THE BUSY RETAIL STORE OF THE L. E. WATERMAN COMPANY

At the "Pen Corner," 173 Broadway, New York City

Cyclopedia

of

Commerce, Accountancy,

Business Administration

Volume 4

A General Reference Work on

ACCOUNTING, AUDITING, BOOKKEEPING, COMMERCIAL LAW, BUSINESS

MANAGEMENT, ADMINISTRATIVE AND INDUSTRIAL ORGANIZATION,

BANKING, ADVERTISING, SELLING, OFFICE AND FACTORY

RECORDS, COST KEEPING, SYSTEMATIZING, ETC.

Prepared by a Corps of

AUDITORS, ACCOUNTANTS, ATTORNEYS, AND SPECIALISTS IN BUSINESS METHODS AND MANAGEMENT

Illustrated with Over Two Thousand Engravings

TEN VOLUMES

CHICAGO

AMERICAN TECHNICAL SOCIETY

1910

Copyright, 1909

BY

AMERICAN SCHOOL OF CORRESPONDENCE

Copyright, 1909

BY

AMERICAN TECHNICAL SOCIETY

Entered at Stationers' Hall, London

All Rights Reserved

Authors and Collaborators

JAMES BRAY GRIFFITH, Managing Editor

Head, Dept. of Commerce, Accountancy, and Business Administration, American School of Correspondence.

ROBERT H. MONTGOMERY

Of the Firm of Lybrand, Ross Bros. & Montgomery, Certified Public Accountants.

Editor of the American Edition of Dicksee's Auditing.

Formerly Lecturer on Auditing at the Evening School of Accounts and Finance of the University of Pennsylvania, and the School of Commerce, Accounts, and Finance of the New York University.

ARTHUR LOWES DICKINSON, F. C. A., C. P. A.

Of the Firms of Jones, Caesar, Dickinson, Wilmot & Company, Certified Public Accountants, and Price, Waterhouse & Company, Chartered Accountants.

WILLIAM M. LYBRAND, C. P. A.

Of the Firm of Lybrand, Ross Bros. & Montgomery, Certified Public Accountants.

F. H. MACPHERSON, C. A., C. P. A.

Of the Firm of F. H. Macpherson & Co., Certified Public Accountants.

CHAS. A. SWEETLAND

Consulting Public Accountant.

Author of "Loose-Leaf Bookkeeping," and "Anti-Confusion Business Methods."

E. C. LANDIS

Of the System Department, Burroughs Adding Machine Company.

HARRIS C. TROW, S. B.

Editor-in-Chief, Textbook Department, American School of Correspondence.

CECIL B. SMEETON, F. I. A.

Public Accountant and Auditor.

President, Incorporated Accountants' Society of Illinois.

Fellow, Institute of Accounts, New York.

JOHN A. CHAMBERLAIN, A. B., LL. B.

Of the Cleveland Bar.

Lecturer on Suretyship, Western Reserve Law School.

Author of "Principles of Business Law."

HUGH WRIGHT

Auditor, Westlake Construction Company.

GLENN M. HOBBS, Ph. D.

Secretary, American School of Correspondence.

JESSIE M. SHEPHERD, A. B.

Associate Editor, Textbook Department, American School of Correspondence.

GEORGE C. RUSSELL

Systematizer.

Formerly Manager, System Department, Elliott-Fisher Company.

OSCAR E. PERRIGO, M. E.

Specialist in Industrial Organization.

Author of "Machine-Shop Economics and Systems," etc.

DARWIN S. HATCH, B. S.

Assistant Editor, Textbook Department, American School of Correspondence.

CHAS. E. HATHAWAY

Cost Expert.

Chief Accountant, Fore River Shipbuilding Co.

CHAS. WILBUR LEIGH, B. S.

Associate Professor of Mathematics, Armour Institute of Technology.

L. W. LEWIS

Advertising Manager, The McCaskey Register Co.

MARTIN W. RUSSELL

[4]Registrar and Treasurer, American School of Correspondence.

HALBERT P. GILLETTE, C. E.

Managing Editor, Engineering-Contracting.

Author of "Handbook of Cost Data for Contractors and Engineers."

R. T. MILLER, JR., A. M., LL. B.

President, American School of Correspondence.

WILLIAM SCHUTTE

Manager of Advertising, National Cash Register Co.

E. ST. ELMO LEWIS

Advertising Manager, Burroughs Adding Machine Company.

Author of "The Credit Man and His Work" and "Financial Advertising."

RICHARD T. DANA

Consulting Engineer.

Chief Engineer, Construction Service Co.

P. H. BOGARDUS

Publicity Manager, American School of Correspondence.

WILLIAM G. NICHOLS

General Manufacturing Agent for the China Mfg. Co., The Webster Mfg. Co., and the Pembroke Mills.

Author of "Cost Finding" and "Cotton Mills."

C. H. HUNTER

Advertising Manager, Elliott-Fisher Co.

FRANK C. MORSE

Filing Expert.

Secretary, Browne-Morse Co.

H. E. K'BERG

Expert on Loose-Leaf Systems.

Formerly Manager, Business Systems Department, Burroughs Adding Machine Co.

EDWARD B. WAITE

Head, Instruction Department, American School of Correspondence.

Authorities Consulted

The editors have freely consulted the standard technical and business literature of America and Europe in the preparation of these volumes. They desire to express their indebtedness, particularly, to the following eminent authorities, whose well-known treatises should be in the library of everyone interested in modern business methods.

Grateful acknowledgment is made also of the valuable service rendered by the many manufacturers and specialists in office and factory methods, whose coöperation has made it possible to include in these volumes suitable illustrations of the latest equipment for office use; as well as those financial, mercantile, and manufacturing concerns who have supplied illustrations of offices, factories, shops, and buildings, typical of the commercial and industrial life of America.

JOSEPH HARDCASTLE, C. P. A.

Formerly Professor of Principles and Practice of Accounts, School of Commerce, Accounts, and Finance, New York University.

Author of "Accounts of Executors and Testamentary Trustees."

HORACE LUCIAN ARNOLD

Specialist in Factory Organization and Accounting.

Author of "The Complete Cost Keeper," and "Factory Manager and Accountant."

JOHN F. J. MULHALL, P. A.

Specialist in Corporation Accounts.

Author of "Quasi Public Corporation Accounting and Management."

SHERWIN CODY

Advertising and Sales Specialist.

Author of "How to Do Business by Letter," and "Art of Writing and Speaking the English Language."

FREDERICK TIPSON, C. P. A.

Author of "Theory of Accounts."

CHARLES BUXTON GOING

Managing Editor of The Engineering Magazine.

Associate in Mechanical Engineering, Columbia University.

Corresponding Member, Canadian Mining Institute.

F. E. WEBNER

Public Accountant.

Specialist in Factory Accounting.

[6]Contributor to The Engineering Press.

AMOS K. FISKE

Associate Editor of the New York Journal of Commerce.

Author of "The Modern Bank."

JOSEPH FRENCH JOHNSON

Dean of the New York University School of Commerce, Accounts, and Finance.

Editor, The Journal of Accountancy.

Author of "Money, Exchange, and Banking."

M. U. OVERLAND

Of the New York Bar.

Author of "Classified Corporation Laws of All the States."

THOMAS CONYNGTON

Of the New York Bar.

Author of "Corporate Management," "Corporate Organization," "The Modern Corporation," and "Partnership Relations."

THEOPHILUS PARSONS, LL. D.

Author of "The Laws of Business."

E. ST. ELMO LEWIS

Advertising Manager, Burroughs Adding Machine Company.

Formerly Manager of Publicity, National Cash Register Co.

Author of "The Credit Man and His Work," and "Financial Advertising."

T. E. YOUNG, B. A., F. R. A. S.

Ex-President of the Institute of Actuaries.

Member of the Actuary Society of America.

Author of "Insurance."

LAWRENCE R. DICKSEE, F. C. A.

Professor of Accounting at the University of Birmingham.

Author of "Advanced Accounting," "Auditing," "Bookkeeping for Company Secretary," etc.

FRANCIS W. PIXLEY

Author of "Auditors, Their Duties and Responsibilities," and "Accountancy."

CHARLES U. CARPENTER

General Manager, The Herring-Hall-Marvin Safe Co.

Formerly General Manager, National Cash Register Co.

[7]Author of "Profit Making Management."

C. E. KNOEPPEL

Specialist in Cost Analysis and Factory Betterment.

Author of "Systematic Foundry Operation and Foundry Costing," "Maximum Production through Organization and Supervision," and other papers.

HARRINGTON EMERSON, M. A.

Consulting Engineer.

Director of Organization and Betterment Work on the Santa Fe System.

Originator of the Emerson Efficiency System.

Author of "Efficiency as a Basis for Operation and Wages."

ELMER H. BEACH

Specialist in Accounting Methods.

Editor, Beach's Magazine of Business.

Founder of The Bookkeeper.

Editor of The American Business and Accounting Encyclopedia.

J. J. RAHILL, C. P. A.

Member, California Society of Public Accountants.

Author of "Corporation Accounting and Corporation Law."

FRANK BROOKER, C. P. A.

Ex-New York State Examiner of Certified Public Accountants.

Ex-President, American Association of Public Accountants.

Author of "American Accountants' Manual."

CLINTON E. WOODS, M. E.

Specialist in Industrial Organization.

Formerly Comptroller, Sears, Roebuck & Co.

Author of "Organizing a Factory," and "Woods' Reports."

CHARLES E. SPRAGUE, C. P. A.

President of the Union Dime Savings Bank, New York.

Author of "The Accountancy of Investment," "Extended Bond Tables," and "Problems and Studies in the Accountancy of Investment."

CHARLES WALDO HASKINS, C. P. A., L. H. M.

Author of "Business Education and Accountancy."

JOHN J. CRAWFORD

Author of "Bank Directors, Their Powers, Duties, and Liabilities."

DR. F. A. CLEVELAND

Of the Wharton School of Finance, University of Pennsylvania.

Author of "Funds and Their Uses."

CHICAGO SALES AND DISPLAY ROOMS OF THE NEW HAVEN CLOCK COMPANY

Foreword

With the unprecedented increase in our commercial activities has come a demand for better business methods. Methods which were adequate for the business of a less active commercial era, have given way to systems and labor-saving ideas in keeping with the financial and industrial progress of the world.

Out of this progress has risen a new literature—the literature of business. But with the rapid advancement in the science of business, its literature can scarcely be said to have kept pace, at least, not to the same extent as in other sciences and professions. Much excellent material dealing with special phases of business activity has been prepared, but this is so scattered that the student desiring to acquire a comprehensive business library has found himself confronted by serious difficulties. He has been obliged, to a great extent, to make his selections blindly, resulting in many duplications of material without securing needed information on important phases of the subject.

In the belief that a demand exists for a library which shall embrace the best practice in all branches of business—from buying to selling, from simple bookkeeping to the administration of the financial affairs of a great corporation—these volumes have been prepared. Prepared primarily for[9] use as instruction books for the American School of Correspondence, the material from which the Cyclopedia has been compiled embraces the latest ideas with explanations of the most approved methods of modern business.

Editors and writers have been selected because of their familiarity with, and experience in handling various subjects pertaining to Commerce, Accountancy, and Business Administration. Writers with practical business experience have received preference over those with theoretical training; practicability has been considered of greater importance than literary excellence.

In addition to covering the entire general field of business, this Cyclopedia contains much specialized information not heretofore published in any form. This specialization is particularly apparent in those sections which treat of accounting and methods of management for Department Stores, Contractors, Publishers and Printers, Insurance, and Real Estate. The value of this information will be recognized by every student of business.

The principal value which is claimed for this Cyclopedia is as a reference work, but, comprising as it does the material used by the School in its correspondence courses, it is offered with the confident expectation that it will prove of great value to the trained man who desires to become conversant with phases of business practice with which he is unfamiliar, and to those holding advanced clerical and managerial positions.

In conclusion, grateful acknowledgment is made to authors and collaborators, to whose hearty cooperation the excellence of this work is due.

Table of Contents

(For professional standing of authors, see list of Authors and Collaborators at front of volume.)

