equal value to the stock issued therefor have come into possession of the corporation. As mentioned above, this trouble is obviated in the case of no-par-value stock. However, after stock has once been paid for in full, all future purchasers may hold it without liability for further contribution regardless of the price they pay for it. Because of its freedom from this liability, treasury stock has a readier marketability than unissued stock.

In some enterprises, particularly those of a speculative character where it is extremely difficult if not impossible to place a true valuation on the property to be used or exploited, the practice is very prevalent of issuing the entire authorized capital stock in payment for the properties to be acquired. The stock so issued thus becomes fully paid and its owners liable to no further contribution. To provide working capital, some portion of the stock is usually donated to the [Pg 12] company for resale. This is sometimes called donated stock and is, of course, true treasury stock. In states where a corporation is permitted to buy its own stock, treasury stock may be acquired by purchase. Theoretically, stock which has been issued under a contract providing for redemption becomes treasury stock when redeemed and may be reissued until it has been canceled through charter provision to reduce the capital authorized. (See also pages 15, 16.)

Forfeited Stock

Stock is said to be forfeited through failure to make the agreed purchase payments on it. The laws of the different states vary with regard to the conditions under which stock may be declared forfeited. In some states the instalments paid on the stock—or all but a small amount to cover the cost of handling the transaction, or a specified portion of the amount paid in—must be returned to the purchaser. In others, the entire amount paid in may be declared forfeited. In the State of New York the provision in the law is as follows: “If default shall be made in the payment of any instalment ... the board may declare the stock and all previous payments thereon forfeited for the use of the corporation, after the expiration of sixty days from the service on the defaulting stockholder, personally or by mail directed to him at his last-known post-office address, of a written notice requiring him to make payment within sixty days from the service of the notice at a place specified therein, and stating that, in case of failure to do so, his stock and all previous payments thereon will be forfeited for the use of the corporation. Such stock, if forfeited, may be reissued or subscriptions therefor may be received as in the case of stock not issued or subscribed for. If not sold for its par value or subscribed for within six months after such forfeiture, it shall be canceled and deducted from the amount of the capital stock.” The provisions are very specific and must be carefully followed. The method of accounting is given on page 19. [Pg 13]

Bonus Stocks or Bonds

Bonus stocks or bonds are stocks or bonds given as a bonus upon the purchase of other stocks or bonds. Thus, upon the purchase of a share of preferred stock, one share of common may be given as a bonus.

Accounting for Stocks

Accounting for the original issue of stock has been treated in Volume I. There several different methods of opening the records of the corporation were given and the manner of treating premiums and discount and instalment subscriptions was shown. Here some additional problems peculiar to corporation accounting will be discussed.

Discount on Stock

In the State of New York the stock of a corporation cannot be sold below par. Where sale below par is allowed, the proper booking of the discount requires consideration. The Interstate Commerce Commission requires that discounts or premiums be shown on the books under those titles, i.e., Discount on Capital Stock and Premium on Capital Stock. This method is to be commended as being true to fact and presenting a full and sufficient record of the facts. In the case of other concerns over whose accounting practices there is no regulation, that method is honored more in the breach than in the observance. A prevalent feeling is that the appearance on a balance sheet of such an item as discount on stock is a serious reflection on the standing of the corporation and is to be avoided in any way possible. Discount on stock is not an attractive item on a balance sheet, but there is little justification for such sentiment in those states where the sale of stock at a discount is a perfectly legitimate transaction. The balance sheet ought to represent facts as they are until they change; then the new conditions should be shown. So long as the discount on stock remains a [Pg 14] fact it should be so shown. When the discount has ceased to exist through its absorption against premium on stock or the general surplus, it should no longer be reported because it is then a matter of ancient history with which the present is not concerned.

A favorite method of charging the discount on stock to organization expense is not approved, not because it is a misnomer, for discount may well be looked upon as one of the expenses of organization, but because it is an item of sufficient importance and interest to require separate record. Charging the discount to some asset account, when payment of stock is made by property instead of by cash, is to be severely condemned. Inflation of asset values to cover up such an item cannot be justified.