VOLUME IV

| Theory of Accounts | By James B. Griffith | Page 11 |

| Dictionary of Commercial Terms—Commercial Abbreviations—Objects of Bookkeeping—Methods—Single Entry—Double Entry—Advantages of Double Entry —Classes of Account Books—Recording Transactions—Promissory Notes—Bank Deposits—Sample Transactions—Classes of Accounts—Classes of Assets—Revenue Accounts—Rules for Journalizing—Rules for Posting—Trial Balance—Sample Ledger Accounts—Treatment of Cash Discounts—Profit and Loss—Merchandise Inventory Accounts—Balance Sheet—Journalizing Notes—Journalizing Drafts | ||

| Single Proprietorship and Partnership Accounts | By James B. Griffith | Page 119 |

| Retail Business—Proprietors' Accounts—Inventory—Retail Coal Books— Uncollectible Accounts—Sales Tickets—Departmental Records—Partnership Agreements—Kinds of Partners—Participation in Profits—Interest on Investments—Capital and Personal Accounts—Opening and Closing Partnership Books—Model Set of Books | ||

| Corporation and Manufacturing Accounts | By James B. Griffith | Page 195 |

| Classification of Corporations—Joint Stock Company—Creation of Corporation —Stockholders—Stock Certificates—Capitalization—Capital and Capital Stock —Stock Subscriptions—Management of Corporations—Powers of Directors and Officers—Dividends—Closing Transfer Books—Sale of Stock Below Par—Corporation Bookkeeping—Books Required—Opening Entries—Changing Books from Partnership to Corporation—Stock Donated to Employes—Reserves—Computing Sinking Funds—Premium and Interest on Bonds—Manufacturing and Cost Accounts—Factory Assets—Factory Expenses—Balance Ledger | ||

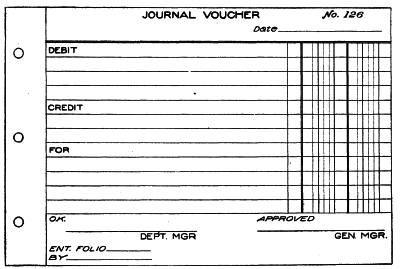

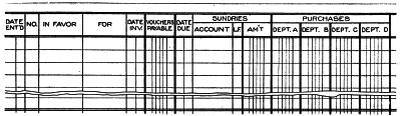

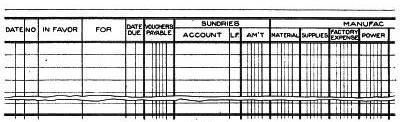

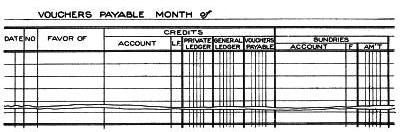

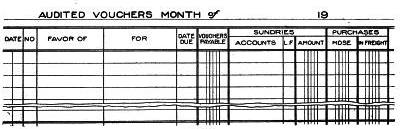

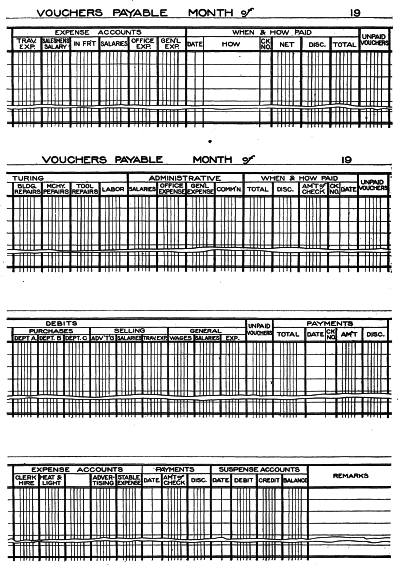

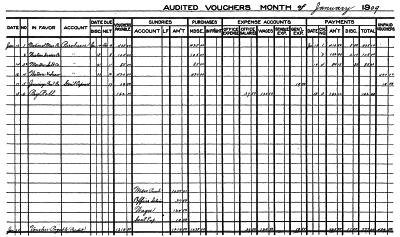

| The Voucher System of Accounting | By James B. Griffith | Page 273 |

| Use of Vouchers—Voucher Checks—Journal Vouchers—Voucher Register— Operation of System—Auditing Invoices—Executing Vouchers—Paying, Filing, and Indexing Vouchers—Voucher File—Demonstration of System—Voucher Accounting—Unit System—Combined Purchase Ledger and Invoice File—Private Ledger—Private Journal—General Ledger—Manufacturing Accounts—Charting Accounts—Chart of Trading Business—Chart of Manufacturing Accounts—Examples of Charts—Explanation of Charts | ||

| Review Questions | Page 325 | |

| Index | Page 345 | |

THE ACCOUNTING DEPARTMENT IN THE OFFICES OF THE GREEN FUEL ECONOMIZER COMPANY, MATTEAWAN, N. Y.

THEORY OF ACCOUNTS

PART I

Like every other special branch of study, the Theory and Practice of Accounts has its own special vocabulary of technical terms. In all literature of accounting and business methods in general, these terms are frequently employed; and the student will find it not only advantageous, but in fact absolutely necessary, to familiarize himself thoroughly with their use.

The commercial terms and definitions in the following list are the ones most commonly used in business. Great care has been exercised in preparing a list that is practical and in making the definitions clear.

DICTIONARY OF COMMERCIAL TERMS

Acceptance—When a draft or bill of exchange is presented to the payer, he writes across the face "Accepted" or "Accepted for payment at ..." and signs his name. It is then termed an acceptance.

Accommodation Note—A note given without consideration of value received; usually done to enable the payee to raise money.

Account—

(a) A statement of debits and credits.

(b) A record of transactions with a particular person or persons, or with respect to a particular object.

Account Books—Books in which records of business transactions or accounts are kept.

Account Current—An account of transactions during the present month, week, or other current period. An open account.

Account Sales—A statement in detail covering sales, expenses, and net proceeds made by a commission merchant to one who has consigned goods to him.

Accrued; Accrued Interest—

(a) Accumulated interest not payable until a specified date.

(b) Accumulated rent.

Specimen Account

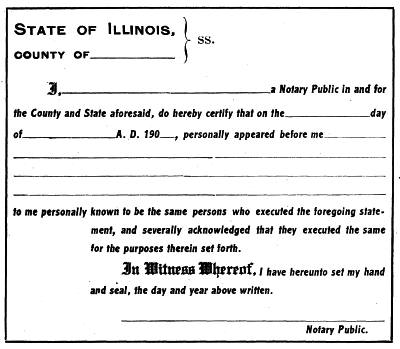

Acknowledgment—A certificate to the genuineness of a document signed and sworn to before an authorized official, as a Notary Public.

Administrator—One appointed by the court to settle an estate.

Ad Valorem—According to value. A term used to indicate that duties are payable on the value rather than on the weight or quantity of articles.

Adventure—As used in business, this term signifies a venture or speculation.

Account Sales

Advice—Information with reference to a business transaction; notice of shipment; notice of draft. Transmitted by letter or telegram.

Affidavit—A statement or declaration made under oath, before an authorized official.

Agent—One authorized to act or transact business for another.

Agreement—A mutual contract entered into by two or more persons.

Acknowledgment

Allowance—An abatement; a credit for inferior goods, error in quantity, etc.

Annual Statement—A yearly summary of the transactions of a business.

Annuity—An amount payable to or received from another each year for a term of years or for life.

Antedate—To date a document or paper ahead of the actual time of its execution.

Appraise—To place a value on goods or property. An estimate made for the purpose of assessing duties or taxes.

Appreciation—An increase in value. Real estate may increase in value on account of the demand for property in the immediate vicinity.

Approbation or Approval Sales. Goods delivered to customers with the understanding that if not found satisfactory they are to be returned within a definite period and without payment.

Articles—A collection of merchandise; parts of a written agreement, as "Articles of Association."

Arbitrate—To determine or settle disputes between two or more parties, as settlement of differences between employer and employees.

Assets—All of the property, goods, possessions of value of a person or persons in business.

Assign—To transfer or convey to another for the benefit of creditors.

Assignee—The person to whom the property or business is transferred. Usually acts as a trustee of the creditors.

Assignment—The debtor's transfer or conveyance of his property to a trustee.

Assignor—The debtor who makes an assignment, or transfers property for the benefit of creditors.

Association—A body organized for a common object.

Attachment—A legal seizure of goods to satisfy a debt or claim.

Auxiliary—Books of record other than books of original entry or principal books of account. Books used for purposes of distribution or the gathering of statistics are "auxiliary" books.

Audit—To verify the accuracy of accounts by examining or checking records pertaining thereto.

Average—As applied to accounts, the mean time which bills of different dates have to run, or an average due date for several accounts. Determining the due date is sometimes referred to as averaging accounts.

Balance—The difference between the debit and credit sides of an account. To close an account by entering the amount on the lesser side necessary to make the two sides balance.

Balance Sheet—A statement or summary in condensed form made for the purpose of showing the standing or condition of a business.

Balance of Trade—The balance or difference in value between the imports and exports of a country.

Bale—The form in which certain commodities are marketed. A bale of cotton, bale of hay, etc.

Bank Balance—The net amount to the credit of a depositor at the bank.

Bank Note—A note issued by a bank, payable on demand, which passes for money.

Bank Draft—An order drawn by one bank on another for the purpose of paying money.

Bank Pass-Book—A small book furnished to a depositor by his bank, in which are entered the amounts of deposits and sometimes the checks or withdrawals.

Bankrupt—A person, firm, or corporation whose liabilities exceed their assets; who are unable to meet their obligations.

Bill—A statement or record of goods bought or sold, or of services rendered.

Bill

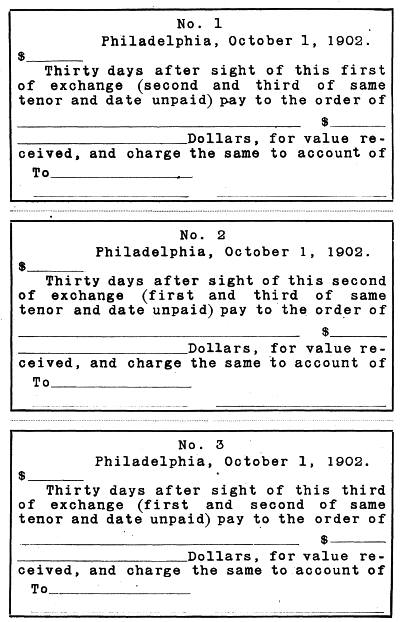

Bill of Exchange—An order on a given person or bank to pay a specified amount to the person and at the time named in the bill. The term is more commonly used to apply to orders on another country, being made in triplicate.

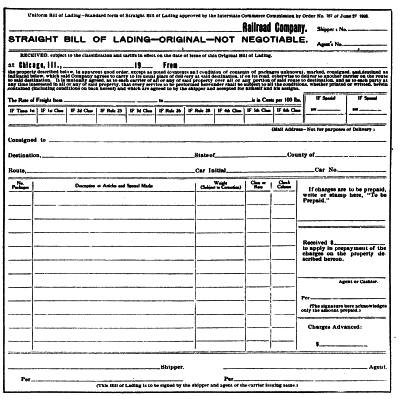

Bill of Lading—A receipt issued by the representative of a common carrier, for goods accepted for transportation to a specified point and at a given rate. It is a contract, and, when transferred to a third party, becomes an absolute title to the goods.

Bill of Lading

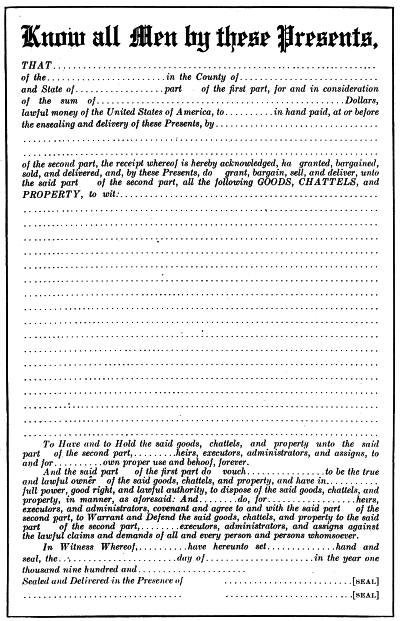

Bill of Sale—A written document executed by the seller, transferring title to personal property.

Bill Head—The blank or form on which a bill is made. For illustration, see Bill.

Bill of Exchange

Bills Payable—Promissory notes and acceptances which we are to pay.

Bills Receivable—Promissory notes and acceptances which are to be paid to us.

Blanks—Papers or books ruled or printed in suitable form for business records.

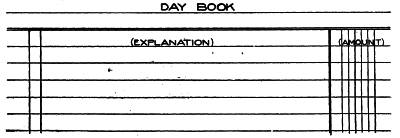

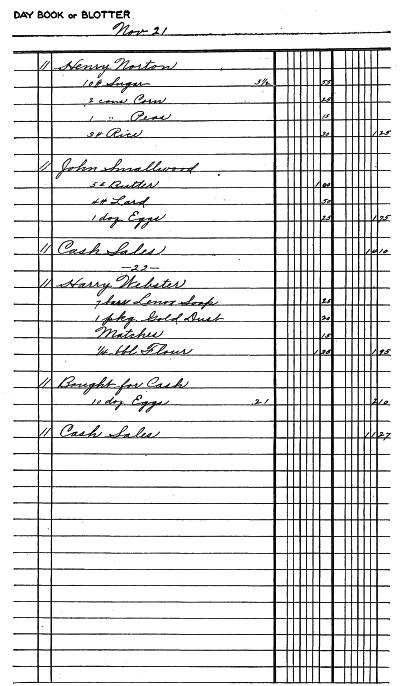

Blotter—A book in which are entered memoranda of transactions which are later copied into other books. Also known as a day book.

Bond—A written agreement binding a person to do or not to do certain things specified therein. A negotiable instrument secured by mortgage or other security, binding the maker to pay certain sums on specific dates.

Bonded Goods—Goods stored in a government warehouse, or in bonded cars, bonds having been given by the owner for the payment of import duties or internal revenue taxes when removed.

Bonus—An amount paid in excess of the sum originally agreed upon. A premium or gift—for example, a sum paid to a salesman as extra compensation for making a certain number of sales.

Book Account—A charge or evidence of indebtedness on the books of account not secured by note or other written promise.

Brand—A class of goods. A symbol or name used to designate a specific article. A trade mark.

Broker—One who acts as agent or middleman between buyer and seller.

Brokerage—The commissions or fees paid the broker for his services. Also a term used to designate his business.

Bullion—Uncoined gold or silver.

Call Loans—Loans made payable on demand or when called for.

Cancel—To render null and void; to annul.

Capital—Property or money invested in a business.

Capital Stock—A term used to indicate the subscriptions of all stockholders to the capital of a corporation.

Cartage—The charges made for hauling goods by wagon, or otherwise than by freight or express.

Cash Sales—Sales for which immediate payment is received in contradistinction to sales of goods on credit.

Bill of Sale

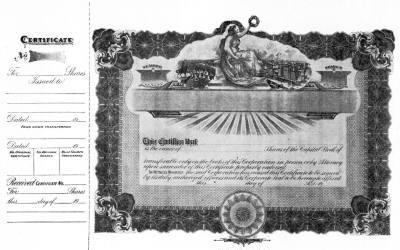

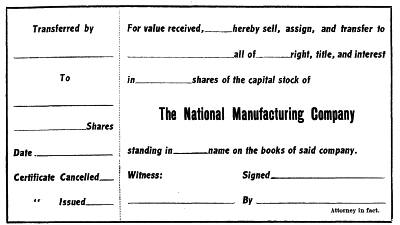

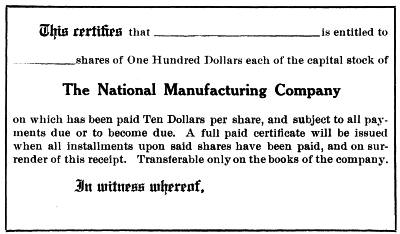

Certificate of Stock—A written statement or declaration of the purchase of a specified number of shares of the capital stock of a corporation. An evidence of ownership.

Certified Check—A check, the payment of which is guaranteed by the bank on which it is drawn.

Charges—The expense involved in handling goods or in performing a specific act—as, for example, charges for storage, freight charges, etc. Also a synonym for debits.

Chart—A classified exhibit of the components of a business organization, showing the authority and responsibilities of the members. Grouping of the accounts of a business with respect to their relation to one another.

Charter—To hire a car, ship, or other instrument of transportation. A document defining the rights and duties of a corporation.

Check—An order on a bank to pay to a certain person, or to the order of such person, a specified sum, which sum is to be charged to the account of the drawer of the check.

Clearing House—An exchange established by banks in cities, for their convenience in making daily settlements. The checks and drafts on the different banks are exchanged without the formality of presenting them personally at each bank. A balance is found, and this amount only is paid in cash.

Closing an Account—Making an entry that will balance the account.

Collateral—Pledges of security—as stocks, bonds, etc.—to protect an obligation or insure the payment of a loan.

Commission—A percentage or share of the proceeds allowed for the sale of merchandise—as the pay of a commission merchant for selling a car of flour.

Commission Merchant—One who sells goods on commission. Similar to a broker.

Commercial Paper—Negotiable paper used in business.

Common Law—Law based upon the precedent of usage, though not contained in the statutes.

Company—A corporation; also used to designate partners whose names are not known.

Compromise—To settle an account for less than the amount claimed. To agree upon a settlement.

Certificate of Stock

Consideration—The price or money paid or to be paid which induces the entering into a contract by two or more persons.

Consignee—The party to whom goods are shipped. A person to whom goods are sent to be sold on commission is a consignee. The goods so sent are known as a consignment, and the sender is the consignor.

Consul—An agent of the Government, residing in a foreign part, who guards the interests of his own Government.

Contra—On the opposite side—as a contra account.

Contract—A written agreement between two or more persons to perform or not to perform some specified act or acts.

Contingent Assets and Liabilities—Resources or liabilities whose value depends upon certain conditions.

Contingent Fund—A sum put aside to provide for an anticipated obligation; a reserve fund.

Conveyance—A term used to describe certain forms of legal documents transferring from one person to another, title to property or collateral.

Copyright—A right granted to an author or publisher to control the publication of any writing, or the reproduction of a photograph, painting, etc.

Counterfeit—A spurious coin, or bank or treasury note.

Coupon—A certificate detached from a bond, which entitles the holder to the payment of interest.

Coupon Bond—Bonds to which are attached coupons calling for the payment of interest. The coupons, when detached, become negotiable paper.

Credentials—Letters or testimonials conveying authority.

Creditor—One whom we owe; one who gives credit.

Currency—The coin or paper money constituting the circulating medium of a country.

Debenture—A certified evidence of debt. See Bond.

Debit—To charge; to record an amount due.

Deed—A written document or contract transferring title to real estate.

Defalcation—The appropriating to one's own use, of money intrusted to him by another; embezzlement.

Deferred Bonds—Bonds which are to be paid when some condition is fulfilled in the future.

Delivery Receipt—An acknowledgment of the delivery of goods. Largely used by merchants in the delivery of goods to customers.

Demand Note—A promissory note or acceptance payable on presentation or on demand.

Deposit—The money placed in custody of the bank, subject to order.

Depreciation—A reduction in the value of property. In a manufacturing plant, buildings and machinery depreciate in value through wear and tear; a residence property may depreciate owing to the nature of a nearby building.

Delivery Receipt

Discount—An allowance or abatement made for the payment of a bill within a specified period. The interest paid in advance on money borrowed from a bank.

Dishonor—Refusal to accept a draft, or failure to pay a written obligation when due.

Demand Note

Dividend—The profits which are distributed among the stockholders of a corporation.

Draft—A written order for the payment of money—usually made through some bank.

Drawer—The person by whom the draft is made; the one who requested the payment of money by the drawee.

Drayage—Synonymous with cartage.

Due Bill—A written acknowledgment of an amount due; of the same effect as a demand note.

Dunning—Soliciting or urgently pressing the payment of a debt.

Duplicate—A copy of a paper or document; the act of making a copy.

Duty—The tax paid on imported goods.

Doubtful—Of questionable value. We refer to an account as "doubtful" when we question the likelihood of its payment.

Draft

Earnest—An advance payment, applying on the purchase price, made to bind an oral bargain.

Embezzlement—See Defalcation.

Exchange—The charge made by a bank for the collection of drafts or checks.

Exports—Commodities sent to another country.

Extend—To set a later date for payment; to add several items and carry the totals to the proper column.

Face Value—The amount for which a commercial paper is drawn.

Facsimile—An exact duplicate or exact copy.

Financial Statement—A term used in the same sense as balance sheet or annual statement.

Fiscal—A financial or business year, in contradistinction to a calendar year. The fiscal year of a business may commence and end on any date—usually on the date on which it was started.

Fixed Assets—Permanent assets acquired by a firm or corporation to enable them to conduct a business. Includes real estate, building, machinery, horses and wagons, etc.

Fixed Charges—Those charges in connection with the operation of a business which occur at regular intervals, such as rent, taxes, etc.

Fixtures—A fixed asset represented by that part of the furniture not readily removable, such as gas and electric light fixtures.

Folio—A column provided in account books, in which to enter the page numbers of other books from or to which records are transferred.

Footing—The sum or amount of a column of figures.

Foreign Exchange—Drafts on foreign cities.

Freight—The charges paid for the transportation of goods.

Gain—The increase in value of assets or profit resulting from a transaction or transactions.

Gauging—Measuring the liquid contents of casks or barrels.

Going Business—A term used to designate a business in actual operation. Goodwill or the reputation of a business has a value so long as the business is in operation, or keeps going. When a business is discontinued, only the physical assets or actual properties owned by the business are of value.

Good Will—The monetary value of the reputation of a business over and above its visible assets; the value of a business name.

Gross—The entire amount in contradistinction to the net amount—as gross weight or gross profit.

Guarantee or Guaranty—Surety for the maintenance of quality or the performance of contracts.

Honor—To pay a promissory note when due; to accept or pay a draft.

Hypothecate—To deposit as collateral security for a loan.

Import—To bring goods into the country.

Income—The receipts of a business.

Income Bonds—Bonds on which the payment of interest is contingent on profits earned. If the interest is passed on account of lack of funds, the holder of the bond has no claim.

Indemnity—Security against a form of loss which has occurred or may occur—as fire insurance, against loss by fire.

Indorse—To guarantee the payment of commercial paper by writing one's name on the back.

Indorsee—The person to whom a paper is indorsed.

Lease

Indorser—The person who guarantees payment; the one who indorses.

Infringe; Infringement—To trespass upon another's rights—as infringement of a patent or copyright.

Installment—An account or note the payment of which is to be made in several parts, at stated intervals.

Insolvent—Unable to pay one's obligations.

Instant—Principally used in correspondence to indicate the present month.

Insurance Policy—A contract between an insurance company and the insured.

Interest—The sum or premium paid for the use of money; one's share in a business or a particular property.

Inventory—An itemized schedule of the property or goods belonging to a business.

Investment—Money paid for goods or property to be held; not for speculation.

Invoice—A list of goods bought or sold. See Bill.

Jobber—One who buys from manufacturers and sells to retailers; a middleman.

Job Lot—An incomplete assortment of goods to be disposed of in a lump. Usually indicates small portions or remnants of a stock, the bulk of which has been sold.

Joint Stock—Property owned in common by several individuals known as stockholders.

Leakage—An allowance for waste of liquids in transit; refers particularly to liquids shipped in casks.

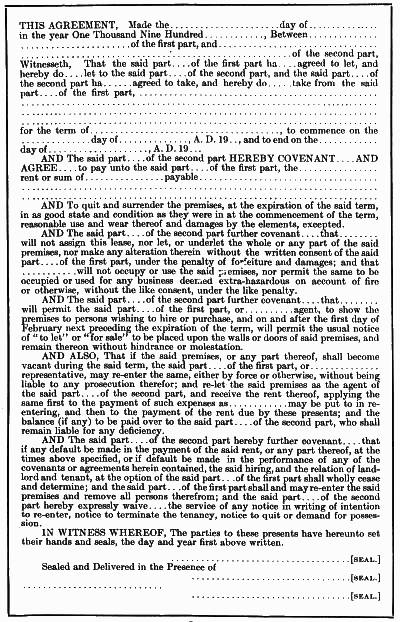

Lease—A written agreement covering the use of property during a specified period, at a stated rental.

Legal Tender—The lawful amount to be offered in payment of an obligation. Bank notes or other currency which passes for money.

Lessee—One who receives a lease. The lessor makes it.

Letter of Advice—A letter giving notice of some act in which the one receiving the advice has an interest—as making a shipment, notice of draft, etc.

Letter of Credit—A letter which authorizes the receiving, by the holder, of credit to a stated amount. Principally used by travelers to secure credit from foreign bankers.

Liabilities—The obligations or debts of a firm, corporation, or individual.

License—Permission, usually granted by a municipality, to conduct a specified business.

Liquidation—The closing-out of a business or an estate.

Loss and Gain—The amount of profits or losses of a business.

Maker—One who signs a note.

Manifest—A list or schedule of the articles in a ship's cargo, or of the goods comprising a shipment.

Order

Maturity—The time when an obligation or an account is due.

Mercantile Agency—A company which obtains and keeps for the use of its customers information showing the standing of business firms.

Merchandise—The stock in trade, or goods bought to be sold again.

Money Order—An order instructing a third party to pay money to the person named. A form in which money is transmitted.

Monopoly—The exclusive control of the manufacture or sale of an article.

Mortgage—A temporary transfer of title to land, goods, or chattels to secure payment of a debt.

Mortgagor—One who gives a mortgage. The one to whom the mortgage is given is the mortgagee.

Negotiable—An agreement or any commercial paper which can be transferred by delivery or endorsement—as a bank note or promissory note.

Net—Less all charges or deductions. Gross assets less liabilities leaves net capital; gross income less all expenses leaves net profit; etc.

Nominal—Having no actual existence; exists in name only.

Obligation—Indebtedness.

Open Account—An account which has not been paid.

Opening Entries—The entries made in the books when it is desired to open the accounts of a business.

Option—The right to be the first purchaser; a privilege.

Orders—Requests for the shipment of goods.

Original Entry—The first record made of a charge or credit which becomes the basis of proof of the account.

Overdraw—To draw a check for a greater amount than the drawer has on deposit in a bank.

Par—Face value.

Partnership—A firm; a union of two or more persons for the transaction of business or the ownership of property.

Payee—The one to whom money is to be paid. The one who pays the money is the payer.

Per Annum—By the year.

Per Cent or Per Centum—By the hundred.

Per Diem—By the day.

Personal Account—Any account with an individual, firm, or corporation.

Personal Property—All property other than real estate.

Petty Cash—A term used to signify small expenditures in actual cash.

Postdate—To date ahead; after the real date.

Post—To transfer amounts from books of entry to the ledger, which is the book of final record.