Premium on Stock

The premium on stock sold above par is best recorded in a premium account which should remain on the books as a part of the permanent capital and not therefore be transferred to surplus and returned as a dividend to the shareholder. It may be legitimately used to cancel any discounts.

In the State of New York a corporation cannot issue its stock “except for money, labor done, or property actually received for the use and lawful purposes of such corporation.” A broad interpretation has been given the word labor so that under the law it may comprise both manual and mental labor and services of almost any kind legitimately received at the time of organization of the corporation or at any subsequent time. Stock may thus be used to pay for organization expense, promoters’ fees, etc.

Property Exchanged for Stock

Where stock is issued for property, no more is supposed to be issued than has a par value equal to a fair market value of the property received therefor. In valuing the property the judgment of the [Pg 15] directors is conclusive, unless fraud can be shown. Any stock issued for property becomes full-paid and the owner is neither subject to further call by the corporation nor liable to contribution for the benefit of creditors. In all statements and reports required by law to be published, stock issued for property purchased must be so reported.

Treasury Stock Donated

When treasury stock comes into the possession of the company by donation, the entries needed to show the transactions are somewhat as indicated below, some variations from the form shown being sometimes met with. Practice varies as to the value at which treasury stock shall be brought onto the books, some concerns booking it at an arbitrary value based on an estimate as to what it will probably bring when sold; others booking it always at par. Practice varies also as to the manner of showing treasury stock on the balance sheet, some listing it among the assets at the value at which it was brought on the books; others treating it as a deduction from authorized capital, a sort of valuation account for the capital stock. These points are discussed in Chapter XXI and will not be treated here except to state a conclusion on which the booking of the transactions depends. Manifestly, if treasury stock is to be treated as a deduction from capital stock, it will have to be brought onto the books at par. Such treatment usually results in an inflated showing of the surplus arising from the donation until that has been adjusted to the values realized from its sale—an adjustment which cannot be completed with accuracy until all treasury stock has been disposed of. If treasury stock is to be shown among the assets on the balance sheet, it is perhaps best booked at an estimated realizable price, a method which will show the donated surplus also at an estimated realizable figure. While authorities differ on these points, the weight of opinion seems to favor booking treasury stock at par and showing it as a valuation account on the balance sheet. [Pg 16]

For the sake of illustration assume that the stockholders donated $100,000 par value of common stock to the corporation and that $50,000 of it is sold at 60 cents on the dollar. The entries to record the transactions would be:

| (1) | Treasury Stock, Common | $100,000.00 | |

| Donated Surplus | $100,000.00 | ||

| (With suitable explanation.) | |||

| (2) | Cash | 30,000.00 | |

| Discount on Treasury Stock, Common | 20,000.00 | ||

| Treasury Stock, Common | 50,000.00 |

Other titles for Donated Surplus are “Donated Working Capital,” “Donation Account,” etc. The account “Discount on Treasury Stock, Common” will ultimately be closed against Donated Surplus, and there is no objection to making the charge for discount directly to Donated Surplus instead of as shown above, although the method shown perhaps makes more easily available the information as to the discounts allowed on sales of various portions of the treasury stock. If it is sold at one price, the charge for the discount should be direct to Donated Surplus. A balance sheet drawn up at an intermediate period, i.e., before Discount on Treasury Stock is closed, should show Donated Surplus at its adjusted figure, viz., book value less discount. After all treasury stock has been sold, the Donated Surplus account, as adjusted, will show the true surplus arising out of the donation transactions. The proper disposition of this—as to whether it should be maintained as a permanent increase in capital, be transferred to general surplus and so be made available for dividends, or be treated as a deduction from plant values on the theory that they have been overstated as originally booked—is discussed in detail in Chapter XXI.