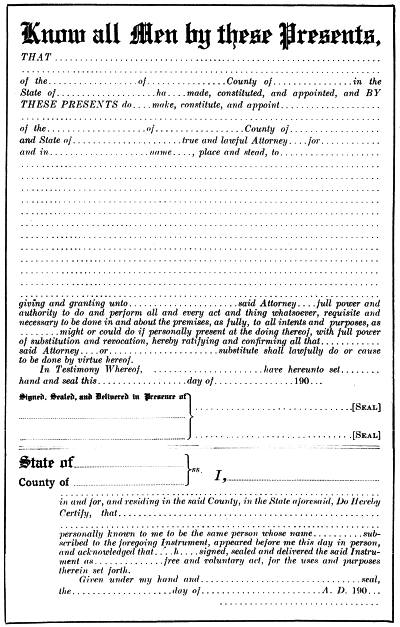

Power of Attorney—Authority to act for and in the name of another in business transactions.

Preferred Stock—Stock which participates in the profits before any dividend can be paid on the common or ordinary stock.

Premium—The amount paid above par value; the amount paid to an insurance company for insurance against loss.

Present Worth—The net capital of an individual.

Proceeds—The amount realized from a sale of property.

Profit and Loss—Synonymous with loss and gain.

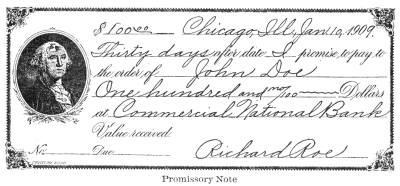

Promissory Note—A promise, signed by the maker or makers, to pay a stated sum at a specified time and place.

Promissory Note

Pro Rata—A distribution of money or goods in proportionate parts.

Protest—A formal notice acknowledged before a notary that a note or draft was not paid at maturity, and that the maker will be held responsible for the payment.

Quotation—A price named for a given article or for services.

Ratify—To approve; to sanction the acts of an agent.

Raw Material—Material to be manufactured into other products—as iron ore, pig iron, lumber, etc.

Real Estate—Primarily refers to land, although buildings are frequently included.

Rebate—An allowance or deduction. See Allowance.

Receipt—An acknowledgment that money or something of value has been received.

Receiver—One appointed to take charge of the affairs of a corporation, either solvent or insolvent, and administer its affairs under orders of the court.

Remittance—Money or funds of any character transmitted from one place to another.

Power of Attorney

Renewal Note—A new note given to take the place of a note that is due.

Rent—A payment for the use of property owned by another.

Resources—Synonymous with assets.

Revenue—Income of a business.

Revoke—To recall authority of another to act as agent.

Royalty—A stipulated amount paid to the owner of a mine, patent, copyright, etc., usually based on sales. The owner of a copyright receives a royalty based on the number of books sold.

Receipt

Schedule—Inventory of goods or statement of prices.

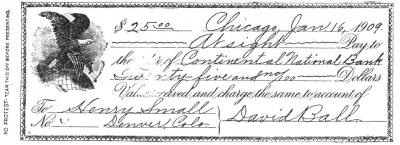

Sight Draft—A draft payable on presentation or at sight.

Solvent—Able to pay one's debts.

Statement—Commonly used to designate a list of bills to customers during a stated period. Also used to designate a financial summary showing profits and losses of a business.

Stockholder—An owner of stock in a corporation or joint stock company.

Storage—The charge for keeping goods in a store or warehouse.

Surety—One who has guaranteed or made himself responsible for the acts of another.

Syndicate—A combination of capitalists, usually temporary, for the conduct of some financial enterprise.

Tare—The amount deducted from gross weights to cover weight of packages—as crates, boxes, barrels, etc.

Tariff—A schedule of prices, as freight tariff. The duties imposed on imports or exports.

Terms—The conditions governing a given sale. "Terms cash" means that payment is to be made as soon as goods are delivered.

Tickler—Memoranda of matters requiring attention in the future, arranged according to dates.

Time Draft—A draft which matures at some future date.

Trade Discount—The discount allowed by a manufacturer to a jobber or by a jobber to a retailer.

Statement

Trade Mark—See Brand.

Ultimo—Principally used in correspondence to designate last month.

Valid—Legal or binding; usually applied to a properly executed contract.

Value Received—Used in notes to indicate that value has been given.

Void—Without legal force; not binding.

Voucher—A receipt; a document which proves the accuracy of an account or the authority for an expenditure.

Voucher

Warehouse—A building used for storage purposes.

Warehouse Receipt—A document acknowledging the receipt of goods for storage in a warehouse.

Warranty—An agreement to assume responsibility if certain facts do not prove as represented.

Way Bill—A document containing a list of goods shipped by a railroad.

Wholesale—A business which sells goods in large quantities, usually in original packages and to the trade only.

Working Capital—The capital actually used in the active operations of a business.

COMMERCIAL ABBREVIATIONS

The commercial abbreviations in the following list are in constant[36] use in the various lines of trade, and should be thoroughly understood by the student of accounting.

| A 1 | First-class |

| acct. | Account |

| ad | Advertisement |

| Agt. | Agent |

| amt. | Amount |

| Ans. | Answer |

| Art. | Article |

| asstd. | Assorted |

| Ass't. | Assistant |

| Atty. | Attorney |

| bal. | Balance |

| bbl. | Barrel |

| B. B. | Bill Book |

| bds. | Boards |

| bdls. | Bundles |

| bgs. | Bags |

| bk. | Book |

| bkt. | Basket |

| B. L. or B/L | Bill of Lading |

| bls. | Bales |

| bot. | Bought |

| B. P. or B/P | Bills Payable |

| bro't. | Brought |

| B. R. or B/R | Bills Receivable |

| B. Ren'd. | Bill Rendered |

| bu. | Bushel |

| bx. | Box |

| C. B. | Cash Book |

| ¢ or cts. | Cents |

| chgd. | Charged |

| c. i. f. | Cost, Insurance, and Freight |

| ck. | Check |

| cks. | Casks, Checks |

| Co. | Company |

| C. O. D. | Collect on delivery |

| Coll. | Collect or Collector |

| Com. | Commission |

| Com'l. | Commercial |

| Cons'd. | Consigned |

| Const. | Consignment |

| Cr. | Credit or Creditor |

| ctg. | Cartage |

| cwt. | Hundredweight |

| D. B. | Day Book |

| Dept. | Department |

| dft. | Draft |

| dis. or Disc't. | Discount |

| div. | Dividend |

| do. or ditto | The Same |

| doz. | Dozen |

| Dr. | Debit or Debtor |

| ds. | Days |

| ea. | Each |

| E. E. | Error excepted |

| E. and O. E. | Errors and omissions excepted |

| e. g. | For example |

| Ent. | Entry or Enter |

| Ent'd. | Entered |

| etc. or &c. | And others; And so forth |

| Exch. | Exchange |

| ex. | Express |

| exp. | Expense |

| Exr. | Executor |

| f. o. b. | Free on board |

| fol. | Folio; Page of a book |

| f'd, ford. | Forward |

| frt. | Freight |

| ft. | Foot, Feet |

| gal. | Gallon |

| gr. | Grain |

| gro. or gr. | Gross |

| guar. | Guaranteed |

| hdkf. | Handkerchief |

| hhd. | Hogshead |

| hund. | Hundred |

| I. B. | Invoice Book |

| in. | Inches |

| Ins. | Insurance |

| Inst. | Instant (this month) |

| int. | Interest |

| inv. | Invoice |

| invt. | Inventory |

| I. O. U. | I owe you; A due bill |

| J. | Journal |

| lb. | Pound |

| lbr. | Lumber |

| lab. | Labor |

| Manf. | Manufacture |

| Mdse. | Merchandise |

| Mem. | Memorandum |

| Mfd. | Manufactured |

| Mfst. | Manifest |

| Mfr. | Manufacturer |

| Mo. or mo. | Month |

| Mtg. | Mortgage |

| Ms. | Manuscript |

| Mut. | Mutual |

| Nat. or Nat'l. | National |

| N. B. | Take notice |

| No. | Number |

| N. P. | Notary Public, Net Proceeds |

| O. B. | Order Book |

| O. K. | All Correct; Approved |

| oz. | Ounce |

| p. | Page |

| pp. | Pages |

| pay't or pm't. | Payment |

| pc. | Piece |

| pcs. | Pieces |

| P. B. | Pass Book |

| P. C. B. | Petty Cash Book |

| pd. | Paid |

| per. | By; By the |

| [37]per an. | By the year |

| pk. | Peck |

| pkg. | Package |

| pop. | Population |

| pref. | Preferred |

| Prem. | Premium |

| Pro. | Proceeds |

| prop'r. | Proprietor |

| prox. | Next Month |

| P. S. | Postscript |

| pub. | Publisher |

| Qr. or qr. | Quarter, Quire |

| Qt. or qt. | Quart |

| rec'd. | Received |

| ret'd. | Returned |

| R. R. | Railroad |

| Ry. | Railway |

| S. B. | Sales Book |

| S. E. | Single Entry |

| Sec. | Secretary |

| Shipt. | Shipment |

| Shs. | Shares |

| Sig. | Signature |

| S. S. | Steamship |

| s. s. | To wit; Namely |

| St. dft. | Sight Draft |

| Sund. | Sundry |

| Supt. | Superintendent |

| sq. | Square |

| T. B. | Trial Balance; Time Book |

| ult. | Ultimo; Last month |

| via. | By way of |

| viz. | Namely |

| Vol. | Volume |

| vs. | Against |

| W. B. | Way Bill |

| Wk. | Week |

| Wt. or wt. | Weight |

| yr. | Year |

| yd. or yds. | Yard or Yards |

COMMERCIAL SIGNS AND CHARACTERS

The signs and characters most commonly used in business are the following:

| @ | To or At |

| a/c | Account |

| B/L | Bill of Lading |

| B/R | Bills Receivable or Bill Rendered |

| B/P | Bills Payable |

| B/S | Bill of Sale |

| ¢ | Cents |

| c/o | Care of |

| D/D | Days after date |

| D/S | Days after sight |

| F/B | Free on board |

| J/A | Joint Account |

| L/C | Letter of Credit |

| L/M | Letters of Marque |

| £ | Pounds Sterling |

| o/c | On account |

| o/c | Out of courtesy |

| % | Per cent |

| p | Per |

| $ | Dollars |

| # | Number, if written before a figure, as #25; Pounds, if written after, as 25# |

| ✓ | Check Mark |

| " | Ditto |

| ° | Degrees |

| ' | Prime; Minute; Feet |

| " | Seconds; Inches; also used as Ditto marks |

| 1¹ | One and one-fourth |

| 1² | One and one-half |

| 1³ | One and three-fourths |

| + | Plus |

| - | Minus |

| × | By or times |

| ÷ | Divided by |

| = | Equals |

DEFINITION AND OBJECTS OF BOOKKEEPING

1. Bookkeeping is the art of recording the transactions of a business in a manner that makes it possible to determine the accuracy of the records.

The objects of bookkeeping are:

(a) To exhibit a record of the separate transactions of a business.

(b) To furnish statistical information in respect to any particular class of transactions.

(c) To exhibit the financial standing or condition of a business.

When properly assembled the bookkeeping records become accounts (for definition, see Dictionary of Commercial Terms).

If correct methods are used, the bookkeeping records will be assembled or grouped in a manner to show their exact nature and their bearing on the status of the business, or the standing of the account.

2. Debit. The term debit designates those items in an account representing values with which we have parted, or transferred to another person or account. Debits are always placed on the left side (or in the left-hand column) of an account. Debits to persons are of the following classes:

(a) The transfer of merchandise.

(b) The rendering of services.

(c) The use of something of value.

Examples—

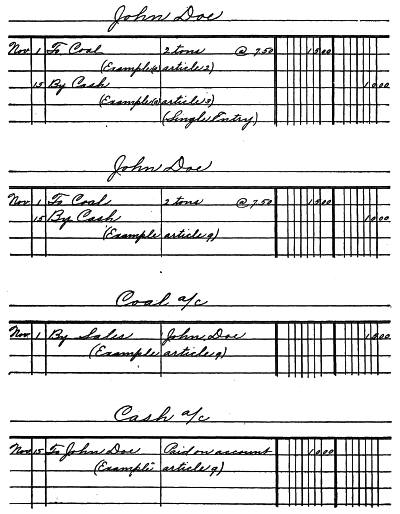

(a) We sell to John Doe two tons of coal at $7.50 per ton. We debit his account with the amount.

(b) We render services to Thos. Ryan for which he is to pay us a stated fee. We debit his account with the amount of the fee.

(c) We are to pay rent for the use of our offices. Our landlord debits us with the amount.

3. Credit. The term credit designates those items in an account representing value which we have received or which has been transferred to us. Credits are always placed on the right side (or in the right-hand column) of an account. Credits to persons are of the following classes:

(a) The receipt of merchandise or money.

(b) The rendering of services.

(c) The use of something of value.

Examples—

(a) John Doe pays us $10.00 on account. We credit his account with the amount.

(b) Our attorney makes a charge for legal services. We credit his account with the amount.

(c) We rent or lease property to another; and when payment is made, we credit his account.

4. Rules for Debit and Credit. Debit and credit are the fundamental principles of bookkeeping. The general rules to be followed in debits and credits are:

Debit cash when you receive it.

Debit a person when you trust him.

Debit a person when you pay him.

Credit cash when you pay it out.

Credit a person when he trusts you.

Credit a person when he pays you.

5. Balance. When the two sides of an account differ in amount, it is said to show a balance. If the debit side of the account is the larger, the difference is a debit balance. If the credit side of the account is the larger, the difference is a credit balance.

Example—If we debit John Doe's account for two tons of coal at $7.50 a ton, or $15.00 (see Example (a), Article 2), and credit his account with $10.00 paid (see Example (a), Article 3), the debit side of the account is $5.00 greater than the credit side. Therefore it shows a debit balance.

METHODS OF BOOKKEEPING

6. There are but two methods or systems of bookkeeping, and they are known as single entry and double entry. No matter in what form bookkeeping records are kept, the method must be either single or double entry.

Single entry is used only in very small businesses or by those who do not understand the advantages of double entry.

SINGLE ENTRY

7. As the name indicates, single entry is a single record of the transaction—that is, a record of one phase of the transaction only.

Example—John Doe's account would show that he received two tons of coal, but there would be no corresponding account to show that our supply of coal had been diminished.

Single entry fails to fulfil the object of bookkeeping, as it does not exhibit the true financial condition of the business, and is incapable of proof of accuracy.

DOUBLE ENTRY

8. Double entry is a system of making two entries (or a double record) of every transaction. In every business transaction, two distinct factors are involved—namely, that which is received, and that which is parted with. If we sell a given quantity of a commodity, we part with it, and the sale takes from or decreases the value of that particular commodity in our possession. If we sell for cash, the[40] transaction adds to our cash possessions; while if the value of the commodity is debited or charged to the account of a customer, it adds to the amount we are to receive from that customer.

9. Principle of Double Entry. Double entry is a system of debits and credits. One writer expresses it as a system of opposing contra things.

The fundamental principle of double entry is that there must be a corresponding credit for every debit.

Example—When we sell John Doe two tons of coal, we debit his account; but we have decreased the value of our stock of coal, and to complete the double entry, we credit coal account (or Merchandise, as the account representing our stock in trade is sometimes known). When he pays us money, we credit his account, and debit cash.

10. Advantages of Double Entry. The principal advantages of double entry bookkeeping are that the system permits of making an accurate exhibit of the standing of the business; it exhibits the profits and losses; it shows the sources of profits and the causes of losses; it permits of proof of the accuracy of the records.

11. Account books are ruled with special forms which adapt them to bookkeeping records. The forms of ruling are many and varied to suit the requirements of different classes of business. Rulings for double entry bookkeeping do not differ materially from those used in single entry. For double entry, at least two amount columns must be provided—one for debits, and one for credits.

The most common form of ruling is known as journal ruling. A book with this ruling is also known as a journal ledger.

The words in parentheses explain the purpose of the different columns. The abbreviations Dr. (debit) and Cr. (credit) are sometimes[41] written at the head of the amount column; but most bookkeepers omit them, as the position of the columns indicates their purpose.

DEMONSTRATION

To illustrate the manner of entering transactions in accounts, we show in the accompanying diagrams how the transactions used in the foregoing examples would appear in the proper accounts.

EXAMPLES FOR PRACTICE

1. On journal ruled paper, which can be procured at any stationer's, write up the account of John Doe as per example given in Articles 2 and 3.

2. Write up the account of John Doe, showing also the accounts necessary to complete the double entry, as per example in Article 11.

3. Write up the accounts covering the following transactions, by the single entry method:

Nov. 16. Sold to James Stevenson 4 cords of wood, at $4.75 per cord. Sold to Andrew White 2½ tons of coal, at $6.00 a ton.

Nov. 17. Sold to Wm. Johnson 1 ton of coal, at $7.00 a ton.

Nov. 19. Received from James Stevenson $12.00 cash, to apply on account.

Nov. 20. Received from Wm. Johnson $7.00 in payment of account.

4. Write up the same accounts by the double entry method, using a merchandise account to represent all classes of merchandise sold.

CLASSES OF ACCOUNT BOOKS

12. Account books are of two classes: (a) those in which complete records of transactions, or complete accounts, are kept; (b) those which contain particulars of individual transactions which must afterward be transferred to books of the (a) class.

Books of the (a) class are known as principal books or books of record; that is, they contain the final or permanent record of an account.

Books of the (b) class are of two kinds: (ba) books of original entry; (bb) auxiliary books.

Any book which contains the first (or original) record of a transaction is a book of original entry (ba).

A CORNER IN THE OFFICES OF THE PLATT IRON WORKS, DAYTON, OHIO

Any book in which records contained in books of original entry (ba) are assembled, to be transferred later to principal books (a), is an auxiliary book.

Any book used for the purpose of assembling statistical information is an auxiliary book.

The books most commonly used in double entry bookkeeping are: Order Book, Day Book, Cash Book, Journal, Sales Book, Purchase Book, Ledger.

13. Order Book. An Order Book is a book of original entry in which is entered a record of each order or request for the shipment or delivery of merchandise. The record shows the name and address of the customer, the kinds and quantities of goods wanted, and the prices at which they are to be sold.

The ruling of the order book varies according to the nature of the business. A simple form of ruling is shown.

14. Day Book. A Day Book is a book of original entry in which are entered full particulars of each completed transaction. These records are afterwards assembled in auxiliary books, from which they are transferred to the principal books.

The use of the day book was formerly universal, but it has been discarded by modern bookkeepers as its use involves unnecessary labor. The records formerly kept in the day book are now made directly in certain books then known as auxiliary, which makes of them books of original entry. The ruling of the day book is shown.

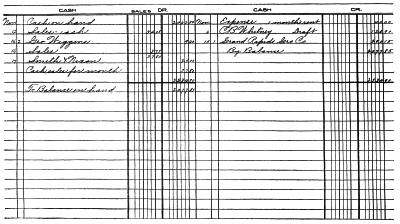

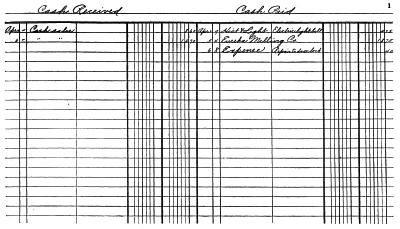

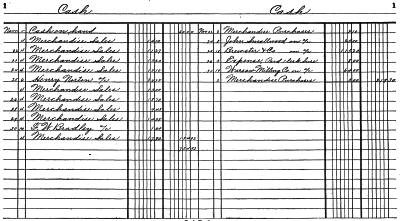

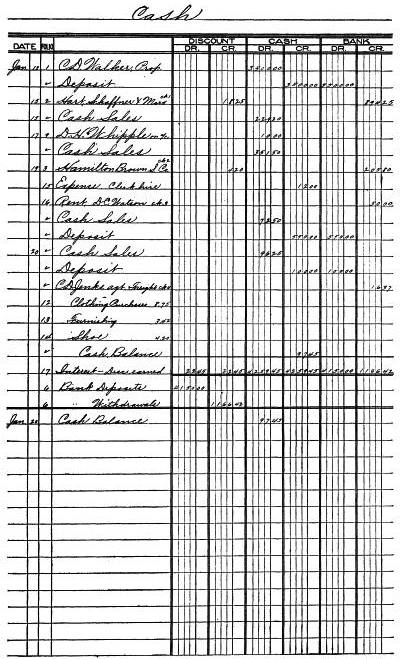

15. Cash Book. A Cash Book is a book of original entry containing records of all transactions which involve either the receipt or payment of cash. The records in the cash book are in fact a complete account with cash. We debit cash for all money received, and credit cash with all money paid out; therefore, the difference between the[44] total footings of the debit and credit sides of the cash book shows the amount of cash which we should have on hand. Since we cannot pay out more than we receive, the debit side should be the larger, unless both sides are equal, which shows that we have paid out all the cash received.

The amounts entered on the debit side of the cash book are transferred (or posted) to the credit side of the account of the one from whom the cash is received.

The amounts entered on the credit side of the cash book are posted to the debit side of the account of the one to whom the cash is paid.

There are many special forms of ruling for cash books, with separate columns for entering certain classes of receipts and payments of a special nature. The ruling of the cash book should be made to meet the requirements of the business in which it is to be used. A simple form of ruling is shown.

It will be noted that the left-hand page is used for the debit side, while the right-hand page is used for credits. This is the only account kept with cash.

16. Journal. A Journal is a book in which separate transactions are entered in a manner to preserve the balance necessary in double entry—that is, showing the proper debit and credit for each transaction. The journal is used for making adjusting entries, and it was formerly the custom to copy into this book from the day book the particulars of every transaction. Records are now made in the journal directly, which makes it a book of original entry.

The records in the journal are transferred or posted to the debit and credit sides of the accounts which they represent.

The journal is frequently combined with the cash book, and is then called a cash journal. An ordinary form of journal ruling is shown in Article 11.

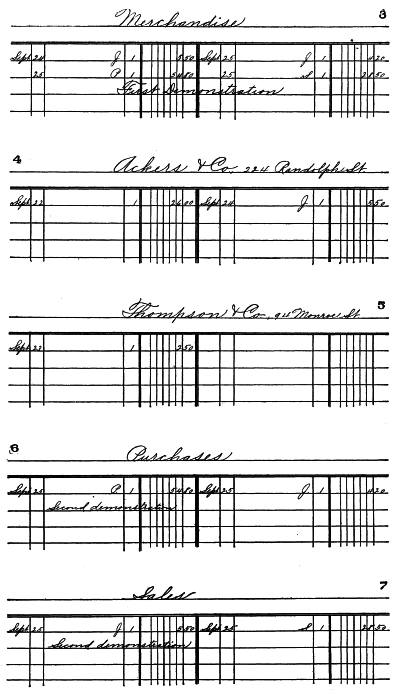

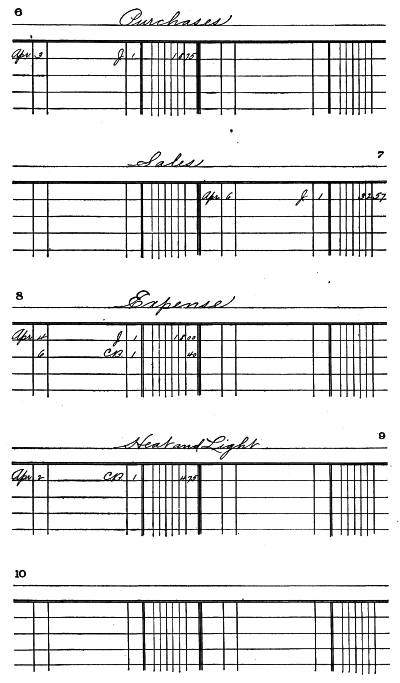

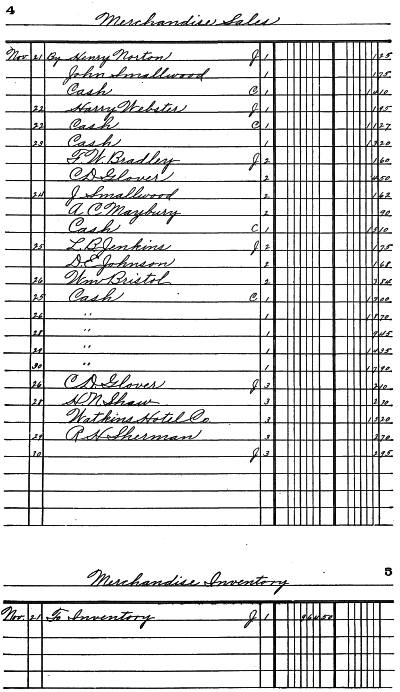

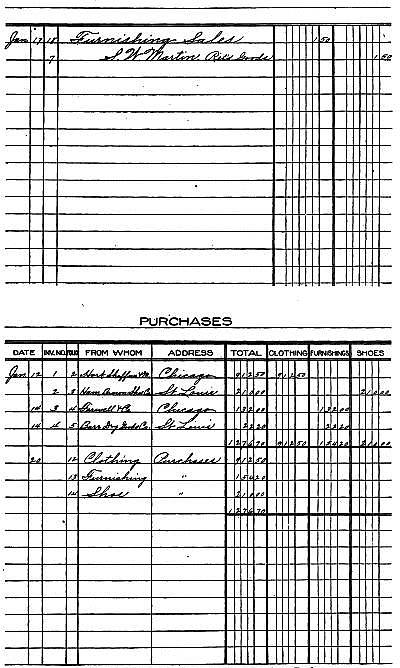

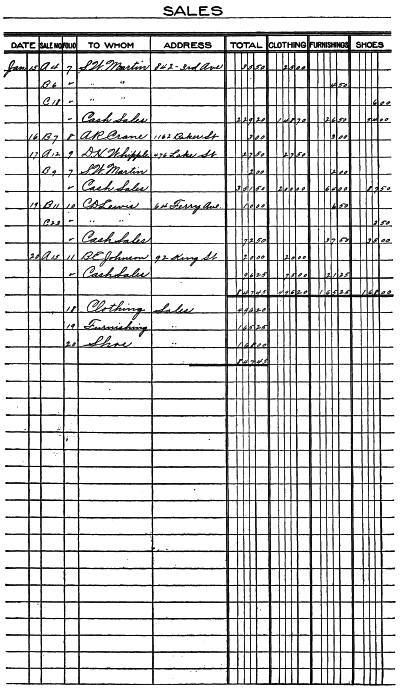

17. Sales Book. A Sales Book is an auxiliary book in which is kept a record of all goods sold, showing name of purchaser, quantity and kind of articles, prices, and amounts.