Bonus Stock

Bonus stock is usually treasury stock for the very good reason that, if [Pg 17] it carried a liability for contribution in amount up to its par value, recipients of such stock might not be overly appreciative of the gift. Instead of being an incentive to purchase the securities which it accompanies as a bonus, it might act as a deterrent. Bonus stock is a gift on the part of the corporation and is therefore an expense. While custom favors recording the expense under the title “Bonus”—or even including it with organization expenses—and treating it as a deferred expense for a number of periods, a correct analysis of a bonus stock transaction may dictate other method of record. If the bonus stock is given with an issue of bonds which could by themselves be disposed of only at a discount, the difference between the market value of the bonds alone and their par value should be charged to Bond Discount, and the rest of the loss on the transaction may be charged either to Bonus account or Discount on Treasury Stock. This distinction is important, as will be seen in Chapter XX where the true nature of bond discount is discussed. When data are available for making the separation it should always be done. Thus, if a $1,000 par bond has a market price of $950 but when sold with one share ($100) of treasury stock as a bonus brings $1,000, the record should be:

| (3) | Cash | $1,000.00 | |

| Bond Discount | 50.00 | ||

| Bonus (or Discount on Treasury Stock) | 50.00 | ||

| Bonds Payable | $1,000.00 | ||

| Treasury Stock | 100.00 |

The customary method of showing, as in entry (4) below, is theoretically incorrect, though it may be necessary to use it when the data needed for the other entry, i.e., (3) above, are not available.

| (4) | Cash | $1,000.00 | |

| Bonus | 100.00 | ||

| Bonds Payable | $1,000.00 | ||

| Treasury Stock | 100.00 |

[Pg 18] If a bonus of treasury stock is given with the sale of preferred stock, similar treatment would make possible a showing of the portion which is really discount on stock and the portion, if any, which is true bonus. Inasmuch as discount on stock and bonus are very similar in kind and in manner of treatment on the books, nothing of real value is perhaps gained in making the separation. The ultimate disposition of the Bonus account is, as indicated above, to treat it as a deferred expense, charging it against profits as rapidly as conditions warrant. It is an undesirable item on the balance sheet or ledger and should be expunged as soon as possible.

Treasury Stock Purchased

Treasury stock which is created by purchase by the issuing company requires consideration. If the price paid is less than par, carrying the treasury stock on the books at par requires an offsetting credit account similar to the Donated Surplus account used above when the stock is created by donation. This credit account simply represents a book surplus and should not usually be made the basis for a dividend. This account may be called “Treasury Stock Surplus,” “Contingent Profit on Treasury Stock Bought,” or other title indicating the true nature of the item. When the treasury stock is resold and the discount or premium on it is charged against this surplus or credited to it, as the case may be, the balance of the Treasury Stock Surplus account will then show the realized profit or loss on the completed treasury stock transactions and may be disposed of as indicated above for Donated Surplus.

On the other hand, if the price paid by the company in the purchase of its own stock is more than par, the premium paid must be charged against general surplus because there is usually no other place for the charge unless there is still open on the books a Premium on Stock account arising out of a previous sale of stock at a premium. Purchase [Pg 19] of stock at a premium may represent simply the payment to the owner of the stock of his share in the general surplus of the company, in which case the premium paid must be shown as a reduction of that surplus.

Redemption of Preferred Stock

Handling redemption of a preferred stock issue is exactly the same as handling treasury stock by purchase. If by contract agreement at the time the preferred stock was issued it can only be redeemed at a premium, the premium must be charged, as indicated above, to an open premium account or to general surplus. The effect is similar to the payment of a special or extra dividend at the time redemption is made.

Forfeited Stock

Payments made on stock which is declared forfeited constitute an item of surplus but of a permanent nature, i.e., not a surplus applicable to the declaration of dividends, though there may be no legal inhibition to that use. If the stock is resold any discount on the resale is properly charged against the surplus arising from the forfeiture. By way of illustration, assume that $1,000 worth of stock has been subscribed for and payments amounting to $400 have been made when the stock is forfeited for failure to pay further instalments. The stock is offered again for subscription and is sold for $900 and payment has been received in full. The entries necessary to show the above are: [Pg 20]