A sales book is a journal of sales. The amounts of individual sales are posted (transferred) to the debit side of the accounts of the purchasers. The footings of the sales book are carried forward until the end of the month, when the total amount is posted as one item to the credit side of the merchandise account, completing the double entry.

The merchandise account has been universally used in the past, all purchases being debited and all sales credited to this account. Certain other accounts (which will be explained later) are now recommended by leading accountants, to take the place of the merchandise account.

Sales books are usually ruled to meet the special needs of each business, separate columns being provided for a record of special classes of sales, or sales of special kinds of goods.

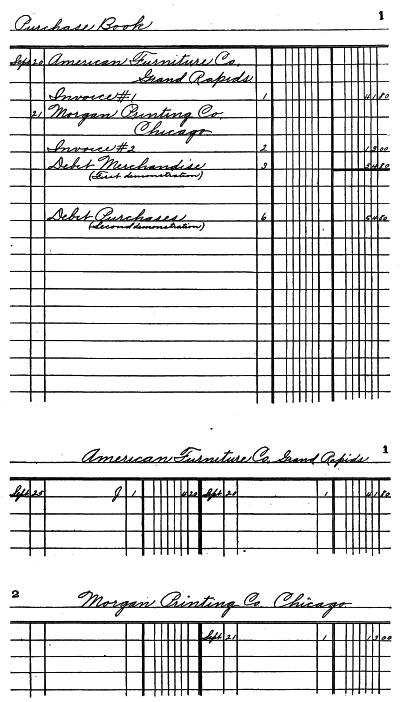

18. Purchase Book. A Purchase or Invoice Book is the opposite of the sales book, being used for a record of all purchases made. Like the sales book, the totals are carried forward to the end of the month, and posted as one item to the debit side of the merchandise account. The amounts of the separate transactions are posted daily to the credit of the persons from whom the goods are purchased.

The purchase book is a purchase journal, and the ruling is the same as that of other journals.

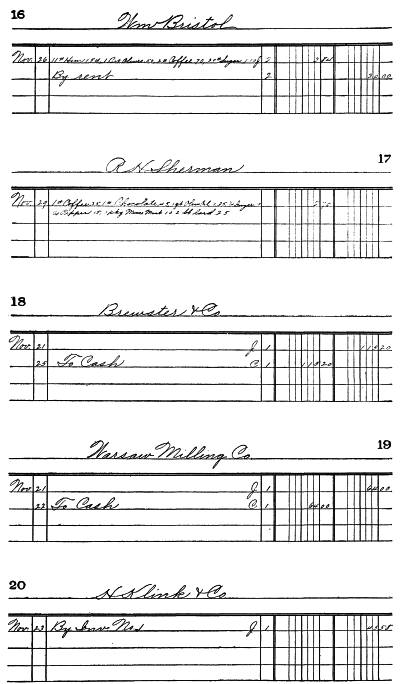

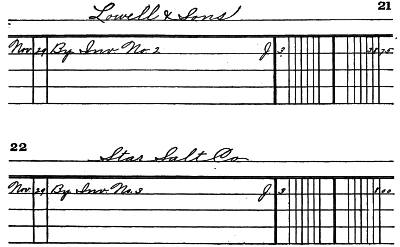

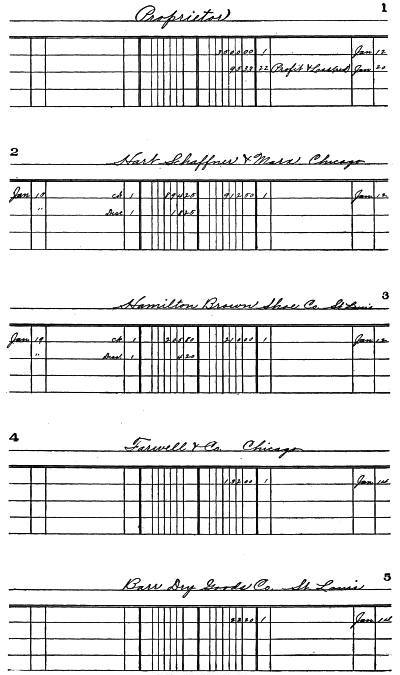

19. Ledger. The Ledger is the principal book, in which particulars of every transaction of every nature are summarized. It is, in fact, a transcript of all other books of the business except those used solely for statistical purposes.

The ledger is the book which contains the final or complete records of all dealings, either with an individual or with respect to a specific class of transactions—as expenditures for a certain purpose, or receipts of a given character, or sales of a given kind of goods.

A transcript of the ledger accounts exhibits the progress and standing of the business.

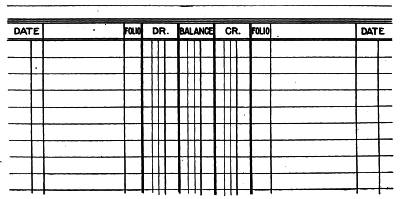

Like other books, ledgers are now made with special forms of ruling, depending on the purpose for which they are to be used. The old style or common form of ledger ruling is shown (p. 35).

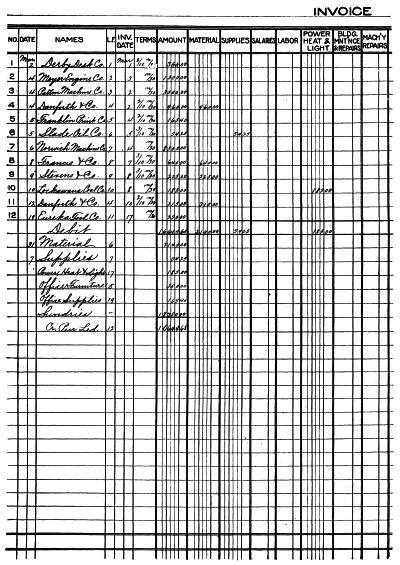

20. Invoice or Bill. An Invoice or Bill is an itemized statement or record of goods sold by one person to another. The invoice or bill is used in every line of business. A conventional form of invoice is shown (p. 5).

RECORDING TRANSACTIONS

21. The records of transactions in the journal which show what accounts are debited and what accounts are credited are called journal entries. The act of making these entries is known as journalizing.

It was formerly the custom to journalize each individual transaction from the day book, but in modern bookkeeping the journal is used only for adjusting and special entries.

22. Posting. When the record of a transaction is transferred to the ledger from a book of Class (b), it is said to be posted. The act of making the transfer is called posting.

The original method was to itemize all transactions in the ledger, but the present custom is to post the totals only.

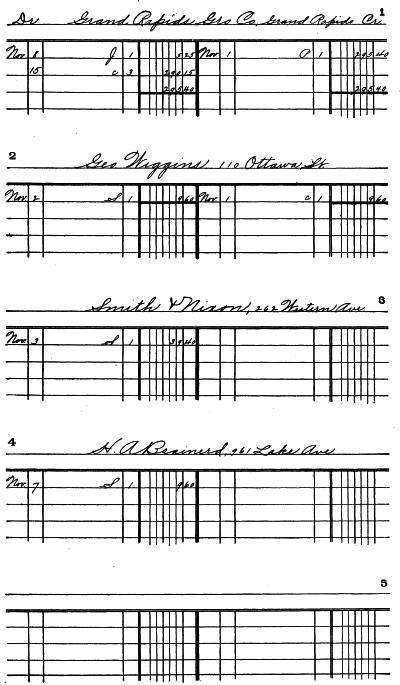

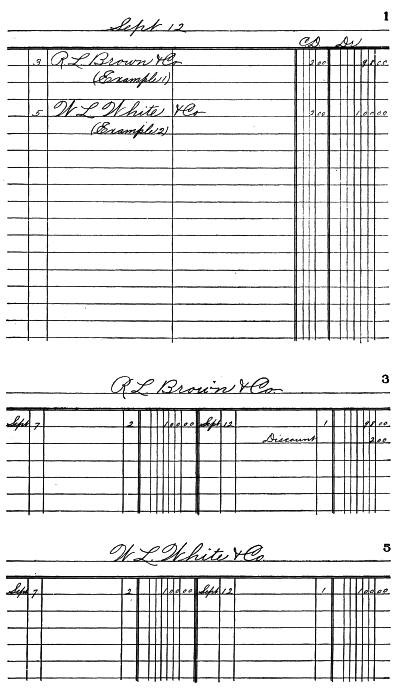

23. When a record is transferred from one book of Class (b) to another, or posted to the ledger, the page number of the book to or from which it is transferred or posted is entered in the column known[47] as the folio column. This is done that the transaction may be traced from one book to another. The presence of the page number also serves as a check to show that the item has been posted.

Example—An item is to be posted from page 1 of the sales book to page 10 of the ledger. In the folio column of the ledger will be entered "S 1" indicating that the item will be found on page 1 of the sales book. In the folio column of the sales book will be entered "10" indicating that the item has been posted to page 10 of the ledger.

24. Ledger Index. An index to the ledger is necessary to enable us to find the accounts. In small ledgers the index is placed in the front of the book itself, while for large ledgers a separate index book is used. There is a distinct advantage in this, as the index book can be kept open on the desk while posting is being done, and the names found much quicker than when it is necessary to turn the leaves of the ledger to find the index.

When an account is opened in the ledger, the name should be written in the index, followed by the page number. The names in the index are arranged in alphabetical order, each name being written under the letter of the alphabet corresponding to the first letter in the name. For example:

| A | B | C | |||||

| Adams, J. C. | 11 | Bacon, I. H. | 2 | Crandall, Jas. | 7 | ||

| Andrews, Henry | 14 | Brown, Henry | 9 | Campbell, Don. | 12 | ||

In a large index, one or more pages are used for a letter; while in a small index, several letters may be placed on the same page.

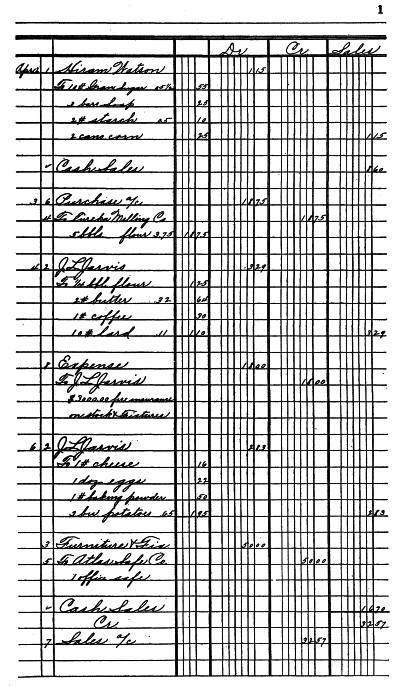

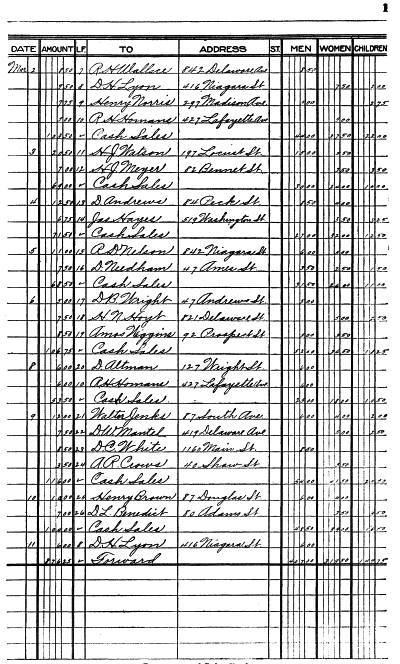

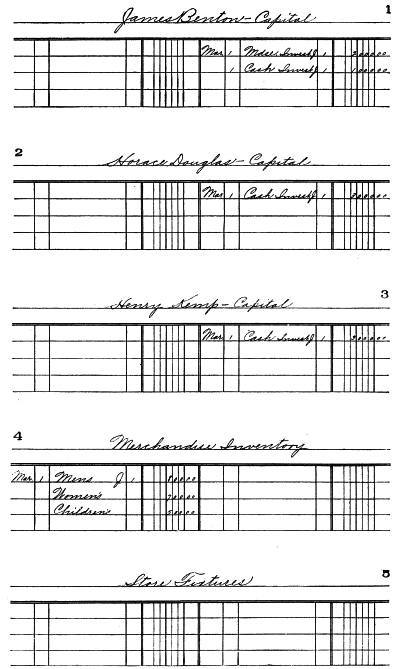

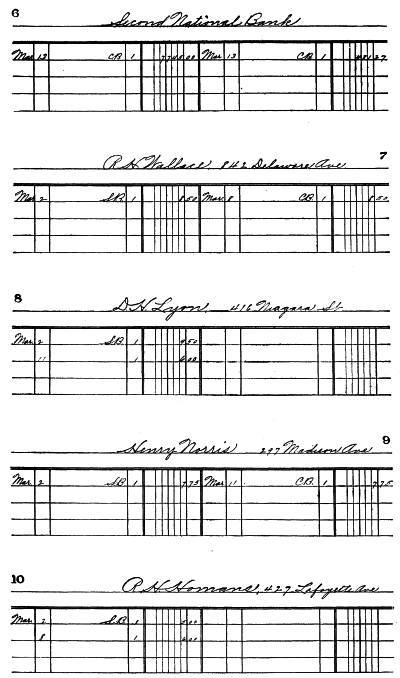

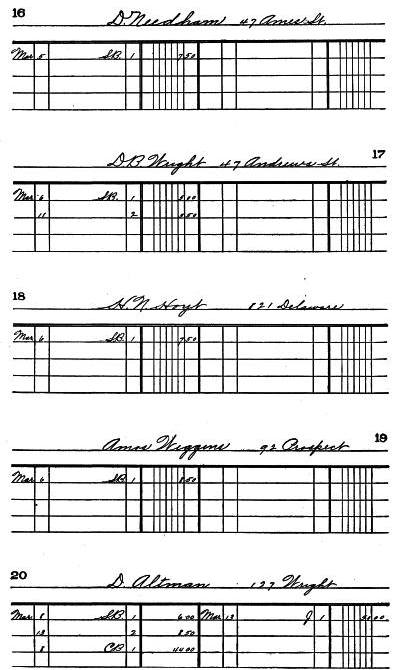

SAMPLE TRANSACTIONS

25. The following sample transactions are carried through the books described in this section, showing the proper entries and postings (see pp. 40-43). The day book has been omitted, as it is practically obsolete, not being used by progressive bookkeepers.

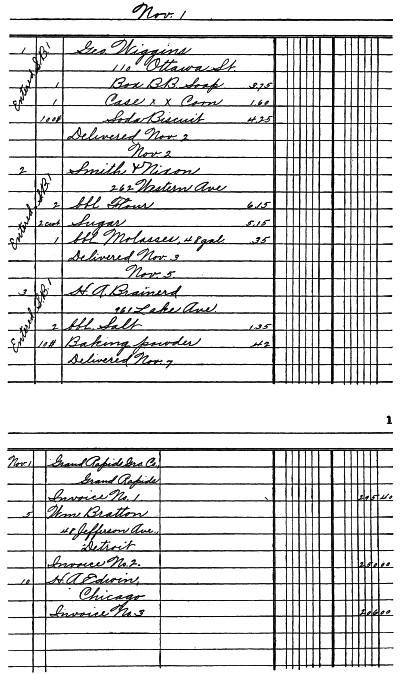

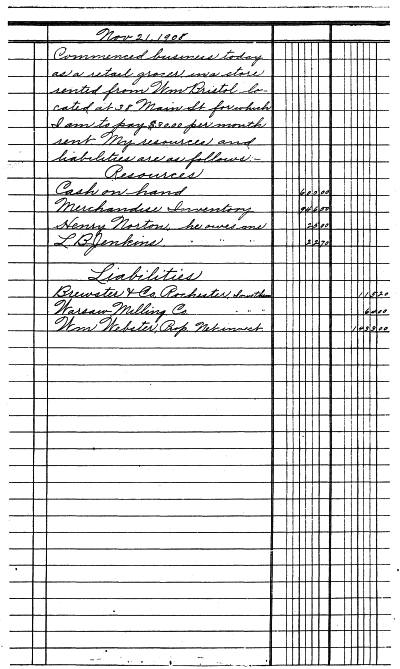

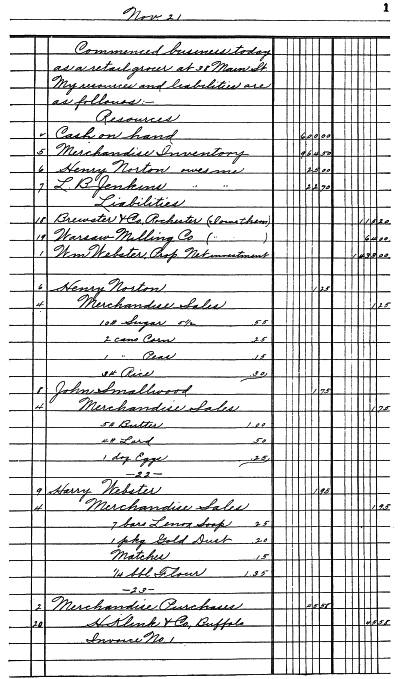

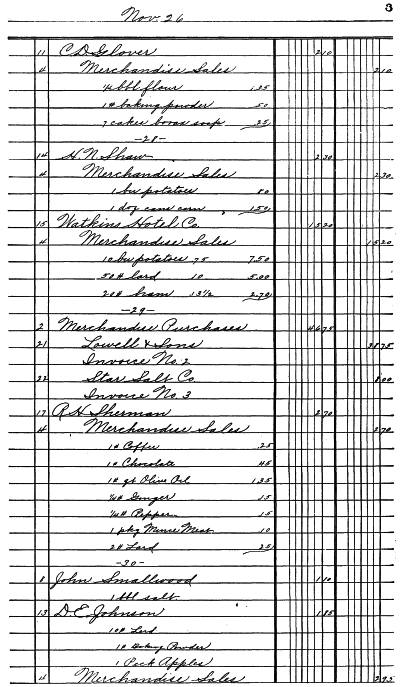

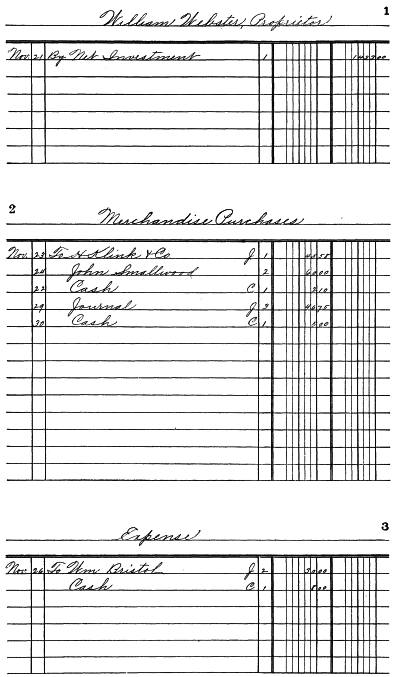

Muskegon, Mich., Nov. 1, 1907.

I, Robert B. Robinson, have this day commenced business as a wholesale dealer in groceries and provisions. I have rented the store located at 68 Pine St., from Geo. Baker, at $40.00 a month. My resources and liabilities are as follows:

| Resources | ||||

| Cash on hand | $ | 2,462.50 | ||

| Merchandise per inventory | 1,147.20 | |||

| Due me from Roger Bros. | 219.40 | |||

| Liabilities[48] | ||||

| C. B. Whitney, Grand Rapids | $ | 126.90 | ||

| My net investment | 3,702.20 | |||

| —Nov. 1— | ||||

| Bought from Grand Rapids Gro. Co., Grand Rapids, Mich. | ||||

| On account | ||||

| 10 cwt. sugar | $4.85 | $ | 48.50 | |

| 10 bbls. flour | 5.25 | 52.50 | ||

| 150 " salt | 1.10 | 165.00 | ||

| 2 " molasses 48 | ||||

| 50,98 gals. | .30 | 29.40 | $295.40 | |

| —1— | ||||

| Paid Geo. Baker | ||||

| For 1 month's rent | Cash | 40.00 | ||

| —2— | ||||

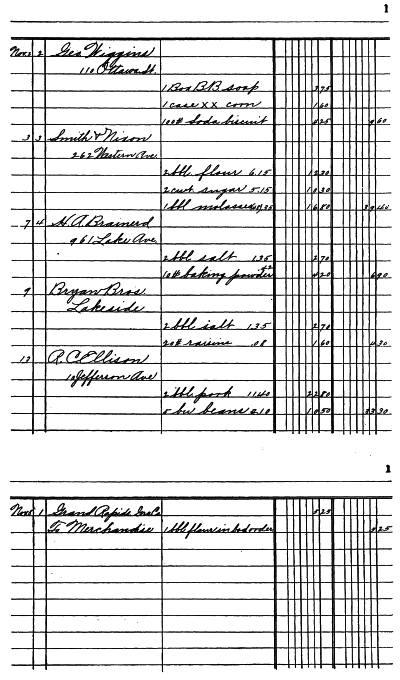

| Sold to Geo. Wiggins, 110 Ottawa St. | ||||

| On account | ||||

| 1 box B. B. soap | 3.75 | |||

| 1 case X. X. corn | 1.60 | |||

| 100# soda biscuit | 4.25 | 9.60 | ||

| —3— | ||||

| Sold to Smith & Nixon, 262 Western Av. | ||||

| On account | ||||

| 2 bbl. flour | 6.15 | 12.30 | ||

| 2 cwt. sugar | 5.15 | 10.30 | ||

| 1 bbl. molasses, 48 gal. | .35 | 16.80 | 39.40 | |

| —5— | ||||

| Bought from William Bratton, 48 Jefferson Av., Detroit | ||||

| On account | ||||

| 10 sacks Java coffee, 1,000# | .25 | 250.00 | ||

| —6— | ||||

| Sent to C. B. Whitney, Grand Rapids | ||||

| Draft to balance account | 126.90 | |||

| —7— | ||||

| Sold to H. A. Brainerd, 961 Lake Av. | ||||

| On account | ||||

| 2 bbls. salt | 1.35 | 2.70 | ||

| 10# baking powder | .42 | 4.20 | 6.90 | |

| —8—[49] | ||||

| Charge Grand Rapids Gro. Co. | ||||

| 1 bbl. flour received in bad order | 5.25 | |||

| —9— | ||||

| Sold to Bryan Bros., Lakeside | ||||

| On account | ||||

| 2 bbls. salt | 1.35 | 2.70 | ||

| 20# raisins | .08 | 1.60 | 4.30 | |

| —10— | ||||

| Bought from H. A. Edwin, Chicago | ||||

| On account | ||||

| 20 bbls. pork | 10.30 | 206.00 | ||

| —12— | ||||

| Sold for cash | ||||

| 3 bbl. pork | 11.35 | 34.05 | ||

| —13— | ||||

| Sold to R. C. Ellison, 10 Jefferson Av. | ||||

| On account | ||||

| 2 bbl. pork | 11.40 | 22.80 | ||

| 5 bu. beans | 2.10 | 10.50 | 33.30 | |

| —14— | ||||

| Received from Geo. Wiggins | ||||

| Cash to balance | 9.60 | |||

| —15— | ||||

| Sent to Grand Rapids Gro. Co. | ||||

| Draft to balance | 290.15 | |||

| —16— | ||||

| Sold for cash | ||||

| 1 box soap | 3.75 | |||

| —17— | ||||

| Received from Smith & Nixon | ||||

| Cash on account | 25.00 | |||

PROMISSORY NOTES

26. A promissory note is a form of commercial paper much used in business. Goods are sold on specific terms—that is, to be paid for in a certain time after date. Profits are based on the supposition that the bills will be paid when due. When not so paid, the debtor is virtually borrowing money from the creditor, and should pay interest for the use of that money just as he would if he had borrowed it from a bank. To settle the account when it is not convenient to pay cash, it is customary to give a promissory note for the amount, plus interest, payable on a certain date. The promissory note is more convenient for the creditor; for when it bears his endorsement, his bankers will discount it, thus giving him the money for use in his business. Even though he may not discount it, the promissory note is better for the creditor, as it gives him a definite promise to pay, which he does not have when the debt is represented by an open account.

27. Bills Receivable and Bills Payable. The commercial term for promissory notes accepted by us is Bills Receivable. The commercial term for promissory notes given by us is Bills Payable. The term "bill" is used in this connection for the reason that a promissory note is a negotiable instrument, and when indorsed it becomes practically a bill of exchange. The accounts in the ledger which represent notes receivable and notes payable are called Bills Receivable Account and Bills Payable Account.

The bills receivable account is debited when a note is received, and credited when a note is paid. The balance of bills receivable account shows the amount of unpaid notes payable to us.

The bills payable account is credited when we give a note and debited when we pay a note. The balance of bills payable account shows the amount of the notes that we owe.

28. Bill Book. For the purpose of keeping a record of bills receivable and bills payable, a book known as a bill book is used. Any draft, note, due bill, or other written promise to pay a specified sum at a stated time, should be treated as a note or bill—receivable or payable, as the case may be. The bill book is an auxiliary book, and the record kept is usually treated as a memorandum only, records of each transaction being made in the journal. The form shown (p. 45) is one in common use.

29. Acceptances. A draft when accepted—that is, when it becomes an acceptance—has the same value as a promissory note, for it is a definite promise to pay on a specified date. Drafts are used for the collection of accounts in other cities than the one in which the creditor's place of business is located. A draft may call for payment a certain number of days after date, or it may call for payment at sight. The former is known as a time draft, while the latter is a sight draft.