| (5) | Subscribers | $1,000.00 | |

| Capital Stock Subscriptions | $1,000.00 | ||

| (6) | Cash | 400.00 | |

| Subscribers | 400.00 | ||

| (7) | Subscribers | 400.00 | |

| Surplus from Forfeited Stock. | 400.00 | ||

| To transfer the forfeited payments to Surplus. |

|||

| (8) | Capital Stock Subscriptions | $1,000.00 | |

| Subscribers | $1,000.00 | ||

| To reverse. | |||

| (9) | Subscribers | 900.00 | |

| Surplus from Forfeited Stock | 100.00 | ||

| Capital Stock Subscriptions | 1,000.00 | ||

| (10) | Cash | 900.00 | |

| Subscribers | 900.00 | ||

| (11) | Capital Stock Subscriptions | 1,000.00 | |

| Capital Stock | 1,000.00 |

Stock of No Par Value

Booking capital stock of no par value presents no new principles. Inasmuch as the stock has no fixed par value, its sale is recorded for what it fetches. There can be neither discount nor premium. Payment of the subscription may be made, just as in any other case, by means of cash, property, or services, and the same care must be exercised in placing proper valuations on the property taken over. Here there is not the danger of inflating property values to show them equivalent to the par value of the stock issued therefor. Rather, subscription for the stock is made at the figure of the fair value of the property to be turned over in payment of the subscription. In the case of no-par-value stock even greater care must be exercised to see that the contributed capital shall never be encroached upon in the declaration of dividends, and careful supervision is somewhat more difficult because the number of shares issued bears no relation to the amount of the capital stock.

Distinctive Records

The accounting and other records peculiar to a corporation are explained in Volume I, Chapter XLVIII. These records are the subscription book and subscription ledger or instalment book, the stock certificate book and stock ledger, the stock transfer book, the minute book, sometimes a dividend book, in large companies a register of [Pg 21] transfers (which classifies the information as to transfers given in the stock transfer book, and so may serve as a convenient posting medium for the stock ledger), and a stock register (a record kept by the officially appointed registrar of the corporation, whose duty it is to see that there are no irregularities in the issue of stock and that there is no overissue). The stock register should show the amount of stock authorized and the amount issued at any given time, the balance being the stock not yet issued. A form for the stock transfer book and several forms for stock ledgers as prescribed by the Comptroller of the State of New York are shown below.[3] The two latter forms of the stock ledger are applicable only to the State of New York.

Ledger Folio 27

Alliance Automobile Company

For value Received, I hereby sell, assign and transfer unto John H. Lansing, of Newark, New Jersey, Seventy-six Shares of the Capital Stock of the above-mentioned Company, now standing in my name on the Company books and represented by surrendered Certificates Nos. 32, 37, and 44.

Witness my hand and seal this 28th day of September, 1918.

New Certificate No. 224

Issued to John H. Lansing

Ledger Folio 84

Stock Transfer Book

[Pg 22]

| John H. Kircher, 230 Broadway, New York | ||||

|---|---|---|---|---|

| Date of Transfer |

To Whom Shares are Transferred |

Certificate Numbers |

Number of Shares |

|

| Surrendered | Reissued | |||

| 1917 | ||||

| March 13 | W. K. Howard | 15 | 70 | 10 |

| July 15 | Robert Moyer | 70 | 145 | 40 |

| July 31 | Harold McKain | 145 | 40 | |

| December 3 | James McNeil | 85 | 175 | 20 |

| December 16 | James Archer | {175} | 231 | 105 |

| {165} | ||||

| December 31 | Balance | 180 | ||

| 395 | ||||

| Date of Transfer |

From Whom Shares were Transferred |

Amount Paid on Shares |

Certificate Numbers |

Number of Shares |

| 1917 | ||||

| January 10 | Original Issue | Full-Paid | 15 | 90 |

| March 25 | George Holmes | ” | 85 | 75 |

| August 1 | Harvey Cornell | ” | 150 | 35 |

| August 15 | Howard Gaines | ” | 160 | 50 |

| ” | ||||

| September 2 | John Woodwell | ” | 165 | 100 |

| October 5 | Henry Simpson | ” | 42 | 45 |

| 395 | ||||

| 1918 | ||||

| January 3 | 180 | |||

Stock Book or Stock Ledger

[Pg 23]

Stock Book to be Kept by Brokers