30. Discount and Exchange. When a promissory note is taken to the bank for the purpose of raising money, it is customary for the banks to calculate the interest for the time the note is to run, and to deduct this from the principal, giving the borrower the net amount only. In other words, the interest is paid in advance, and such advance payment of interest is called discount.

When a draft is collected through a bank, a small fee is charged, and this fee is called exchange. Exchange is also charged for the collection of out-of-town checks, especially if they are drawn on banks in small towns and cities.

BANK DEPOSITS

31. When money is deposited in a bank, a list of the items in the deposit is made on a blank known as a deposit ticket or deposit slip. These deposit tickets are furnished by the bank for the convenience of its customers.

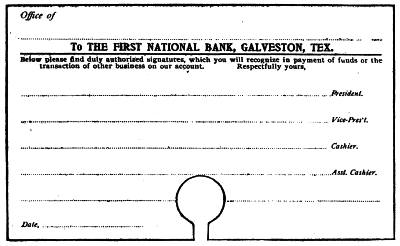

32. Signature Card. Money deposited in a bank can be withdrawn only by presenting a written order or check, signed by the one in whose name the money is deposited. That the bank may know that money is not paid on checks that do not bear the correct signature, each depositor is required to leave at the bank the signature or signatures which are to be honored. These signatures are written on a card, known as a signature card, which the bank keeps for reference.

33. Check Books. Blank checks are usually bound in book form, the checks themselves being perforated so that they can be easily removed. These check books are in most cases furnished by the bank. The number of checks on a page varies, but is seldom more than four. When a check is written, the number, date, name, and amount should be written on the face of the stub. To keep a convenient[57] record of the balance in the bank, it is well to enter a list of all checks and deposits on the back of the check stubs.

Signature Card

34. Pass Book. The bank pass-book should be taken to the bank whenever a deposit is made, as it contains the bank's receipt for all money deposited.

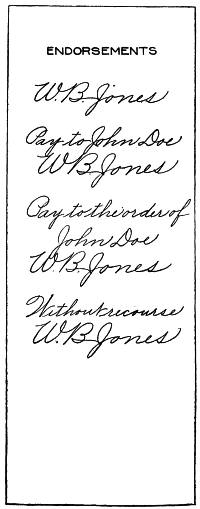

35. Indorsement of Checks. Before a check can be deposited in the bank, it must be indorsed by writing the name of the payee across the back. The indorsement should be on the back of the left end of the check—never on the right end. Several forms of indorsement are shown (p. 48). When the name only is written, it makes the check payable to the bearer, and is known as a blank indorsement. When the words "Pay to" are used, the check becomes payable to the one whose, name appears immediately under the words. It can only be paid to him in person or credited to his account at any bank at which he may deposit the check. A check indorsed with the words "Pay to the order of" permits of a further transfer, and provides a receipt from the one to whom it is so indorsed. When a check is to be deposited, the proper indorsement is "For deposit only." This is of special importance when deposits are sent by messenger. Such indorsements usually include the name of the bank, and are made with a rubber stamp.

36. Depositing Cash. It is a good plan to deposit all cash[58] received and to pay all bills by check, except such small items as are paid from petty cash. By doing this, all transactions pass through the bank, providing a receipt in every case in the form of a canceled check bearing the indorsement of the payee.

Endorsement

37. Treatment of Petty Cash. It is customary in business establishments to keep on hand a certain sum of cash out of which to pay items of expense such as office supplies, etc., when the amount is too small or it is not convenient to write a check.

The best way to handle this is to draw a check for a certain amount, and keep this money separate from the cash received from day to day. At the end of the month, or sooner if the fund is low, draw a check payable to cash for the amount paid out and charge it to expense. This will leave the fund intact.

Example—We shall suppose the amount of petty cash to be kept on hand to be $25.00; and the amount paid out, $15.60, leaving $9.40 on hand. A check will be made for $15.60, to be charged to expense through the regular cash book. The cash will be drawn from the bank, and the amount added to the $9.40, making a total of $25.00.

A record of petty cash is usually kept in a small book called a petty cash book. This book has the regular two-column journal ruling. In handling petty cash, great care should be taken to secure a receipt in some form for every payment.

A BIRD'S-EYE VIEW OF THE BELOIT, WIS., FACTORY OF THE FAIRBANKS-MORSE CO.

SAMPLE TRANSACTIONS

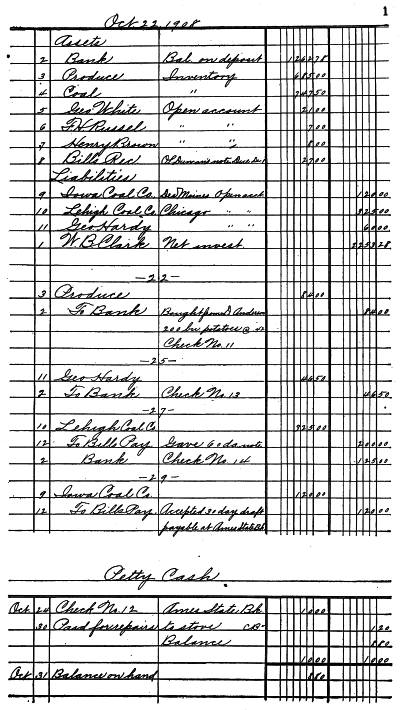

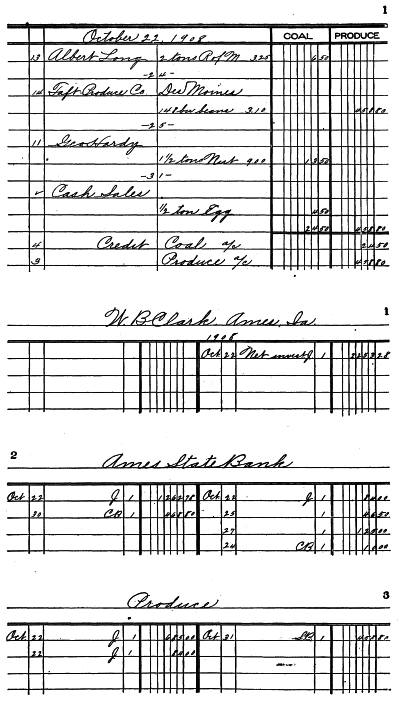

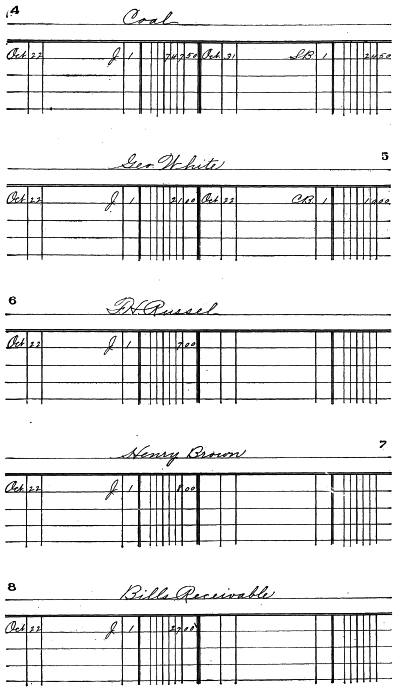

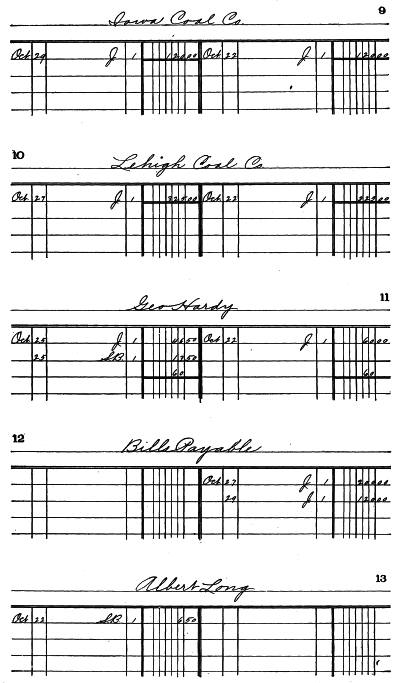

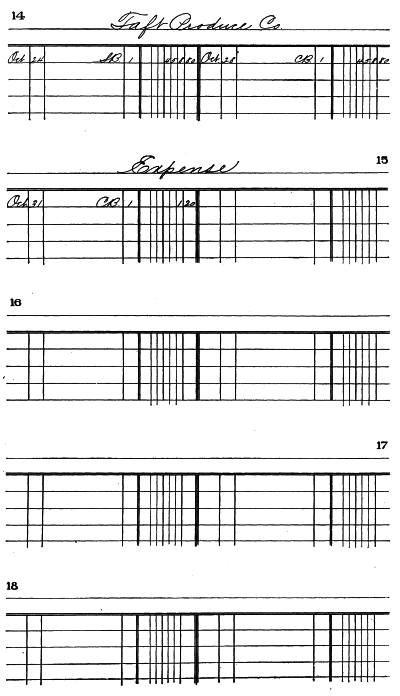

38. The following sample transactions taken from the books of W. B. Clark, Ames, Ia., illustrate the use of the papers and accounts explained in this section, and show how the transactions would appear on the books.

Mr. Clark is a shipper of produce, and a retail dealer in coal. His assets and liabilities are as follows:

| Assets | ||

| Cash in bank | $1,262.78 | |

| Inventory, Produce | 685.00 | |

| " Coal | 747.50 | |

| Geo. White—Open account | 21.00 | |

| F. H. Russel " " | 7.00 | |

| Henry Brown " " | 8.00 | |

| O. L. Duncan—Note due Dec. 1 | 27.00 | $2,758.28 |

| ———— | ||

| Liabilities | ||

| Iowa Coal Co., Des Moines, Open acct. | $120.00 | |

| Lehigh Coal Co., Chicago, Ill., Open acct. | 325.00 | |

| George Hardy, Open account | 60.00 | 505.00 |

| ———— | ||

As he wishes to know how much business he is doing in each department of his business, he keeps accounts in the ledger with both produce and coal instead of one merchandise account. In the sales book, one column is used for coal sales, and one for produce sales. No purchase book is kept, all purchases being posted from the journal or cash book.

| —Oct. 22— | ||

| Bought from David Andrews, for cash | ||

| 200 bu. potatoes @ | .42c | $84.00 |

| Paid by check No. 11. | ||

| —22— | ||

| Sold to Albert Long on account | ||

| 2 tons run of mine coal | $3.25 | 6.50 |

| —23—[60] | ||

| Received from Geo. White on account | ||

| Cash | 10.00 | |

| —24— | ||

| Sold to Taft Produce Co., Des Moines, on account | ||

| 148 bu. beans | 3.10 | 458.80 |

| —24— | ||

| Drew from bank for petty cash | 10.00 | |

| Check No. 12. | ||

| —25— | ||

| Sold to Geo. Hardy on account | ||

| 1½ tons nut coal | 9.00 | 13.50 |

| Gave him check No. 13. | 46.50 | |

| —27— | ||

| Gave to Lehigh Coal Co., Chicago. | ||

| 60-day note | 200.00 | |

| Check No. 14. | 125.00 | |

| —28— | ||

| Taft Produce Co. paid sight draft through Iowa | ||

| National Bank | 458.80 | |

| —29— | ||

| Accepted 30-day draft made by Iowa Coal Co. | 120.00 | |

| Payable at Ames State Bank | ||

| —30— | ||

| Deposited in Ames State Bank | ||

| Draft Iowa National Bank | 458.80 | |

| Cash | 10.00 | |

| —30— | ||

| Paid for repairs to stove, cash | 1.20 | |

| —31— | ||

| Sold for cash, ½ ton egg coal | 4.50 | |

ACCOUNTING DEPARTMENT IN THE NEW YORK OFFICE OF J. WALTER THOMPSON COMPANY

THEORY OF ACCOUNTS

PART II

CLASSES OF ACCOUNTS

39. In double entry bookkeeping, the accounts used may be divided into the two general classes of personal and impersonal. For the purpose of more complete classification, the second class is further subdivided into real, representative, and nominal accounts.

40. Personal Accounts. A personal account is a record of transactions with a particular person or persons.

Examples—

A record of transactions with persons who buy goods from us.

A record of transactions with persons from whom we buy goods.

41. Real Account. A real account is a record of transactions with respect to a particular property. Properties which we possess are termed resources or assets; therefore all real accounts are also asset accounts.

Examples—

Real estate (land and buildings), Machinery, Furniture, Merchandise, etc.

42. Representative Account. A representative account is a summary of all debit or credit transactions of a particular class with respect to several personal accounts. The debit or credit to this account completes the double entry, and illustrates the rule that in double entry there must be a credit for every debit.

Example—

We sell goods to a number of customers, and the amounts of these sales are debited to their several accounts. To complete the double entry, we credit the total amount of these sales to an account called sales account. The total credits to this account during any given period represent the sales to all customers for the same period, and the sales account is a representative account.

The total debits to all customers' accounts for goods purchased in one month amount to $1,423.62. This amount is credited to the sales account. Likewise the purchases for the same period amount to $947.20, and the several amounts are credited to the personal accounts of those from whom the purchases were made, while a like amount is debited to a representative account known as a purchase account.